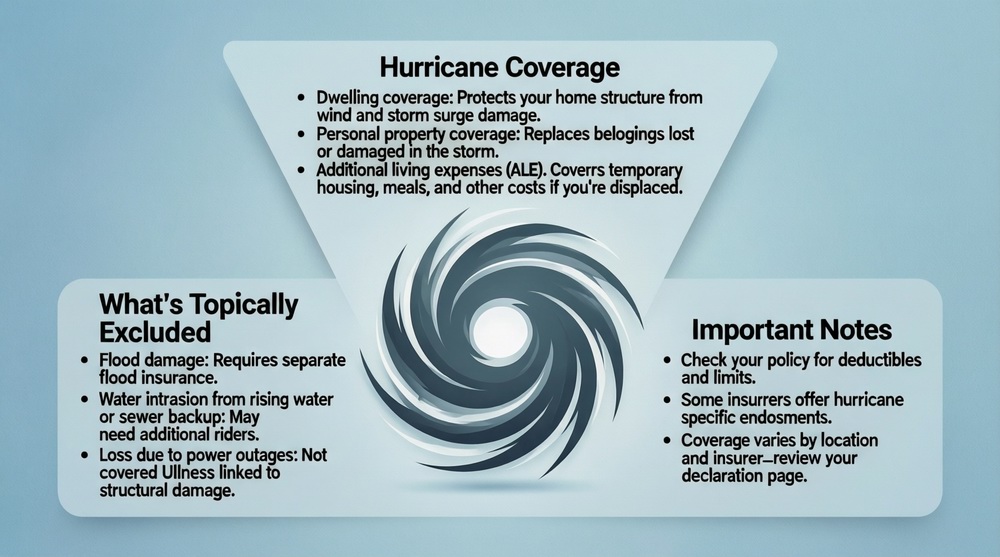

Renters insurance does cover hurricane damage, but only for certain perils associated with the storm. It typically covers damage to your personal property caused by wind, wind-driven rain, and hail. It also provides Additional Living Expenses (ALE) if you’re forced to evacuate or your home is uninhabitable. However, standard renters insurance does NOT cover flood damage, including storm surge and flooding from torrential rain. Flood insurance is a separate policy through the NFIP or private insurers. Furthermore, policies in high-risk coastal areas may have a separate hurricane or windstorm deductible, which is a percentage of your coverage limit, not a flat fee. For foundational knowledge, start with our guide on what renters insurance is.

How Renters Insurance Covers Hurricane Perils

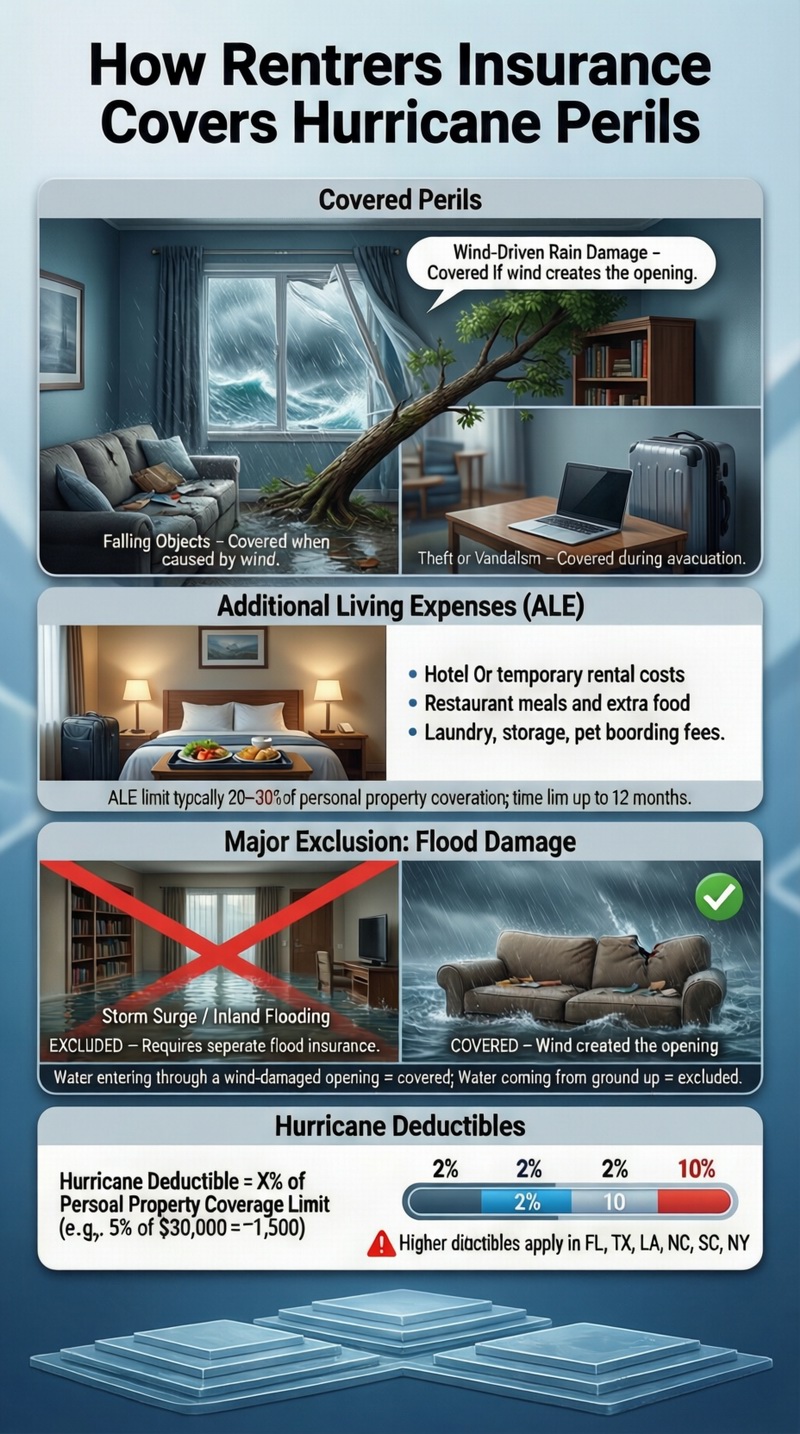

A hurricane is a complex event made up of multiple perils. When asking “does renters insurance cover hurricanes?”, you must break it down by cause of damage. Standard renters insurance (HO-4) is a “named perils” policy, and fortunately, several key hurricane-related perils are named.

Covered Hurricane Damage to Your Belongings

Your personal property coverage (Coverage C) typically protects your belongings from:

– Wind Damage: If hurricane-force winds rip off the roof or break windows, and your belongings are damaged by the wind or subsequent rain entering, that damage is covered.

– Hail Damage: Hail breaking windows or damaging property inside is covered.

– Water Damage from Wind-Driven Rain: This is crucial. If wind first creates an opening (breaks a window, damages the roof) allowing rain to enter, the resulting water damage to your belongings is covered. The sequence matters.

– Falling Objects: Trees or debris propelled by wind that crash into your rental and damage your items.

– Theft or Vandalism: If you evacuate and your home is looted, theft is a covered peril.

This coverage is part of your standard renters insurance coverage.

The Lifesaver: Additional Living Expenses (ALE)

If a hurricane forces a mandatory evacuation or renders your rental unit uninhabitable (no power, water, or structural damage), your policy’s ALE coverage (Coverage D) pays for:

– Hotel or temporary rental costs.

– Restaurant meals and extra food costs.

– Laundry, storage, and pet boarding fees.

ALE is subject to a limit (often 20-30% of your personal property coverage) and a time limit (e.g., up to 12 months). In a major hurricane, this coverage is invaluable.

The Major Exclusion: Flood and Storm Surge Damage

This is the most important exclusion. Standard renters insurance explicitly excludes flood damage. For insurance purposes, “flood” is defined as an overflow of a body of water, unusual and rapid accumulation of surface water, or mudflow. This includes:

– Storm Surge: The rising sea water pushed ashore by a hurricane’s winds.

– Inland Flooding: Torrential rainfall that overwhelms drains and causes rivers, lakes, or streets to overflow into homes.

If water comes from the ground up, it’s a flood. If it comes from the sky through a wind-created opening, it’s likely covered wind-driven rain. This distinction is critical for claims.

| Hurricane Damage Scenario | Typically Covered by Renters Insurance? | Key Details & Required Coverage |

|---|---|---|

| Wind smashes a window, rain ruins your sofa. | YES (Wind-Driven Rain) | Covered because wind (a covered peril) created the opening for rain. |

| Storm surge inundates your first-floor apartment. | NO | Excluded as flood. Requires separate flood insurance. |

| A tree falls on the roof, damaging your belongings. | YES | Falling object due to wind is a covered peril. |

| Power outage causes food spoilage. | MAYBE (Check policy) | Some policies have a small limit (e.g., $500) for food spoilage due to off-premises power failure. Not all do. |

| Mandatory evacuation forces hotel stay. | YES (ALE Coverage) | Covered if due to a covered peril (like wind damage) or often if a civil authority orders evacuation for imminent danger. |

| Floodwater enters after wind damage. | NO for flood portion | Very complex. An adjuster will separate damage from wind-driven rain (covered) from damage from rising floodwater (not covered). |

Understanding Hurricane Deductibles

In hurricane-prone states (like FL, TX, LA, NC, SC, NY), your renters insurance policy may have a hurricane or windstorm deductible. This is not a flat dollar amount like your standard deductible (e.g., $500). Instead, it’s a percentage of your personal property coverage limit (e.g., 2%, 5%, or 10%). If you have $30,000 in personal property coverage and a 5% hurricane deductible, you would pay the first $1,500 of a hurricane-related claim out of pocket. This can be a significant amount. Know what your policy says.

How to Be Fully Protected: Creating a Hurricane Insurance Plan

Relying solely on a standard renters policy in hurricane country is risky. Build a layered defense:

1. Maximize Your Renters Insurance:

– Ensure you have adequate personal property limits (conduct a home inventory).

– Opt for Replacement Cost Value (RCV) coverage, not Actual Cash Value.

– Understand your hurricane deductible and ALE limits.

2. Purchase Separate Flood Insurance:

– Flood insurance is available from the National Flood Insurance Program (NFIP) and private insurers.

– There is a 30-day waiting period before NFIP coverage takes effect, so don’t wait until a storm is forecast.

– Consider it even if you’re not in a “high-risk” zone; over 20% of flood claims are outside these areas.

3. Document Everything Before and After:

– Pre-Storm: Photograph and video all rooms and valuables for your inventory. Store this digitally (in the cloud).

– Post-Storm: Document all damage extensively before cleaning up. Take photos of water lines, damaged items, and the source of damage if possible.

The Claims Process After a Hurricane

1. Ensure Safety First. Return only when authorities say it’s safe.

2. Mitigate Further Damage. Take reasonable steps to prevent more loss (e.g., cover broken windows with tarps). Keep receipts for materials, as these may be reimbursable.

3. Contact Your Insurer. File your claim as soon as possible. Be prepared for high call volume.

4. Separate Damage Types. Be ready to help the adjuster distinguish between wind/rain damage (covered) and flood damage (not covered unless you have flood insurance).

5. File with Multiple Insurers if Needed. If you have flood insurance, you will file a separate claim with that insurer for flood damage.

Special Considerations for High-Risk Areas

In some coastal regions, obtaining standard renters insurance can be more difficult or expensive. You may be placed in a state-run insurance pool (like Florida’s “Citizens”) or see significantly higher premiums. Despite the cost, coverage is non-negotiable. Also, review your lease; landlords in hurricane zones often have specific requirements for tenant insurance and may require proof of flood insurance. For help evaluating renters insurance cost in high-risk areas, see our guide, and explore all renters insurance options.

Conclusion: Dual Policies for Complete Protection

So, does renters insurance cover hurricanes? Partially—it’s a critical piece of the puzzle, covering wind, hail, and the evacuation costs that often accompany a storm. But it’s only half the solution. The destructive power of water, in the form of storm surge and flooding, requires a separate flood insurance policy. The combination of a robust renters policy (with high limits, RCV, and an understanding of your deductible) and a flood insurance policy is the only way to achieve comprehensive financial protection against a hurricane. Don’t gamble with one of nature’s most powerful forces; insure against all its facets.

Frequently Asked Questions (FAQ)

If I’m inland, do I still need to worry about hurricane coverage?

Absolutely. Inland areas face major hurricane risks from high winds, tornadoes spawned by the storm, and especially inland flooding from torrential rainfall, which can travel hundreds of miles from the coast. Your renters insurance covers the wind damage, but you may still need flood insurance if you’re in a flood-prone area, even far from the coast.

Does renters insurance cover a hotel if I evacuate voluntarily?

It depends. ALE coverage typically requires that your home be uninhabitable due to a covered loss or that a civil authority prohibits access due to direct damage to the area. If you voluntarily evacuate before a mandatory order is issued and your home suffers no damage, ALE may not apply. Check your policy wording.

What is the difference between “flood” and “water backup” coverage?

Flood is water from outside (rivers, oceans, ground) flowing into your home. Water backup is when sewage or water backs up through drains from inside the municipal sewer system. Both are excluded from standard renters policies. You need a flood policy for the first and a “water backup endorsement” for the second. A hurricane can cause both.

Can my renters insurance be canceled because I live in a hurricane zone?

Insurers cannot cancel a mid-term policy due to hurricane risk. However, they may choose not to renew your policy after it expires, especially if they are reducing their exposure in a high-risk area. This is why state-run insurance pools exist—to provide coverage of last resort.

How do I prove wind caused an opening for rain damage?

Documentation is key. Take photos that show the wind damage (e.g., broken window frame, missing shingles) and the resulting water damage inside. If possible, take photos before any temporary repairs. Your adjuster will investigate, but clear evidence helps support your claim that it was wind-driven rain, not floodwater.

Are hurricane deductibles legal and common?

Yes, they are legal and standard practice in many coastal states. They are explicitly outlined in the policy you purchase. It’s essential to read your declarations page to see if you have a flat deductible or a percentage-based hurricane deductible and what triggers it (e.g., when the National Weather Service issues a hurricane warning).

Where can I get official information on flood risk and insurance?

The primary source for flood insurance and mapping is the FEMA National Flood Insurance Program (NFIP) website. You can enter your address to see flood maps, understand your risk, and find agents who sell policies. This is an essential step for anyone in a hurricane-prone region.