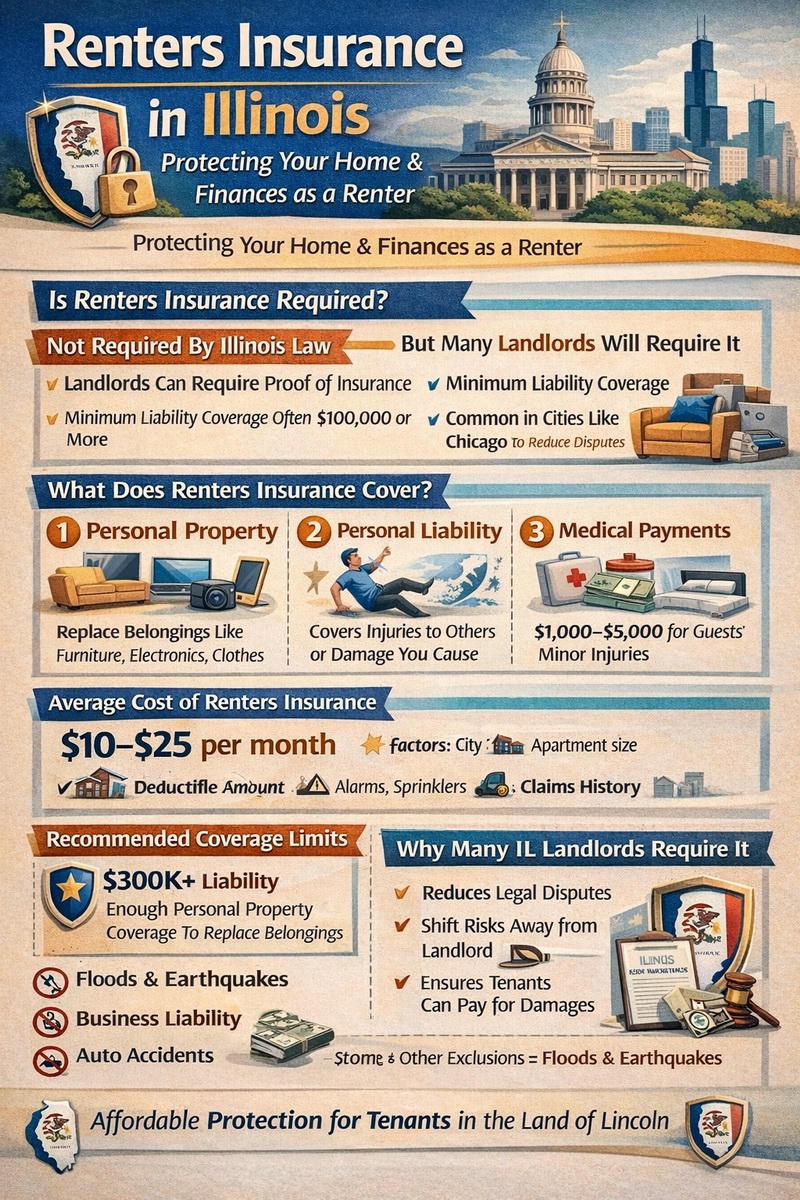

Renters insurance in Illinois is a critical, yet affordable, safeguard for tenants across the state, from the bustling streets of Chicago to the quiet towns of downstate. While Illinois law does not mandate renters insurance, a vast majority of landlords and property management companies require tenants to carry a policy, typically with minimum liability limits of $100,000. A standard policy protects your personal belongings from perils like fire, theft, and the severe weather Illinois is known for, including tornadoes and winter storms. It also provides essential personal liability coverage if someone is injured in your rental. The average cost in Illinois is competitive, often between $150-$250 per year, but varies significantly by location—Chicago premiums are higher than in Peoria or Springfield. This guide will navigate Illinois-specific risks, coverage needs, legal considerations, and provide actionable steps to find the right, cost-effective policy for your Illinois rental.

Why Renters Insurance is Essential in Illinois

For Illinois residents, renters insurance is not just a lease requirement; it’s a practical necessity driven by the state’s unique blend of urban density, volatile weather, and legal landscape. Illinois ranks high for tornado activity, experiences significant winter storms, and has major urban centers with higher crime rates. Furthermore, the state’s legal framework around landlord-tenant relationships makes liability protection crucial. A renters policy provides a financial safety net that shields you from unexpected losses, whether from a break-in in your Chicago apartment, a pipe bursting in your Carbondale rental during a freeze, or a guest injury in your Naperville condo.

Landlord Requirements and Lease Clauses

Most leases in Illinois, especially for professionally managed properties, include a clause requiring the tenant to obtain and maintain renters insurance. Common requirements are:

- Liability Coverage: A minimum of $100,000 (often $300,000 in newer or upscale buildings).

- Proof of Insurance: You must provide a certificate of insurance (declarations page) before move-in.

- Additional Insured/Interest: The landlord may require being listed as an “additional interest” or “interested party.” This means they get notified if your policy lapses but are not covered by it.

Failure to comply can result in fees, lease termination, or even eviction. Always read your lease’s insurance section carefully.

Illinois-Specific Risks to Insure Against

Your Illinois renters insurance policy should be evaluated against key regional risks:

- Tornadoes and Severe Thunderstorms: Illinois is in “Tornado Alley’s” doorstep. Wind and hail damage from these storms are covered under standard policies.

- Winter Weather: Freezing pipes, ice dams, and weight of snow can cause water damage. Burst pipes are typically covered, but gradual seepage is not.

- Urban Living Risks (Chicago, Rockford, Aurora): Higher theft/vandalism rates and greater fire risk in multi-unit buildings make personal property coverage vital.

- Foundation Water Seepage: Older buildings in areas like Chicagoland may have basement moisture issues; this is excluded and requires separate maintenance.

Understanding Coverage and Costs in Illinois

The cost and structure of renters insurance in Illinois are influenced by statewide factors and hyper-local variables. Understanding this helps you budget and shop effectively.

Average Cost Across the State

Illinois renters insurance premiums are generally near or slightly below the national average. According to industry data, the average annual premium ranges from $150 to $250. However, this is a broad estimate. Your actual cost depends on:

- Your City & ZIP Code: Crime rates, weather risk, and fire department proximity directly impact your rate.

- Coverage Limits & Deductible: Higher personal property or liability limits increase cost; a higher deductible lowers it.

- Building Type & Age: A newer building with sprinklers and security may qualify for discounts.

- Your Insurance/Claims History: A good credit-based insurance score can lower your premium in Illinois.

For a deeper dive into pricing factors, see our analysis of renters insurance cost.

Cost Comparison by Major Illinois City

Premiums can vary dramatically within the state:

| City/Region | Estimated Avg. Annual Premium | Primary Cost Drivers |

|---|---|---|

| Chicago | $180 – $300+ | Higher crime rates, dense population, greater fire risk in multi-unit buildings, higher liability claims. |

| Suburban Cook/DuPage Co. (e.g., Naperville, Schaumburg) | $150 – $220 | Lower crime than Chicago, but still subject to severe weather. Newer construction may offer discounts. |

| Peoria, Springfield, Rockford | $140 – $200 | Mid-sized city rates. Weather risks (tornadoes) remain a key factor. Generally lower crime. |

| Downstate/Rural Illinois | $130 – $180 | Lowest crime rates, but distance from fire hydrants/stations can increase risk scores. Tornado risk is pervasive. |

| University Towns (Champaign-Urbana, Bloomington-Normal, DeKalb) | $160 – $240 | Higher theft risk in student-heavy areas. Many leases near campuses mandate insurance. |

Always get multiple quotes to find the best rate for your exact location.

Key Coverages for Illinois Renters

Beyond the standard policy, Illinois tenants should pay special attention to certain coverages and endorsements due to local risks. A robust renters insurance coverage plan addresses these concerns.

Personal Property: Valuing Your Belongings Accurately

Illinois renters often underestimate the value of their possessions. Conduct a thorough home inventory. Pay special attention to:

- Electronics & Appliances: Standard in most apartments.

- Seasonal Gear: Winter clothing, sports equipment for summer and winter activities.

- Furniture: The cost to replace items new can be high.

Crucially, choose Replacement Cost Value (RCV) over Actual Cash Value (ACV). RCV pays to buy new items; ACV pays only depreciated value. For items like a 5-year-old TV, the difference in payout can be hundreds of dollars.

Liability Protection: A Non-Negotiable in Illinois

Given lease requirements and the litigious environment, do not skimp on liability. A minimum of $300,000 is strongly recommended, even if your lease only requires $100,000. This covers:

- Injuries to guests in your home (e.g., slip on ice you tracked in).

- Damage you accidentally cause to the building (e.g., a kitchen fire).

- Dog bite liability (subject to breed restrictions; Illinois has strict liability dog bite laws).

Additional Living Expenses (ALE) for Weather Disasters

If a tornado, fire, or major pipe burst makes your rental uninhabitable, ALE pays for hotel stays, meals, and other increased costs. Given Illinois’ weather, ensuring you have adequate ALE limits (often 20-30% of your personal property limit) is wise.

Endorsements to Consider in Illinois

- Sewer/Water Backup Coverage: Heavy rains in Illinois can overwhelm municipal sewer systems, causing backups into ground-floor units. This is excluded from standard policies but is a critical add-on, especially in older buildings in Chicago, Rockford, or the Metro East area.

- Scheduled Personal Property: For high-value items like jewelry, musical instruments, or fine art that exceed standard sub-limits.

- Identity Theft Coverage: Useful for urban and suburban residents alike.

Important Note: Standard renters insurance does NOT cover flood damage. For flood risk along the Mississippi, Illinois, or Fox Rivers, or in flood-prone areas like parts of Cook County, you need a separate policy from the National Flood Insurance Program (NFIP).

Navigating the Illinois Insurance Marketplace

Illinois has a competitive insurance market with national carriers, regional companies, and digital insurers all vying for business. Knowing how to shop can save you money.

Top Providers in Illinois

Major insurers like State Farm (headquartered in Bloomington, IL), Allstate, American Family, and Liberty Mutual have a strong presence. Digital providers like Lemonade and Progressive also offer competitive quotes. Consider:

- Local/Regional Agents: An independent agent can shop multiple companies for you and provide personalized advice on Illinois-specific risks.

- Direct Online Insurers: Often offer the fastest, most streamlined application and management process.

- Bundling: If you have auto insurance, bundling with the same company for renters insurance typically yields a discount of 10-20%.

How to Get the Best Rate

- Shop Around: Get at least 3-5 quotes. Prices for the same coverage can vary widely.

- Ask About All Discounts: Common discounts in Illinois include multi-policy, safety features (smoke alarms, deadbolts), claims-free, and paperless billing.

- Maintain Good Credit: Illinois allows insurers to use credit-based insurance scores. Improving your credit can lower your premium over time.

- Choose a Higher Deductible: Opting for a $1,000 instead of a $500 deductible can lower your premium, but ensure you can afford the higher out-of-pocket cost if you have a claim.

For authoritative information on shopping and understanding policies, resources like the Insurance Information Institute’s Illinois fact sheet are valuable.

Steps to Take Before and After You Buy

Securing your policy is just the beginning. Proper setup and knowing what to do in a disaster are key.

Before a Loss: Documentation and Preparation

- Create a Home Inventory: Use your phone to video each room, opening drawers and closets. Note high-value items and keep receipts.

- Understand Your Policy: Know your deductible, limits, and how to file a claim. Keep your insurer’s contact info handy.

- Meet Lease Requirements: Provide your landlord with the required certificate of insurance promptly.

- Prepare for Severe Weather: Have a plan for tornado warnings. Know where important documents and your inventory are stored (ideally digitally in the cloud).

After a Loss: Filing a Claim in Illinois

If disaster strikes:

- Ensure Safety & Mitigate Damage: Take reasonable steps to prevent further loss (e.g., put a tarp over a broken window).

- Document Everything: Take photos/video of all damage before cleaning up.

- Contact Your Insurer Immediately: Start the claims process. Have your policy number ready.

- Keep Records: Save all receipts for temporary repairs or additional living expenses.

- Cooperate with the Adjuster: They will assess the damage. Provide your inventory and documentation.

Conclusion

Renters insurance in Illinois is a small investment for monumental peace of mind. It fulfills common lease requirements, protects your financial future from liability lawsuits, and ensures you can recover from the property losses caused by the state’s unpredictable weather and other perils. By understanding the local cost factors, prioritizing key coverages like liability and water backup, and shopping wisely among Illinois’ many providers, you can secure robust protection that fits your budget. Don’t wait for a tornado warning or a break-in to realize the value of being insured. Take action today to protect your home and belongings with a comprehensive renters insurance policy tailored for life in the Prairie State.

Frequently Asked Questions (FAQ)

Is renters insurance required by law in Illinois?

No, Illinois state law does not require tenants to carry renters insurance. However, it is extremely common for landlords to require it as a condition of the lease. This requirement is legal and enforceable, so you must comply if it’s in your lease agreement.

Does renters insurance in Chicago cost more?

Yes, premiums in Chicago are typically higher than the Illinois state average due to higher population density, greater crime rates in certain areas, increased fire risk in older multi-unit buildings, and a higher frequency of liability claims. Shopping around is especially important in Chicago to find competitive rates.

Are tornadoes covered by standard renters insurance?

Yes, wind damage from tornadoes is covered under the standard “windstorm” peril in a renters insurance policy. This includes damage to your personal property from the tornado itself or from falling debris. It’s important to note that tornado-related flood damage would not be covered unless you have a separate flood insurance policy.

What is the “loss assessment” coverage I see on some policies?

Loss assessment coverage (often an add-on) can be important for renters in condos or cooperatives. If the building’s association has a master insurance policy and issues a special assessment to all unit owners for a covered loss (e.g., a deductible after a hailstorm damages the roof), this coverage can help pay your share. It’s less relevant for typical apartment renters.

Can my insurer cancel my policy after a tornado or hail claim?

In Illinois, an insurer cannot cancel a policy mid-term solely because you filed a claim. However, at renewal time, they may choose not to renew your policy based on your claims history. A single weather-related claim is less likely to trigger non-renewal than multiple claims, but it can affect your premium.

I’m a student at UIUC or ISU. Do I need my own policy?

If you live in university-owned housing (dorms), your parents’ homeowners insurance may extend to you with limitations. If you live off-campus in an apartment or rental house, you almost certainly need your own separate renters insurance policy. Your landlord will likely require it, and it’s necessary to protect your belongings and liability.

How do I prove I have insurance to my Chicago landlord?

Your insurance company will provide a “declarations page” or a “certificate of insurance” that shows your policy number, effective dates, coverage types, and limits. You simply need to provide a copy of this document to your landlord or management company, often via email or a tenant portal. They may also request to be listed as an “interested party.”