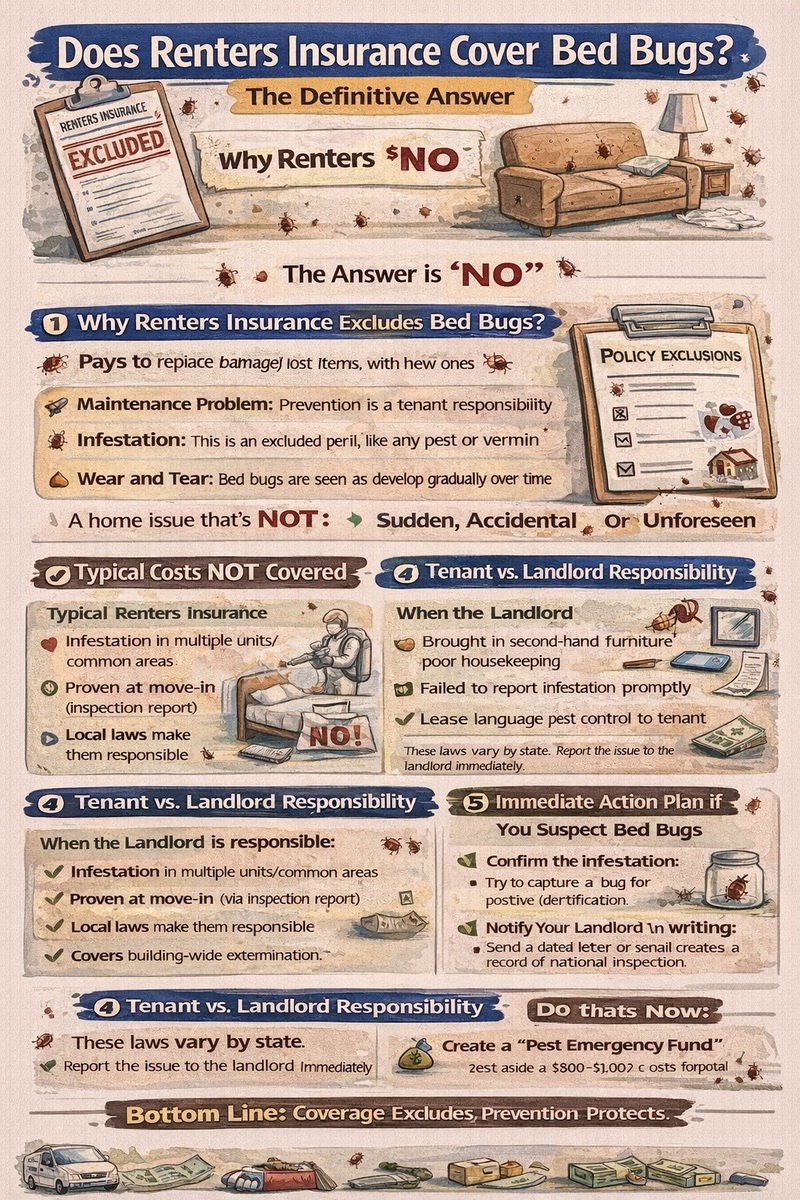

The direct answer to “Does renters insurance cover bed bugs?” is almost always a firm no. Bed bug infestations and the costs associated with eradicating them are overwhelmingly excluded from standard renters insurance policies. Insurance companies classify bed bugs as a maintenance issue, a pest infestation, or a problem caused by gradual wear and tear—all categories explicitly not covered. This means your policy will not pay for professional extermination, replacing infested furniture like mattresses or couches, or any temporary housing if you must vacate. However, in extremely rare cases, if you can prove a sudden, specific, and covered event (like a fire or vandalism) directly caused bed bugs to invade your unit from a neighboring one, there might be a path to limited coverage, but this is highly exceptional. Understanding this exclusion is crucial to avoid surprise costs and to focus on proactive prevention and knowing your legal rights as a tenant.

The Core Reason for Exclusion: Maintenance vs. Sudden Peril

To understand why the answer to “Does renters insurance cover bed bugs?” is negative, you must understand the fundamental principle of renters insurance. It is designed to protect against sudden, accidental, and unforeseen events—known as “covered perils”—like fire, theft, or burst pipes. Bed bug infestations are viewed by insurers as a maintenance or housekeeping issue. They develop gradually over time, are preventable with proper vigilance, and are considered a general risk of living in multi-unit dwellings. Because insurance is not intended for predictable maintenance problems or issues considered under the control of the property owner or tenant, bed bugs fall firmly into the category of excluded losses.

The “Wear and Tear” and “Infestation” Exclusions

Standard renters insurance policies contain specific exclusions for:

- Insect or Vermin Infestation: Directly excludes damage caused by pests, including bed bugs, rodents, or termites.

- Gradual Damage: Excludes loss that occurs slowly over time, such as the spread of an infestation.

- Wear and Tear: Excludes deterioration due to aging or lack of maintenance.

These exclusions are clear and broad, leaving little room for interpretation. The cost of extermination is seen as a routine cost of occupancy, similar to replacing a lightbulb or unclogging a drain, not an insurable event.

Why Insurers Are So Firm on This Exclusion

From an insurer’s perspective, bed bug claims are problematic for three key reasons: 1) Difficulty of Proof: It’s nearly impossible to prove when or how an infestation began, opening the door for fraudulent claims. 2) High Contagion Risk: Infestations easily spread between units, making it difficult to assign liability and cost. 3) Preventability: Insurers believe consistent inspection and immediate action can prevent widespread infestation. These factors make bed bugs an unacceptable financial risk for insurance pools designed for acute, accidental losses.

Possible (But Rare) Exceptions and Gray Areas

While direct coverage for the infestation itself is excluded, there are narrow, hypothetical scenarios where a renters insurance claim related to bed bugs might be partially considered. These are exceptions that prove the rule and require very specific circumstances.

Scenario: Damage from a Covered Peril Leading to Infestation

Imagine a rare event: a fire or significant vandalism in a neighboring unit forces bed bugs to flee and migrate into your apartment through walls or ducts. In this case, you might have a claim for the damage caused by the covered peril (the migrating bugs), but not for the cost to exterminate them. Even then, proving direct causation would be an immense challenge requiring expert entomologist testimony, and most insurers would likely deny the claim based on the infestation exclusion. This scenario is more theoretical than practical.

Scenario: Additional Living Expenses (ALE) Due to Treatment

If a covered peril (like a fire) makes your home uninhabitable, your loss of use coverage pays for a hotel. However, if you must vacate solely for bed bug fumigation (which is not a covered peril), ALE does not apply. The only potential overlap is if a covered event and necessary bed bug treatment happen simultaneously, and the treatment is mandated by authorities as part of making the home habitable again after the covered event—an extremely convoluted situation.

| Situation | Typical Renters Insurance Coverage | Reason |

|---|---|---|

| Discovering bed bugs and needing extermination. | NO | Excluded as an infestation/vermin. |

| Throwing out an infested mattress, sofa, and clothing. | NO | Damage caused by an excluded peril is also excluded. |

| Paying for a hotel during fumigation. | NO | Loss of use requires a covered peril; infestation is not covered. |

| Medical bills from bed bug bites or allergic reactions. | NO (under property policy) | Medical payments coverage is for guest injuries on your property, not your own illnesses. |

| Bed bugs ruin furniture after a covered fire in next-door unit forces them to migrate. | Highly Unlikely / Case-by-Case | Extremely difficult to prove direct causation; insurer will likely cite infestation exclusion. |

Who Is Responsible? Tenant vs. Landlord Obligations

Since renters insurance won’t cover it, the financial responsibility for bed bug eradication typically falls to either the tenant or the landlord, governed by state and local laws and the specifics of your lease agreement.

When the Landlord Is Typically Responsible

In many jurisdictions, the landlord is legally responsible for providing a habitable premises, which includes addressing pest infestations that were not caused by the tenant. This is especially true if:

- The infestation is present in multiple units, indicating it originated in common areas or another tenant’s space.

- The tenant can prove the bugs were present upon move-in (documentation from a move-in inspection is key).

- Local housing codes explicitly place pest control responsibility on the property owner.

The landlord’s responsibility usually covers the cost of professional extermination for the entire building.

When the Tenant May Be Held Responsible

A tenant can be held financially liable if they are found to have caused or significantly contributed to the infestation. This could be due to:

- Bringing in infested second-hand furniture.

- Extremely poor housekeeping that facilitates infestation.

- Failing to report the problem promptly, allowing it to spread.

- Lease language that specifically assigns pest control costs to the tenant.

Always review your lease’s “pest control” clause carefully. Even if the landlord pays for building-wide treatment, you may be responsible for the extensive preparation (washing/drying all fabrics, bagging belongings, moving furniture) and for replacing your own infested personal property.

Proactive Steps: Prevention and Action Plan

Given the high cost and stress of bed bug treatment and the lack of insurance coverage, prevention and a swift response plan are your best defenses.

Prevention Tips for Renters

- Inspect Second-Hand Items: Thoroughly check any used furniture, mattresses, or clothing before bringing them inside.

- Travel Vigilance: Inspect hotel room headboards, mattress seams, and luggage racks. Keep luggage on a stand away from beds/walls and wash all clothes in hot water upon returning home.

- Use Protective Covers: Encase mattresses and box springs in bed bug-proof covers.

- Reduce Clutter: Eliminate hiding spots around your bed and living area.

- Regular Inspection: Periodically check mattress seams, box spring edges, behind headboards, and in furniture crevices for signs (live bugs, shed skins, small dark fecal spots).

Immediate Action Plan if You Suspect Bed Bugs

1. Confirm the Infestation: Try to capture a bug for positive identification by a professional. Do not spread them by moving items to other rooms.

2. Notify Your Landlord in Writing: Send a dated letter or email immediately. This creates a legal record of notification.

3. Document Everything: Take photos/video of the bugs, signs of infestation, and any bites. Keep a log of all communications with the landlord.

4. Prepare for Professional Treatment: Follow the exterminator’s preparation instructions meticulously. Failure to prepare properly can lead to treatment failure and you being charged for repeat visits.

5. Know Your Rights: Research tenant laws in your city and state. Resources like the U.S. Environmental Protection Agency (EPA) bed bug page provide valuable information on treatment and legal frameworks.

Financial Planning: How to Handle the Costs

Since insurance won’t pay, you need a strategy to manage potential expenses. A robust renters insurance policy protects you from many disasters, but for bed bugs, you are your own first line of defense.

Estimating Potential Out-of-Pocket Costs

Be prepared for significant expenses:

- Professional Extermination: Can range from $500 to several thousand dollars for heat treatment or multiple chemical treatments, depending on unit size and severity.

- Replacing Belongings: Infested mattresses, furniture, and sometimes even electronics may need to be discarded. This can cost thousands.

- Laundry and Preparation: The cost of washing/drying all clothing, linens, and fabrics in hot water, plus purchasing sealable plastic bins and bags.

- Temporary Housing: If you must vacate, hotel costs are entirely on you.

Creating a “Pest Emergency Fund”

Given the high cost and low likelihood of insurance help, consider setting aside a small emergency fund specifically for potential pest issues. Even $500-1,000 can help cover initial inspection costs or replacement of essential items. This is a practical form of self-insurance for a common rental risk that traditional policies exclude. For other covered risks that do impact your finances, understanding the full renters insurance cost helps you balance your overall budget.

Conclusion

So, does renters insurance cover bed bugs? The clear, unambiguous answer is no. Bed bug infestations are a pervasive and expensive problem that fall squarely outside the scope of standard renters insurance due to their nature as a preventable maintenance issue. Renters must not rely on their insurance policy for financial rescue in this scenario. Instead, focus your energy on prevention, know your lease and local tenant laws regarding pest control responsibility, and act swiftly and decisively at the first sign of an issue. While a good renters insurance policy is indispensable for protecting you from fires, theft, and liability, it is not a cure-all. Being an informed and proactive tenant is your most powerful tool in the fight against bed bugs.

Frequently Asked Questions (FAQ)

Will renters insurance cover replacing my mattress if it has bed bugs?

No. Since the damage to the mattress is caused by the excluded peril (bed bug infestation), the cost to dispose of and replace the mattress is not covered by your renters insurance policy. You will be responsible for this cost out of pocket.

What if my neighbor’s bed bugs spread to my apartment?

This is a common situation, but it does not change the insurance coverage answer. Your renters insurance still excludes the infestation. However, it may strengthen your case that the landlord is responsible for the cost of building-wide extermination, as the source is likely in the building’s common areas or another unit. You must address this with your landlord, not your insurer.

Can I get a specific bed bug insurance rider or endorsement?

Generally, no. Insurance companies do not offer bed bug endorsements for standard renters policies because the risk is too common, gradual, and difficult to underwrite. The pest infestation exclusion is a foundational part of the policy that cannot be removed.

Does my landlord’s insurance cover bed bugs?

It’s unlikely. A landlord’s commercial property insurance covers the building structure and their liability, but it typically contains the same exclusions for vermin and infestations as renters insurance. The cost of pest control is usually considered a routine operating expense the landlord must budget for, not an insurable event.

What should I do first if I find bed bugs?

1. Do not panic or start moving items to other rooms.

2. Document the evidence with photos/video.

3. Immediately notify your landlord or property manager in writing.

4. Research reputable, licensed pest control companies in your area.

5. Begin preparing for treatment as advised, such as bagging linens and clothing.

Are there any insurance policies that cover bed bugs?

Virtually no standard property or renters insurance policies cover bed bugs. In rare cases, a specialized commercial policy for hotels or multi-family housing might have some limited coverage options, but these are not available to individual tenants. For renters, there is no practical insurance solution for this risk.

How can I prove I didn’t cause the infestation?

Proof is challenging but can be supported by: a clean move-in inspection report, prompt reporting of the issue, evidence of infestation in common areas or neighboring units, and demonstrating that you follow preventative practices (like using mattress encasements and inspecting second-hand furniture). Your credibility and timeliness in reporting are often the biggest factors.