Replacement cost coverage renters insurance is a critical policy endorsement that ensures you receive the full amount needed to buy a brand-new equivalent of a lost or damaged item, without deduction for depreciation. Unlike standard “actual cash value” (ACV) coverage, which pays only the item’s current used-market worth, replacement cost coverage provides a true financial safety net, allowing you to rebuild your life with new possessions after a disaster. This coverage typically involves a two-step payment process: first, you receive the ACV amount, and after you actually replace the item and submit a receipt, you get the remaining balance to cover the full replacement cost. While it adds a modest amount to your premium—often just 10-20% more—the value is immense, especially for high-ticket electronics, furniture, and appliances. Every renter should evaluate this option to avoid being significantly underpaid at the time of a claim.

What Is Replacement Cost Coverage in Renters Insurance?

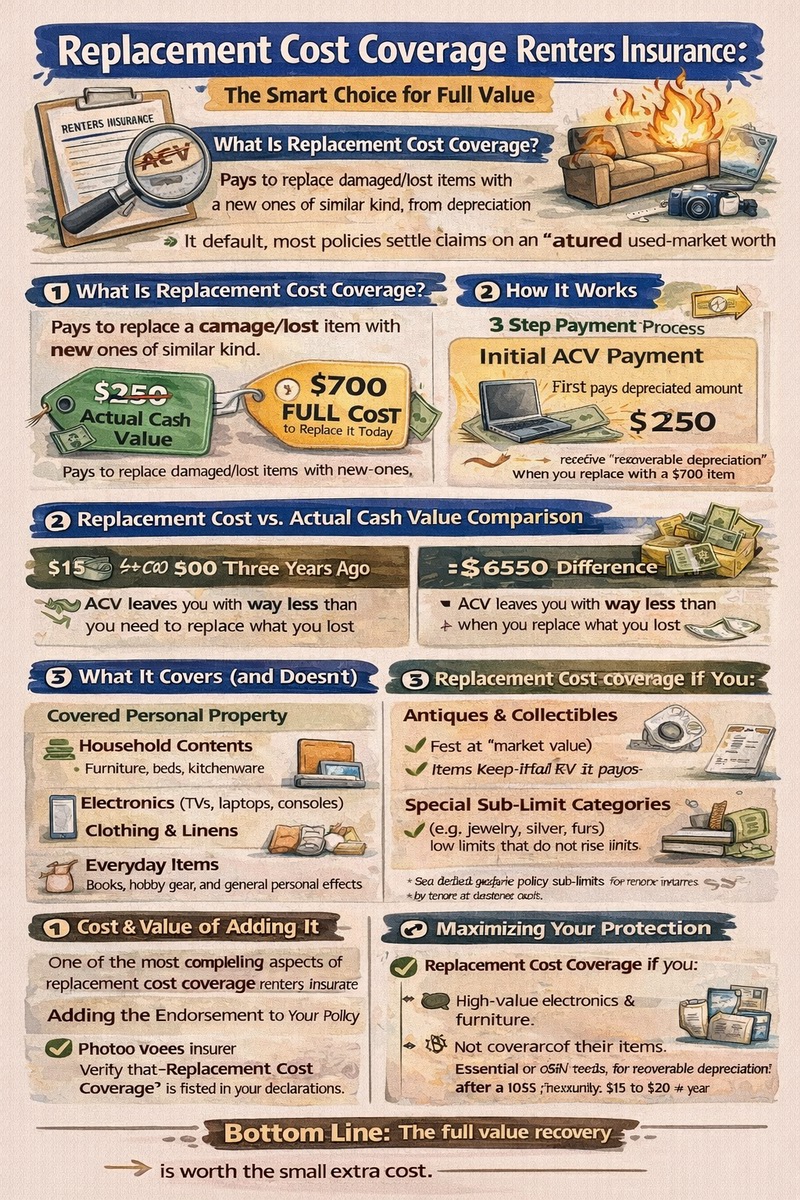

Replacement cost coverage is an optional but highly recommended add-on to a standard renters insurance policy that changes how your insurer values lost or damaged personal property. In its default state, most policies settle claims on an “actual cash value” basis, which factors in depreciation—the loss in value due to age, wear, and tear. Replacement cost coverage removes depreciation from the equation. It promises to pay you the cost to purchase a new item of similar kind and quality at today’s prices. This feature transforms your renters insurance from a partial reimbursement system into a full recovery tool, ensuring you are not financially penalized for the natural aging of your belongings after a covered loss like fire, theft, or water damage.

The Core Principle: Indemnification Without Depreciation

The fundamental purpose of insurance is “indemnification”—to restore you to the financial position you were in before the loss. Replacement cost coverage fulfills this principle more completely than ACV. For example, if a five-year-old television is stolen, ACV might pay you $150 based on its depreciated used value. Replacement cost coverage, however, would pay the $500 it costs to buy a comparable new TV, truly putting you back where you started. This distinction is the most significant financial decision you can make when structuring your policy.

How It Works: The Two-Payment Process

Claim settlements under replacement cost coverage typically follow a specific sequence:

- Initial ACV Payment: After a covered loss, the insurance company first calculates and pays you the actual cash value of the item (purchase price minus depreciation).

- Replacement and Reimbursement: You then go out and actually replace the item. You submit the receipt to your insurer.

- Recoverable Depreciation Payment: The company issues a second payment for the difference between the ACV and the full replacement cost, up to your policy limits.

There is usually a time limit to complete the replacement and submit receipts, commonly 180 days to one year. Understanding this process is key to maximizing your claim payout.

Replacement Cost vs. Actual Cash Value: A Critical Comparison

The choice between replacement cost coverage and actual cash value coverage has profound financial implications at claim time. Seeing the direct comparison highlights why the former is the superior choice for nearly all renters who can afford the slight premium increase.

Side-by-Scenario: A Living Room Fire

Imagine a fire damages your living room. Here’s how the two coverage types would handle the same items:

| Item | Purchased For / Age | Estimated ACV (Depreciated) | Replacement Cost (New Today) | ACV Payout | Replacement Cost Payout |

|---|---|---|---|---|---|

| Sofa | $1,200 / 4 years old | $400 | $1,400 | $400 | $1,400 (after replacement) |

| Laptop | $1,000 / 3 years old | $300 | $950 | $300 | $950 (after replacement) |

| Area Rug | $800 / 6 years old | $200 | $850 | $200 | $850 (after replacement) |

| Total for These Items | $900 | $3,200 |

As shown, the difference is staggering. The ACV payout of $900 leaves you unable to replace your items, forcing you to buy used or dip into savings. The replacement cost coverage payout of $3,200 allows you to fully restock your home with new equivalents.

The Hidden Impact of Depreciation

Depreciation schedules used by insurers can be harsh. Electronics and appliances can lose 20-40% of their value per year. Furniture depreciates based on a typical lifespan. Under ACV, you are essentially only insured for the “remaining useful life” of an item. After a total loss, replacement cost coverage renters insurance is the only way to avoid starting over with a collection of used, older items or a significant financial shortfall.

What Does Replacement Cost Coverage Actually Cover?

It’s important to understand the scope and limitations of this endorsement. Generally, it applies to the broad categories of personal property (Coverage C) listed in your policy, but with important nuances.

Covered Personal Property Categories

Replacement cost coverage typically applies to:

- Household Contents: Furniture, rugs, curtains, kitchenware, and appliances.

- Electronics: Televisions, computers, tablets, gaming systems, and audio equipment.

- Clothing and Linens: All articles of clothing, shoes, bedding, and towels.

- Everyday Items: Books, hobby equipment, and general personal effects.

The core rule is that the item must be replaced with one of “like kind and quality.” You can’t use a mattress claim to buy a luxury sports car, but you can upgrade from a basic model to a similar mid-tier model if the low-end one is no longer sold. For a full list of what’s included, review our guide to renters insurance coverage.

Common Exceptions and Special Limits

Replacement cost coverage usually does NOT apply to certain categories, which are often settled at ACV or have special rules:

- Antiques, Fine Art, and Collectibles: These items may not have a “new” equivalent. They often require a specialized appraisal and scheduled personal property coverage.

- Items Not Actually Replaced: If you choose to keep the cash from the initial ACV payment and not replace the item, you do not receive the recoverable depreciation.

- Property Subject to Special Sub-Limits: Categories like jewelry, watches, furs, and silverware often have low standard limits (e.g., $1,500 total). Replacement cost may apply up to that limit, but for full coverage of high-value items, you need to “schedule” them separately with an appraisal.

The Cost and Value of Adding This Coverage

One of the most compelling aspects of replacement cost coverage renters insurance is its high value relative to its cost. For most renters, the premium increase is a small price for a major upgrade in protection.

Typical Premium Increase

Adding replacement cost coverage to your personal property protection typically increases your annual premium by 10% to 20%. For example, if your base renters insurance policy costs $150 per year, adding this endorsement might raise it to $165-$180 annually—an increase of $15 to $30 per year, or about $1.25 to $2.50 per month. When weighed against the thousands of dollars in additional claim payout demonstrated in the table above, the return on investment is exceptionally high.

Factors Influencing the Cost

The exact cost depends on:

- Your Personal Property Limit: A higher limit means a slightly higher absolute dollar increase for the endorsement.

- Your Deductible: A higher deductible lowers your overall premium, which can make the relative cost of the endorsement slightly lower.

- Your Location and Insurer: Rates and endorsement pricing vary by state and by company. It’s always wise to get quotes that include this option. To understand how this fits into your overall budget, see our analysis of renters insurance cost factors.

Is It Worth It? A Resounding Yes for Most Renters

Unless you own almost no possessions or all your items are very old and you would be content with a cash settlement for their minimal used value, replacement cost coverage is worth it. It is particularly crucial for:

- Renters with newer, expensive electronics and furniture.

- Anyone who would struggle to pay the difference out-of-pocket to replace items new.

- Renters who want genuine peace of mind, knowing their policy will fully restore their standard of living after a loss.

How to Add and Use Replacement Cost Coverage

Securing and properly utilizing this coverage requires a few specific steps, from policy setup to the claims process.

Adding the Endorsement to Your Policy

Replacement cost coverage is not automatic. You must actively select it when purchasing a new policy or request an endorsement to an existing one. Contact your insurance agent or company and specifically ask to add “Replacement Cost Coverage” for your personal property (Coverage C). They will adjust your premium and issue a new declarations page or policy endorsement confirming the change. Verify that it appears on your documents.

The Claims Process: Maximizing Your Payout

To fully benefit from this coverage after a loss:

- File Your Claim as Usual: Report the loss and provide your inventory list with descriptions, ages, and original purchase prices if possible.

- Receive the ACV Payment: The insurer will send an initial check for the depreciated value.

- Replace the Items: Shop for and purchase replacements for your lost/damaged items. Keep meticulous records.

- Submit Receipts for Recoverable Depreciation: Send copies of the receipts to your claims adjuster. Be sure they detail the item purchased.

- Receive the Final Payment: The insurer will review the receipts and issue a second check for the difference, bringing your total compensation to the full replacement cost.

Maintain open communication with your adjuster and be aware of your policy’s deadline for submitting replacement receipts.

Supporting Your Claim with a Home Inventory

A detailed home inventory is the single best tool to support a replacement cost claim. It should include:

- Photos or videos of each room and individual high-value items.

- Receipts, serial numbers, and model numbers.

- Notes on purchase dates and prices.

Store this inventory digitally (e.g., in cloud storage) so it’s safe even if your home is destroyed. This documentation speeds up the claims process and provides proof of what you owned and its original value. Resources like the National Association of Insurance Commissioners (NAIC) offer free home inventory templates and apps.

Conclusion

Choosing replacement cost coverage renters insurance is one of the smartest financial decisions a renter can make. It closes the devastating gap between the depreciated value of your belongings and what it actually costs to replace them with new items after a disaster. For a minimal increase in your premium—often less than the cost of a few coffees per month—you secure a guarantee that your insurance will truly make you whole. Don’t let depreciation leave you underinsured. Review your current policy today, and if you don’t have this endorsement, contact your agent to add it immediately. Ensuring you have robust renters insurance with replacement cost coverage is the definitive step towards complete peace of mind and financial security in your rented home.

Frequently Asked Questions (FAQ)

Is replacement cost coverage worth it for older items?

Yes, it can still be valuable. While the recoverable depreciation on a 10-year-old couch might be small, the coverage still ensures you get the full cost of a comparable new couch, which is likely much more than its near-zero actual cash value. It protects you against inflation and ensures you can replace any item, regardless of age, with something new.

Does replacement cost coverage mean I get a brand new item for an old one?

Essentially, yes. The core principle is that you are reimbursed the amount of money required to purchase a new item of “like kind and quality” to replace the old one. It is not a payout for the old item’s sentimental value, but a financial mechanism to restore your tangible possessions with new equivalents.

Can I use the money to upgrade an item?

Typically, you are reimbursed for the cost of a “comparable” item. If your exact model is discontinued, you can usually buy the closest current equivalent. If you choose to buy a more expensive, upgraded model, the insurer will generally only pay up to the cost of the comparable item, leaving you to pay the price difference out of pocket.

Is there a time limit to replace items and get the depreciation back?

Yes, almost all policies impose a time limit. Common timeframes are 180 days (6 months) or one year from the date of loss. You must complete the replacement and submit receipts within this period to receive the recoverable depreciation payment. Check your specific policy wording for the exact deadline.

Does replacement cost coverage apply if my stuff is stolen?

Absolutely. Replacement cost coverage applies to all covered perils listed in your policy, which includes theft. If your laptop is stolen, the process is the same: you receive the ACV first, then buy a new laptop, submit the receipt, and receive the balance to cover the full replacement cost.

What if I can’t find a receipt for an item I need to replace?

While receipts are the best proof, they are not always mandatory. You can work with your claims adjuster and provide other evidence, such as a credit card statement showing the purchase, a photograph of the item in your home, or a link to a current retailer selling a comparable model. The adjuster will use this to estimate a fair replacement cost.

Does this coverage increase my personal property limit?

No. Replacement cost coverage changes the *valuation method*, not your *coverage limit*. Your policy’s personal property limit (e.g., $30,000) is the maximum total amount the insurer will pay for all items in a loss. Replacement cost ensures you get the full new-item value for each thing you claim, up to that overall limit.