The answer to “does renters insurance cover property damage” is a resounding yes—it is one of the core functions of the policy. Renters insurance provides financial protection for your personal property—your belongings—against damage or destruction caused by a wide range of named perils, also known as “covered causes of loss.” This includes damage from fire, smoke, lightning, windstorms, hail, theft, vandalism, and sudden water discharge (like a burst pipe). However, it’s crucial to understand that it covers your property, not the physical structure of the rental building itself (that’s your landlord’s responsibility). Coverage is subject to your policy’s limits, a deductible, and specific exclusions for perils like floods and earthquakes. Understanding what is covered, how claims are paid (Actual Cash Value vs. Replacement Cost), and the process for filing a claim is essential for every tenant to ensure they can recover financially after a damaging event.

What Types of Property Damage Are Covered?

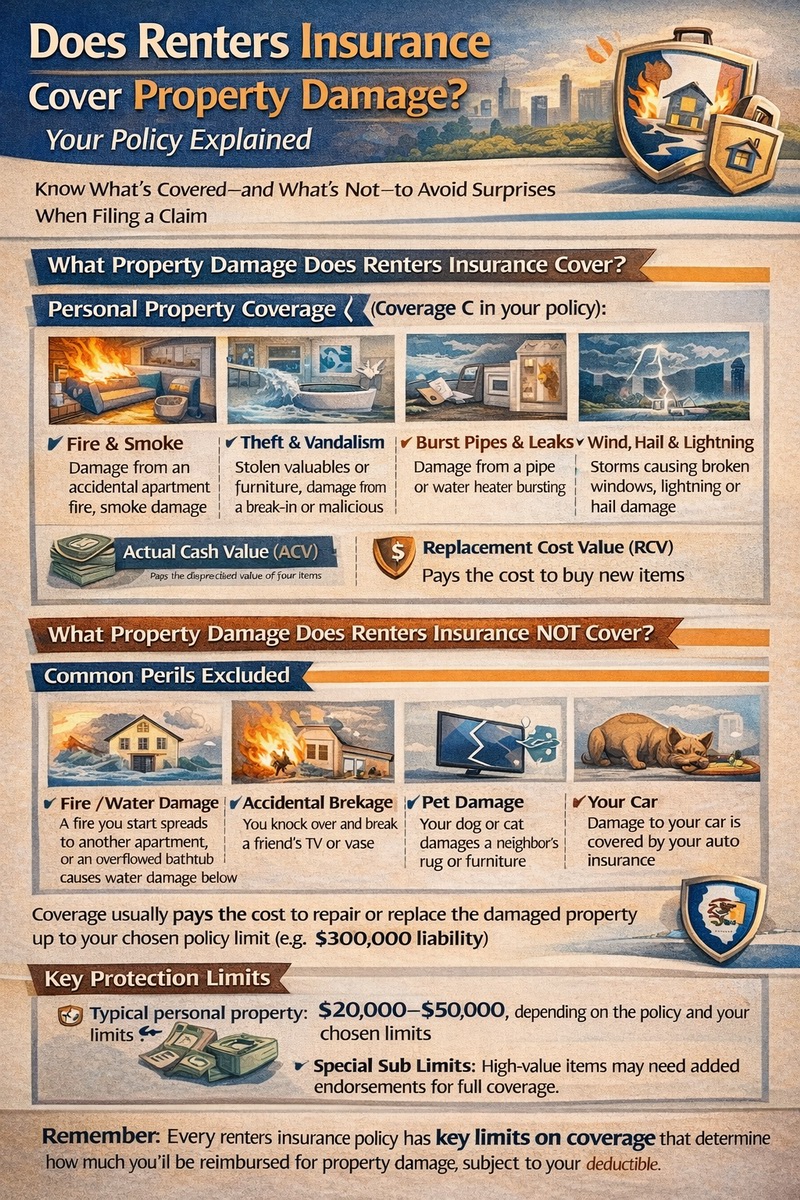

Standard renters insurance policies operate on a “named perils” basis, meaning they explicitly list the causes of damage that are covered. When asking “does renters insurance cover property damage,” you are asking if the cause is on that list. The good news is that the list includes the most common and devastating events that can befall your belongings. A typical renters insurance policy covers damage caused by:

- Fire and Lightning: Damage from a house fire, electrical fire, or lightning strike.

- Windstorm and Hail: Damage from tornadoes, hurricanes, straight-line winds, and hail.

- Explosion: Damage from any sudden explosion.

- Smoke: Sudden and accidental damage from smoke (not from gradual soot buildup).

- Theft: Property stolen from your home or even your car (off-premises coverage).

- Vandalism and Malicious Mischief: Intentional damage to your property by others.

- Falling Objects: Damage caused by something falling onto your property (e.g., a tree limb through the roof damaging your furniture).

- Weight of Ice, Snow, or Sleet: Collapse damage from the weight of winter precipitation.

- Sudden & Accidental Water Discharge: This includes water overflow or discharge from plumbing, heating, or air conditioning systems (e.g., a burst pipe or overflowing washing machine).

- Electrical Surge Damage: Sudden, accidental damage from artificially generated electrical current (like a power surge from a lightning strike).

Understanding “Named Perils” vs. “Open Perils”

Most basic renters policies are “named perils” for your personal property. This is the list-based approach described above. Some insurers offer more expensive “open perils” or “all-risk” coverage for personal property, which flips the logic: it covers all causes of loss except those specifically excluded (like flood or earthquake). For most renters, the named perils policy provides ample coverage for common disasters.

Real-World Examples of Covered Damage

- A kitchen fire ruins your furniture and electronics with smoke and fire damage.

- A burglar breaks in, smashes a window, and steals your laptop and jewelry.

- A severe thunderstorm with hail breaks your windows, allowing rain to soak and ruin your sofa and rug.

- A pipe freezes and bursts in the wall, flooding your apartment and damaging your book collection and bed frame.

- A tree limb crashes through your bedroom window during a windstorm, destroying your dresser and clothing.

In all these cases, your renters insurance would cover the repair or replacement cost of your damaged personal property, minus your deductible. For a comprehensive look at these coverages, see our guide on renters insurance coverage.

Sewer BackupUsually NO (unless added)Often excluded but can be added as a “water backup” endorsement for a small fee.

| Cause of Damage | Typically Covered? | Important Notes & Exceptions |

|---|---|---|

| Fire/Smoke | YES | One of the most common and critical coverages. |

| Theft/Burglary | YES | Includes theft from your home, car, or storage unit. A police report is usually required. |

| Burst Pipe (Sudden) | YES | Covers water damage to your belongings. Does not cover the source of the leak (landlord’s responsibility). |

| Windstorm/Hail | YES | Covers damage from the storm itself. Does not cover flood water from the storm. |

| Flood | NO | Requires a separate flood insurance policy from the NFIP or private insurer. |

| Earthquake | NO | Requires a separate earthquake endorsement or policy. |

| Normal Wear & Tear | NO | Damage from gradual deterioration, aging, or poor maintenance is excluded. |

| Insect/Rodent Infestation | NO | Damage from bed bugs, termites, mice, etc., is considered a maintenance issue. |

Key Limitations, Exclusions, and Financial Terms

While the coverage is broad, it is not unlimited. Understanding the financial structure and common exclusions is key to setting realistic expectations.

Coverage Limits and Sublimits

Your policy has a total personal property limit (e.g., $20,000). This is the maximum it will pay for all items in a single loss event. More importantly, policies have “sublimits” or “special limits of liability” for certain high-value categories:

- Jewelry, Watches, Furs: Often limited to $1,500 – $2,500 total for theft.

- Silverware/Goldware: Often limited to $2,500 – $5,000.

- Firearms: Often limited to $2,000 – $3,000.

- Business Property: Equipment used for business at home may have a sublimit (e.g., $2,500).

- Cash, Precious Metals: Very low limits, often $200 – $500.

To fully cover items that exceed these sublimits, you must “schedule” them by adding a rider or endorsement with a specific appraised value.

Actual Cash Value vs. Replacement Cost Coverage

This is a critical distinction that drastically affects your claim payout.

- Actual Cash Value (ACV): The default for many basic policies. Pays the replacement cost of an item minus depreciation (age, wear, and tear). A 5-year-old TV might only get you $150, not the $800 needed to buy a new one.

- Replacement Cost Value (RCV): A valuable endorsement. Pays the full cost to replace the damaged item with a new one of similar kind and quality, without deducting for depreciation. This is the recommended choice for full financial recovery.

The difference in payout can be thousands of dollars. Always check which valuation method your policy uses. Understanding this choice is a major part of evaluating your overall renters insurance cost and value.

The Deductible

This is the amount you pay out-of-pocket on each claim before insurance kicks in. Common deductibles are $500 or $1,000. If you have $2,000 in damage and a $500 deductible, the insurer pays $1,500. Choosing a higher deductible lowers your premium but increases your out-of-pocket cost when you file a claim.

The Claims Process for Property Damage

Knowing how to properly file a claim ensures you get the maximum entitled benefit in the shortest time.

Step 1: Immediate Actions After Damage Occurs

- Ensure Safety: In case of fire, flood, or structural damage, ensure everyone is safe and evacuate if necessary.

- Mitigate Further Damage: Take reasonable steps to prevent additional loss (e.g., put a tarp over a broken window, move dry items away from water). Keep receipts for any materials purchased for temporary repairs.

- Document Everything: Before cleaning up, take extensive photos and video of all damaged property and the overall scene. This is your most important evidence.

- Prepare an Inventory: Make a detailed list of damaged items, including descriptions, approximate age, original cost, and estimated replacement cost.

Step 2: Contacting Your Insurance Company

Report the claim to your insurer as soon as possible. Provide them with:

- Your policy number.

- The date and cause of the loss.

- A general description of the damage.

- The police report number, if theft or vandalism was involved.

They will assign a claims adjuster who will contact you to investigate, possibly visit the site, and review your documentation.

Step 3: Working with the Adjuster and Receiving Payment

The adjuster will determine if the cause is covered, assess the value of your loss (using ACV or RCV), and apply your deductible. For an ACV policy, you’ll receive a check for the depreciated amount. For an RCV policy, you may receive an initial ACV payment, and then a second payment for the “recoverable depreciation” after you actually replace the items and submit receipts. Do not discard severely damaged items until the adjuster has seen them.

What Renters Insurance Does NOT Cover (Key Exclusions)

To fully answer “does renters insurance cover property damage,” you must know the common exclusions. These typically require separate policies or are considered the responsibility of the tenant or landlord through maintenance.

Major Excluded Perils

- Floods: Surface water, overflowing rivers, storm surge. Must purchase separate flood insurance.

- Earthquakes & Earth Movement: Requires a separate endorsement or policy.

- Neglect & Intentional Damage: Damage you intentionally cause or allow to happen through neglect.

- Power Failure: Loss due to failure of power or utility services, if the failure originates off-premises.

- War & Nuclear Hazard: Standard exclusion in all property policies.

Damage to the Building and Others’ Property

Renters insurance covers your stuff, not the building. Damage to the apartment’s walls, floors, built-in appliances, or plumbing systems is the landlord’s responsibility, covered by their commercial property insurance. Similarly, damage you cause to a neighbor’s property (like a fire that spreads) would fall under your liability coverage, not your personal property coverage. For liability insights, you can refer to resources from the Insurance Information Institute.

Conclusion

So, does renters insurance cover property damage? Absolutely. It is the primary mechanism to protect your financial investment in everything you own from a wide array of common disasters. The key to maximizing this protection lies in understanding the named perils, ensuring you have adequate coverage limits, opting for Replacement Cost Value, and being aware of the exclusions so you can fill gaps with additional policies if needed. A well-structured renters insurance policy is your best defense against the unexpected, providing the funds to replace your belongings and get your life back on track after a loss. Don’t wait for disaster to strike—review your renters insurance policy today to ensure your property is fully protected.

Frequently Asked Questions (FAQ)

Does renters insurance cover water damage from a leaky roof?

It depends on the cause and suddenness. If the roof leaks during a heavy rainstorm (a windstorm peril) and water damages your belongings, that is likely covered. However, if the leak is due to long-term wear and tear or poor maintenance of the roof, the damage to your property may be denied as it resulted from an excluded “maintenance” issue. The repair to the roof itself is always the landlord’s responsibility.

Will renters insurance replace my items with new ones?

Only if you have Replacement Cost Value (RCV) coverage. The standard Actual Cash Value (ACV) coverage will only pay the depreciated value of your items. For example, ACV would give you $100 for a 5-year-old microwave, while RCV would give you $150 to buy a new comparable model. Always choose RCV if available.

Are my belongings covered if they’re damaged outside my home?

Yes, most policies include “off-premises” coverage. This means your belongings are protected against covered perils anywhere in the world. If your laptop is stolen from your car or a hotel room, or damaged by a fire in a friend’s house, your renters insurance would typically cover the loss, subject to your deductible and limits.

Does it cover damage from pests like bed bugs or rodents?

No. Damage from insects, rodents, or other pests (including bed bugs) is explicitly excluded from renters insurance. These are considered issues of maintenance, prevention, and sanitation. The cost of extermination and replacing infested items falls on you or, in some cases, your landlord depending on local law and the lease.

What if the property damage is my fault?

Renters insurance covers “sudden and accidental” damage, even if it results from your negligence. For example, if you accidentally leave a candle burning and start a fire, or overflow the bathtub, the resulting damage to your property is covered. However, intentional damage is never covered.

How do I prove what I owned and its value after a total loss?

This is why a home inventory is essential. The best proof is photos or video of your possessions, along with receipts, serial numbers, and model information. Store this inventory digitally (e.g., in cloud storage) so it survives a physical disaster. Without proof, you’ll have to rely on memory and the adjuster’s assessment, which may result in a lower settlement.

Does renters insurance cover natural disasters like hurricanes?

It covers the damage from the wind and hail of a hurricane, which would damage your belongings. However, it does not cover the flooding that often accompanies hurricanes. For flood coverage, you must purchase a separate flood insurance policy. This is a critical distinction for residents in flood-prone areas.