Renters insurance in Arkansas is a crucial and affordable safeguard for tenants, offering vital protection against the state’s significant severe weather risks, including tornadoes, severe thunderstorms, hail, and flash flooding. While Arkansas law does not mandate renters insurance, the majority of landlords, especially property management companies, require tenants to carry a policy with minimum liability limits, often $100,000. A standard policy covers your personal property from these perils and provides essential liability protection if someone is injured in your rental. The average cost is very reasonable, typically ranging from $130 to $250 per year, making it one of the more affordable states for coverage. However, understanding specific exclusions—like flood damage, which requires separate insurance—and ensuring adequate coverage limits for tornado-prone areas are key steps for every Arkansas renter to ensure complete financial security.

Why Renters Insurance is Non-Negotiable in Arkansas

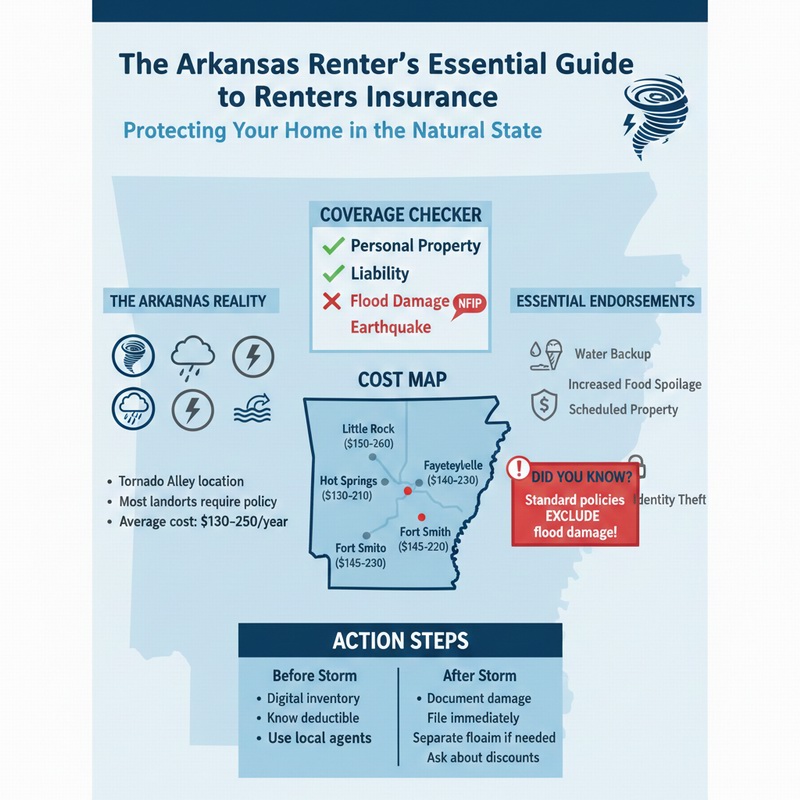

Arkansas’s location in “Tornado Alley” and its vulnerability to severe thunderstorms, straight-line winds, and hail make renters insurance an essential financial safety net for tenants. The state experiences a high frequency of weather-related property claims. Beyond weather, Arkansas’s lease norms and legal landscape make liability coverage a standard requirement. A robust policy ensures you can recover from property losses caused by Arkansas’s volatile climate and protects your assets from lawsuits arising from incidents in your rented home.

Landlord Requirements and Common Lease Clauses

Most professionally managed rental properties in Arkansas include a renters insurance requirement. Standard lease clauses stipulate:

- Minimum Liability Coverage: Often $100,000, though $300,000 is becoming more common in newer complexes.

- Proof of Insurance: You must provide a certificate of insurance (declarations page) before move-in and upon renewal.

- Additional Interest Designation: The landlord is listed as an “additional interest” or “interested party,” meaning they receive notice of policy cancellation or lapse.

- Consequences for Non-Compliance: Failure to maintain coverage can result in fees, lease termination, or the landlord force-placing a policy on your behalf at a much higher cost.

Always review your lease’s “Insurance” section thoroughly.

Arkansas-Specific Risks to Insure Against

Your policy must be evaluated against the Natural State’s prominent perils:

- Tornadoes and Derechos: Arkansas ranks high for tornado activity. Wind damage from these events is a covered peril.

- Severe Thunderstorms & Hail: Frequent storms bring damaging hail (often baseball-sized) and straight-line winds.

- Flash Flooding & River Flooding: Heavy rains can cause sudden flooding. This is EXCLUDED from standard policies and requires separate flood insurance.

- Lightning Strikes: Can cause fire and power surge damage to electronics.

- Winter Ice Storms: Can cause power outages, pipe bursts, and falling tree limbs.

- Theft and Vandalism: While generally lower than national averages, urban areas like Little Rock have higher property crime rates.

Understanding Coverage, Costs, and the Flood Exclusion

The cost of renters insurance in Arkansas is heavily influenced by the state’s severe weather risk, but remains relatively low due to a lower overall cost of living. Understanding the distinct coverage for wind vs. water is paramount.

Average Cost Across the State

Arkansas boasts some of the most affordable renters insurance premiums in the nation. The average annual cost ranges from $130 to $250. Key factors include:

- Location & Storm Frequency: Areas with higher historical tornado/hail activity (Central and Eastern AR) may see slightly higher rates.

- Proximity to Flood Zones: Living near rivers like the Arkansas, Mississippi, or White River can indicate flood risk but doesn’t directly affect standard policy premiums.

- Crime Rates: Urban centers typically have higher premiums than rural areas.

- Coverage Choices: Your selected personal property limit, liability limit, deductible, and whether you choose Replacement Cost Value (RCV).

- Building Age & Features: Updated wiring, security systems, and storm shutters may qualify for discounts.

For a deeper look at pricing, see our guide on renters insurance cost.

Cost Comparison by Major Arkansas Region

| City/Region | Estimated Avg. Annual Premium | Primary Cost & Risk Drivers |

|---|---|---|

| Little Rock Metro Area | $150 – $260 | Highest severe weather risk in the state, urban theft, and higher property values. Central location in tornado alley. |

| Northwest AR (Fayetteville, Springdale, Bentonville) | $140 – $230 | Growing urban area with somewhat lower severe weather risk than central AR, but still significant. Higher cost of living. |

| Fort Smith River Valley | $135 – $220 | Moderate severe weather risk, some flood risk from the Arkansas River. Lower cost of living. |

| Jonesboro, Northeast AR | $140 – $240 | High tornado and severe thunderstorm risk in the Mississippi Delta region. |

| Hot Springs, Southwest AR | $130 – $210 | Moderate severe weather risk, lower population density and crime. |

Always get personalized quotes for your exact address.

The Critical Flood Insurance Consideration

Standard renters insurance in Arkansas covers wind-driven rain from a storm but excludes flooding from overflowing rivers, lakes, or ground saturation. Given Arkansas’s many rivers and potential for flash floods, tenants in flood-prone areas need separate coverage through the National Flood Insurance Program (NFIP). This is especially important for rentals near the Arkansas, Mississippi, Ouachita, or Red Rivers, or in low-lying areas. Check FEMA’s Flood Maps to assess your risk.

Key Coverages for Arkansas Renters

To build a resilient financial plan, Arkansas tenants should prioritize specific coverages within their policy. A comprehensive renters insurance coverage plan addresses the state’s unique exposures.

Personal Property with Replacement Cost

After a tornado or hail storm, you need to replace items new. Choose Replacement Cost Value (RCV) coverage, not Actual Cash Value (ACV). ACV deducts depreciation, leaving you with far less money to rebuild. Conduct a detailed home inventory; tornadoes can cause total losses.

High Liability Limits

With common lease requirements and potential risks, carry at least $300,000 in personal liability coverage. This protects you if you’re found liable for an injury in your home or accidentally cause damage (like a kitchen fire) to the rental property.

Loss of Use / Additional Living Expenses (ALE)

If a tornado or fire makes your rental uninhabitable, ALE pays for hotel, meals, and storage. Given that repairs after major storms can be lengthy, ensure your ALE limit (typically 20-30% of your personal property coverage) is sufficient for a potentially extended displacement.

Essential Endorsements for Arkansas

- Sewer/Water Backup Coverage: Heavy rains can overwhelm municipal systems, causing backups into ground-floor or basement units. This is excluded from standard policies but is a critical, affordable add-on.

- Increased Food Spoilage Limit: Power outages from severe storms are common. Increase the small standard limit for refrigerator/freezer contents.

- Scheduled Personal Property: For high-value items like jewelry, firearms, or musical instruments that exceed standard sub-limits.

- Identity Theft Coverage: Helpful for all renters, available as a low-cost endorsement.

Navigating the Arkansas Insurance Marketplace

Arkansas has a stable insurance market with strong regional and national carriers. Smart shopping can optimize your coverage and cost.

Top Providers in Arkansas

National carriers like State Farm, Allstate, Farmers, and Liberty Mutual have a strong presence. Arkansas also has excellent regional companies like Southern Farm Bureau Casualty Insurance (very popular in AR) and Arkansas Mutual. For high-risk areas, the Arkansas Insurance Department facilitates a residual market if needed.

How to Get the Best Rate and Coverage

- Shop with Local Independent Agents: They understand Arkansas’s specific weather risks and can access multiple companies, including regional favorites like Farm Bureau.

- Bundle Policies: Combining renters and auto insurance with the same company typically yields a significant discount (15-25%).

- Ask About Weather Mitigation Discounts: Storm shutters, hail-resistant roofing on the building, or a safe room may qualify.

- Maintain Good Credit: Arkansas allows insurers to use credit-based insurance scores. Good credit can lead to lower premiums.

- Choose a Higher Deductible: Opting for a higher deductible (e.g., $1,000) lowers your premium, but ensure you can afford the out-of-pocket cost after a storm.

For authoritative information on disaster preparedness, consult the Ready.gov Arkansas page and the Arkansas Insurance Department.

Steps to Take Before and After a Severe Weather Event

Preparation is key in a tornado-prone state. Knowing the claims process ensures a smoother recovery after a disaster.

Before a Storm: Arkansas-Specific Preparation

- Create a Digital Home Inventory: Use your phone to video each room. Store the file in the cloud.

- Know Your Policy & Deductible: Understand what your policy covers and your financial responsibility.

- Prepare a Severe Weather Kit: Include insurance documents, inventory list, medications, and essentials. Know your safe place.

- Secure Important Documents: Have digital copies of your policy, ID, and inventory.

After a Loss: Filing a Claim in Arkansas

If disaster strikes:

- Ensure Safety & Mitigate Damage: Take reasonable steps to prevent further loss (e.g., tarp a damaged roof, board up windows). Keep receipts for materials.

- Document Everything: Take extensive photos/video of all damage before cleaning up.

- Contact Your Insurer Immediately: Start the claims process. Use their app if available for faster service.

- Separate Claims if Needed: If you have both wind and flood damage, you will file separate claims with your renters insurer and your flood insurer.

- Keep Detailed Records: Log all communications with adjusters, contractors, and your landlord. Save all receipts for ALE expenses.

After widespread storms, be patient as adjusters handle high volumes of claims.

Conclusion

Renters insurance in Arkansas is an indispensable, affordable, and often required layer of protection against the state’s formidable weather risks. It provides the financial means to recover personal property from tornadoes, hail, and thunderstorms while shielding you from significant liability exposures. The crucial lesson for Arkansas renters is to recognize the exclusion for flood damage and secure a separate NFIP policy if you live in a flood-prone area. By securing adequate liability limits, opting for Replacement Cost coverage, and considering key endorsements like water backup, you can craft a policy that offers true resilience. Whether you’re in an apartment in Little Rock, a rental home in Fayetteville, or a duplex in Jonesboro, a well-structured renters insurance policy is your best defense for enjoying life in the Natural State with confidence and peace of mind.

Frequently Asked Questions (FAQ)

Is renters insurance required by law in Arkansas?

No, Arkansas state law does not require tenants to carry renters insurance. However, it is a standard and nearly universal requirement imposed by landlords through the lease agreement. You are contractually obligated to comply if it’s in your lease.

Does renters insurance cover tornado damage in Arkansas?

Yes, absolutely. Tornado damage is covered under the standard “windstorm” peril in a renters insurance policy. This includes damage to your personal belongings from tornado winds, hail, and falling debris. The structure itself is the landlord’s responsibility, but your possessions inside are protected.

Do I need flood insurance in Arkansas?

It depends on your location. If you rent near a river, creek, or in a low-lying area prone to flash flooding, you likely need separate flood insurance. Standard policies exclude flood damage. Check FEMA’s flood maps for your address. Many areas of Arkansas, especially along major rivers, are at risk.

Are hail and lightning covered?

Yes. Hail damage to your personal property is covered. Lightning strikes are also a covered peril, which includes damage from fire or power surges caused by the strike. Surge protectors are still recommended for valuable electronics.

I’m a student at the University of Arkansas, UA Little Rock, or A-State. Do I need a policy?

If you live off-campus in a house or apartment, yes, you absolutely need your own renters insurance, and your lease will require it. If you live in a university dormitory, your parents’ homeowners policy may offer limited coverage, but a separate, affordable student policy is highly recommended for full protection of your electronics, textbooks, and liability.

Can my insurance be cancelled because of too many weather claims?

An insurer cannot cancel your policy mid-term for filing weather-related claims. However, at renewal time, they may choose not to renew your policy based on your claims history and overall risk assessment. Maintaining a claims-free history when possible is beneficial.

How do I prove I have insurance to my landlord?

Your insurance company will provide a “declarations page” or “certificate of insurance.” You will provide a copy of this document to your landlord or property manager, usually via email or a tenant portal. They will also require being listed as an “additional interest” on the policy.