Renters insurance in Virginia is a vital and often required protection for tenants across the Commonwealth, from the coastal cities of Virginia Beach and Norfolk to the urban hubs of Richmond and Arlington and the mountain towns of Roanoke. While Virginia state law does not mandate renters insurance, the overwhelming majority of landlords and property management companies include it as a mandatory lease clause, typically requiring liability limits of $100,000 or more. A standard policy protects your personal property against Virginia’s diverse risks, including hurricane wind on the coast, severe thunderstorms statewide, winter storms, and theft. Critically, it excludes flood damage, which is a significant risk in coastal and riverine areas, necessitating a separate NFIP policy. With average annual premiums ranging from a very affordable $140 in low-risk inland areas to $300+ in high-risk coastal cities, securing the right coverage is an essential and manageable step for financial security as a Virginia renter.

Why Renters Insurance is Essential in Virginia

Virginia’s diverse geography—spanning Atlantic coastline, Piedmont plains, and Appalachian mountains—creates a varied risk landscape that makes renters insurance a crucial safeguard. Furthermore, the state’s dense population centers and common legal practices make liability coverage non-negotiable. A robust policy serves as your financial first line of defense against property loss from natural disasters and provides essential legal protection if you’re found responsible for injury or damage in your rental.

Landlord Requirements and Virginia Lease Law

In Virginia, it is standard practice for leases to require tenants to carry renters insurance. Key requirements often include:

- Minimum Liability Coverage: Often $100,000, but $300,000 is common in newer apartment complexes, especially in Northern Virginia.

- Proof of Insurance: You must provide a certificate of insurance (declarations page) before move-in and upon renewal.

- Additional Interest Clause: The landlord will be named as an “additional interest” or “interested party,” so they receive notification of any policy changes or cancellations.

- Lease Enforcement: Failure to maintain required insurance is a lease violation, which can lead to fees, forced placement of a policy at your expense (often more costly), or eviction proceedings.

Always review the “Insurance” section of your Virginia lease carefully.

Virginia-Specific Risks to Insure Against

Your policy should be evaluated against regional perils:

- Hurricanes & Tropical Storms (Coastal & Tidewater): Wind and hail damage from storms is covered; storm surge flooding is NOT.

- Flooding: From coastal surge, river overflow (James, Potomac, Rappahannock), or flash floods. A SEPARATE flood insurance policy is required.

- Severe Thunderstorms & Tornadoes: Statewide risk for damaging wind, hail, and lightning.

- Winter Storms & Nor’easters: Can cause power outages, pipe bursts, and weight-of-snow damage.

- Theft: Urban areas like Richmond, Norfolk, and parts of Northern Virginia have higher property crime rates.

- Sinkholes: A rare but notable risk in certain geological areas of Virginia; typically excluded and may require a separate endorsement.

Understanding Coverage, Costs, and Flood Insurance in VA

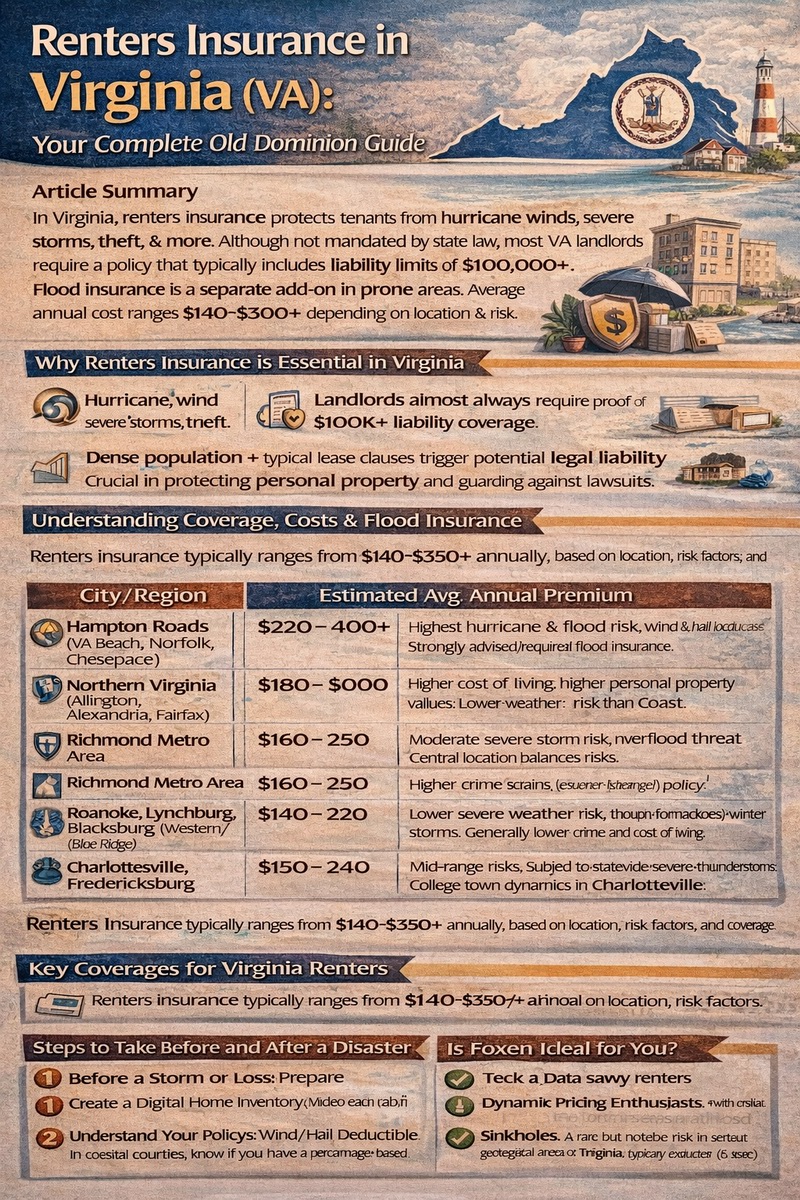

The cost of renters insurance in Virginia varies significantly from the coast to the mountains, largely driven by catastrophe risk. Understanding these variables is key to finding adequate and affordable protection.

Average Cost Across the Commonwealth

Virginia’s average premiums are often slightly below the national average due to competitive markets and generally moderate risk inland. Annual costs typically range from $140 to $350. Key factors include:

- Proximity to the Coast: Hampton Roads (Virginia Beach, Norfolk, Newport News) and the Eastern Shore have the highest premiums due to hurricane risk.

- Flood Zone: Living in a FEMA-designated Special Flood Hazard Area (SFHA), common in coastal and river-adjacent areas, necessitates separate flood insurance and can impact overall risk assessment.

- Urban vs. Rural: Higher crime and claim frequency in dense urban areas increase costs.

- Building Features: Newer construction, security systems, and storm shutters may qualify for discounts.

- Your Coverage Selections: Limits, deductible, and choosing Replacement Cost over Actual Cash Value.

For more on pricing factors, see our overview of renters insurance cost.

Cost Comparison by Major Virginia Region

| City/Region | Estimated Avg. Annual Premium | Primary Cost & Risk Drivers |

|---|---|---|

| Hampton Roads (VA Beach, Norfolk, Chesapeake) | $220 – $400+ | Highest hurricane & flood risk. Potential for wind/hail deductibles. Flood insurance is strongly recommended/mandatory. |

| Northern Virginia (Arlington, Alexandria, Fairfax) | $180 – $300 | High cost of living, higher personal property values, elevated theft risk. Lower weather risk than coast. |

| Richmond Metro Area | $160 – $250 | Moderate severe storm risk, river flood risk (separate policy needed), urban theft. Central location balances risks. |

| Roanoke, Lynchburg, Blacksburg (Western/Blue Ridge) | $140 – $220 | Lower severe weather risk, though tornadoes and winter storms occur. Generally lower crime and cost of living. |

| Charlottesville, Fredericksburg | $150 – $240 | Mid-range risks. Subject to statewide severe thunderstorms. College town dynamics in Charlottesville. |

Always obtain personalized quotes, as rates can vary by neighborhood.

The Critical Flood Insurance Need in Virginia

Virginia has extensive flood risk, not just on the coast. Key areas include:

- Coastal Tidewater: Storm surge from hurricanes and nor’easters.

- Riverine Floodplains: The James, Potomac, Rappahannock, Shenandoah, and other rivers can overflow.

- Urban Flash Flooding: Heavy rains can overwhelm drainage in cities like Richmond and Roanoke.

Standard renters insurance explicitly excludes flood. Coverage must be purchased separately through the National Flood Insurance Program (NFIP) or a private insurer. Check your address on FEMA’s Flood Maps. Landlords in Special Flood Hazard Areas often require tenants to carry contents-only flood insurance.

Key Coverages for Virginia Renters

To build a robust safety net, Virginia tenants should prioritize specific coverages within their policy. A comprehensive renters insurance coverage plan addresses the Commonwealth’s unique exposures.

Personal Property with Replacement Cost

Opt for Replacement Cost Value (RCV) coverage. It pays to buy new items, unlike Actual Cash Value (ACV) which deducts depreciation. After a total loss from a hurricane or fire, RCV is essential for full recovery. Conduct a detailed home inventory, especially for electronics, furniture, and clothing.

High Liability Limits

Given common lease requirements and Virginia’s legal environment, carry at least $300,000 in personal liability coverage. This protects you if you are found liable for an injury in your home or accidentally cause damage to the rental property (e.g., a kitchen fire).

Loss of Use / Additional Living Expenses (ALE)

If a covered disaster displaces you, ALE pays for hotel, meals, and storage. Given that hurricane or fire repairs can take months, ensure your ALE limit (typically 20-30% of personal property coverage) is adequate for a potentially long displacement in Virginia’s rental market.

Essential Endorsements for Virginia

- Sewer/Water Backup Coverage: Heavy rains can overload systems, causing backups. This is excluded from standard policies but is a critical, affordable add-on, especially in older areas of Richmond, Norfolk, and Alexandria.

- Increased Special Limits: Consider raising sublimits for valuable items like jewelry, electronics, or musical instruments if you own items that exceed the standard caps.

- Ordinance or Law Coverage (for older buildings): If your historic rental must be rebuilt to modern codes after a loss, this can help cover increased costs that affect your loss of use period.

Navigating the Virginia Insurance Marketplace

Virginia has a competitive insurance market with many strong regional and national carriers. Knowing how to shop can optimize both price and coverage.

Top Providers in Virginia

National carriers like State Farm, Allstate, Nationwide, and Liberty Mutual have a strong presence. Virginia also has excellent regional companies like Erie Insurance (in Northern VA) and Virginia Mutual. For coastal coverage, companies like Chubb or specialized MGAs may be involved. The Virginia Property Insurance Association (VPIA) is the state’s insurer of last resort for wind/hail in coastal areas if you are denied in the voluntary market.

How to Get the Best Rate and Coverage

- Shop with Independent Agents: Particularly in coastal areas, an independent agent can access multiple markets, including specialty carriers, and advise on wind deductibles and flood insurance.

- Bundle Policies: Combining renters and auto insurance with the same company typically yields a 15-25% discount.

- Ask About Mitigation Discounts: Hurricane shutters, storm-resistant features, security systems, and smoke alarms can lower premiums.

- Maintain Good Credit: Virginia allows insurers to use credit-based insurance scores. Good credit can significantly lower your rate.

- Choose a Higher Deductible: Opting for a higher standard or wind deductible lowers your premium but increases out-of-pocket cost per claim.

For authoritative information on flood risks, consult FEMA’s Flood Insurance page and the Virginia Department of Insurance.

Steps to Take Before and After a Disaster

Preparation is paramount in a state vulnerable to hurricanes and severe storms. Knowing the claims process ensures a smoother recovery.

Before a Storm or Loss: Virginia-Specific Prep

- Create a Digital Home Inventory: Video each room and store the file in the cloud.

- Understand Your Policy’s Wind/Hail Deductible: In coastal counties, know if you have a percentage-based hurricane deductible.

- Know Your Flood Zone & Insurance: Have your NFIP policy number and agent contact handy if applicable.

- Prepare an Evacuation/Go-Bag: Include insurance documents, inventory, medications, and essentials.

After a Loss: Filing a Claim in Virginia

If disaster strikes:

- Ensure Safety & Mitigate Damage: Take reasonable steps to prevent further loss (tarp roof, move wet items). Keep receipts.

- Document Everything: Take extensive photos/video of all damage before cleanup.

- Contact Your Insurer Immediately: Start the claims process. Use their app if available.

- File Separate Claims if Needed: For flood damage, file a claim with your flood insurer. For wind damage, file with your renters insurer.

- Keep Detailed Records: Log all communications with adjusters, contractors, and your landlord. Save all receipts for ALE.

Post-disaster, adjusters are overwhelmed; patience and organization are key.

Conclusion

Renters insurance in Virginia is an indispensable, affordable, and often required component of responsible tenancy. It provides the financial backbone to recover from the state’s varied weather risks and protects against significant liability exposures. The cardinal rule for Virginia renters is to understand the stark divide between wind coverage (included) and flood coverage (separate), especially in coastal and river-adjacent communities. By securing adequate liability limits, opting for Replacement Cost coverage, and considering essential endorsements like water backup, you can tailor a policy that offers true peace of mind. Whether you’re in a high-rise in Arlington, a historic apartment in Richmond, or a beachside condo in Virginia Beach, a well-structured renters insurance policy—paired with flood insurance if needed—is your best strategy for safeguarding your financial future in the Old Dominion.

Frequently Asked Questions (FAQ)

Is renters insurance required by law in Virginia?

No, Virginia state law does not require tenants to carry renters insurance. However, it is standard and nearly universal for landlords to require it as a condition of the lease. You are contractually obligated to comply with your lease’s insurance clause.

Do I need flood insurance in Northern Virginia or Richmond?

Potentially, yes. Flood risk is not limited to the coast. The Potomac River can flood areas in Northern VA, and the James River poses a significant flood risk to parts of Richmond. Heavy rainfall can cause flash flooding anywhere. Check FEMA’s flood maps for your exact address; many are surprised to find they are in a high-risk zone.

What is a “hurricane deductible” in Virginia?

In coastal counties, insurers may apply a separate, higher deductible for damage caused by a named hurricane. It’s often a percentage (e.g., 2-5%) of your insured personal property value, not a flat fee. For example, if your belongings are insured for $25,000 with a 2% hurricane deductible, you’d pay the first $500 of hurricane damage. This is common in Hampton Roads and the Eastern Shore.

Are tornadoes covered by renters insurance in Virginia?

Yes. Tornado damage is covered under the standard “windstorm” peril in a renters insurance policy. Damage to your personal property from tornado winds or debris is covered, subject to your policy’s deductible. Tornadoes would not trigger a “hurricane deductible” unless they were part of a named hurricane event.

I’m a student at UVA, VT, VCU, or GMU. Do I need my own policy?

If you live off-campus in a house or apartment, yes, you absolutely need your own renters insurance policy, and your lease will likely require it. If you live in a university dormitory, your parents’ homeowners policy may extend limited coverage, but it’s often inadequate for a student’s valuable electronics and liability. A separate student renters policy is affordable and recommended.

Can my insurer cancel my policy after a hurricane or bad claim?

In Virginia, an insurer cannot cancel a policy mid-term due to a weather-related claim. However, at renewal time, they may choose not to renew your policy based on their overall risk assessment, which could include your claims history. If you are non-renewed in a coastal area, you may need to seek coverage through the Virginia Property Insurance Association (VPIA).

How do I prove I have insurance to my Northern Virginia landlord?

Your insurer provides a “declarations page” or “certificate of insurance.” You will email or upload a copy of this document to your landlord or property management company. They will also require being listed as an “additional interest” on the policy, which you arrange when purchasing the insurance.