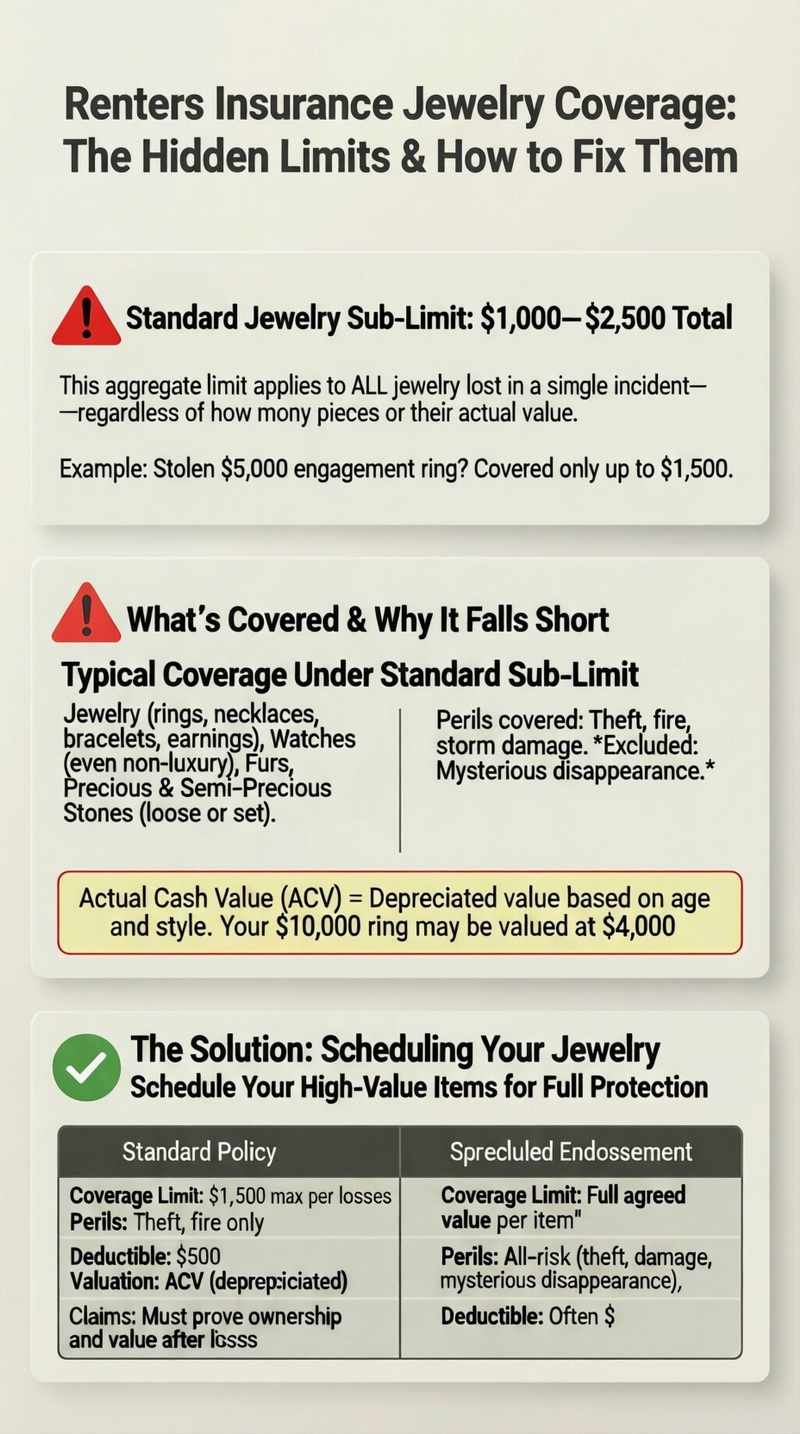

Standard renters insurance jewelry coverage is extremely limited. Most policies have a low sub-limit for theft of jewelry, watches, and furs—typically $1,000 to $2,500 total, regardless of how many pieces you own or their actual value. This means a stolen $5,000 engagement ring might only be covered for $1,500. To get full protection, you must “schedule” your high-value jewelry. This involves getting a professional appraisal and adding a scheduled personal property endorsement (rider) to your policy for each item or collection. This provides agreed-value coverage, often with no deductible, and protects against more perils, including mysterious disappearance. Start with the basics in our guide on what renters insurance is.

The Problem: Standard Renters Insurance Jewelry Limits

When reviewing your renters insurance jewelry coverage, the first thing to find is the “Special Limits of Liability” section in your policy (HO-4 form). This is where insurers cap their payout for high-risk, portable items like jewelry. The limit is an aggregate limit per loss, not per item. For example, if your policy has a $1,500 jewelry theft limit and thieves steal a $4,000 ring and a $1,000 necklace, the maximum you could recover for both items combined is $1,500, minus your deductible. This sub-limit applies primarily to theft; coverage for other perils like fire may fall under your general personal property limit, but the valuation method (ACV vs. RCV) still applies. This is a critical detail in your overall renters insurance coverage.

What’s Typically Covered Under the Standard Sub-Limit?

The sub-limit usually applies to:

– Jewelry: Rings, necklaces, bracelets, earrings, precious gems.

– Watches: Even non-luxury watches are often included in this category.

– Furs: Fur coats and garments.

– Precious and Semi-Precious Stones: Loose or set.

The limit is for the total of all items in this category lost in a single incident (e.g., one theft or one fire).

Actual Cash Value: A Double Whammy

Even if your loss is within the sub-limit, a standard policy with Actual Cash Value (ACV) will pay only the depreciated value of your jewelry. Jewelry doesn’t depreciate like electronics; sentimental and market value may even appreciate. However, insurers often apply depreciation based on age and style, which can result in a shockingly low payout. Replacement Cost Value (RCV) coverage is better but still bound by the theft sub-limit.

The Solution: Scheduling Your Jewelry (A Valuable Items Rider)

Scheduling is the process of listing specific high-value items on your policy with a description and an agreed-upon value. This endorsement overrides the standard sub-limits and provides superior coverage.

| Coverage Aspect | Standard Policy (with sub-limit) | Scheduled Jewelry Endorsement |

|---|---|---|

| Coverage Limit | Low aggregate limit ($1k-$2.5k) for all jewelry. | Covered for the full agreed value listed on the schedule for each item. |

| Perils Covered | Only named perils (theft, fire, etc.). “Mysterious disappearance” is excluded. | All-risk coverage. Includes loss, theft, damage, and mysterious disappearance (e.g., losing a ring). |

| Deductible | Your standard policy deductible applies (e.g., $500). | Often $0 deductible applies to scheduled items. |

| Valuation Method | Actual Cash Value (depreciated) or Replacement Cost. | Agreed Value. You and the insurer agree on the value upfront (via appraisal). |

| Claims Process | Must prove ownership and value after a loss. | Simpler. The item is pre-documented and valued, leading to faster settlement. |

How to Schedule Your Jewelry: A Step-by-Step Guide

1. Identify Items to Schedule: Any single piece or collection whose value exceeds your policy’s jewelry sub-limit should be scheduled. Even items below the limit but with high sentimental value may be worth scheduling for the broader “all-risk” coverage.

2. Get a Professional Appraisal: For items over a certain value (often $5,000+), insurers require a recent appraisal from a certified gemologist or reputable jeweler. The appraisal should include a detailed description, photographs, carat weight, cut, clarity, color, and the current retail replacement value.

3. Contact Your Insurance Company: Provide the appraisal or receipt to your agent. They will add a scheduled personal property endorsement to your policy.

4. Pay the Additional Premium: The cost is typically 1-2% of the item’s appraised value per year. For a $10,000 ring, that’s $100-$200 annually. This is a small price for full peace of mind.

5. Update Appraisals Periodically: Update appraisals every 3-5 years to account for inflation and changes in market value, ensuring your scheduled amount remains accurate.

What About Costume or Fashion Jewelry?

Lower-value fashion jewelry is usually adequately covered under the standard personal property limit, as its total value likely doesn’t exceed the theft sub-limit. However, if you have a collection of vintage costume jewelry with significant value, it’s wise to get it appraised and consider scheduling.

What to Do If Your Jewelry is Lost, Stolen, or Damaged

Even with the best coverage, a loss is stressful. Here’s the claims process:

For Standard (Non-Scheduled) Jewelry:

1. File a Police Report: Mandatory for theft.

2. Contact Your Insurer: Start the claim.

3. Provide Proof: You’ll need to provide proof of ownership (photos, receipts, appraisals) and prove the value. This is very difficult without prior documentation.

4. Receive Payment: Payout will be limited to the sub-limit and subject to your deductible and ACV depreciation.

For Scheduled Jewelry:

1. Report the Loss: Notify insurer and police (if theft).

2. Reference the Schedule: Provide the item’s schedule number from your policy.

3. Simplified Settlement: The insurer will typically issue payment for the agreed value listed on the schedule, often with no deductible, and with less hassle.

The Importance of a Home Inventory and Documentation

For all jewelry, maintain a “jewelry inventory file” with:

– Photographs and videos of each piece, worn and by itself.

– Copies of all appraisals, receipts, and gemological certificates (e.g., GIA reports for diamonds).

– A detailed description, including any inscriptions or unique features.

Store this digitally (in the cloud) and in a safe place separate from the jewelry itself. This is your single most important tool for proving ownership and value.

Cost of Jewelry Coverage and Maximizing Value

Adding scheduled jewelry coverage will increase your premium, but it’s cost-effective. The alternative—being underinsured—is far more expensive. To manage renters insurance cost while protecting valuables:

– Bundle: If you also have auto insurance with the same company, you likely get a multi-policy discount that can offset some of the jewelry rider cost.

– Ask About Discounts: Some insurers offer discounts for having a home security system or a safe, which reduces theft risk.

– Review Limits Annually: As you acquire new pieces or the value of existing ones changes, update your schedule to avoid being underinsured.

Secure Storage: A Requirement and a Discount

Many insurers require scheduled jewelry to be stored in a locked safe when not in use, especially for very high-value items. Using a home safe bolted to the structure can also make you eligible for a general security discount on your overall policy. It’s a wise practice regardless.

Conclusion: Don’t Leave Your Valuables Exposed

Standard renters insurance jewelry coverage is a trap for the unwary. Its low sub-limits and restrictions leave most valuable pieces dangerously underinsured. The solution is simple and affordable: schedule your high-value jewelry. The modest additional premium buys you full, agreed-value coverage, protection against a wider range of losses (including mysterious disappearance), and a hassle-free claims process. Take an afternoon to inventory your jewelry, get key pieces appraised, and contact your insurer to schedule them. It’s the only way to ensure your precious items are truly protected. For a complete review of your protection, explore all renters insurance options with your agent.

Frequently Asked Questions (FAQ)

Does renters insurance cover a lost engagement ring?

Not under a standard policy. “Mysterious disappearance” (losing an item) is excluded. However, if you schedule the ring, the endorsement typically includes coverage for loss. This is a primary reason to schedule engagement and wedding rings.

Do I need an appraisal for every piece of jewelry?

For scheduling, insurers usually require a professional appraisal for items above a certain value threshold (often $1,000-$5,000). For items below that, a detailed receipt from a reputable jeweler may suffice. Always check with your specific insurer.

Are smartwatches like an Apple Watch covered as jewelry?

This is a gray area. An Apple Watch is primarily an electronic device and might be covered under the general personal property limit or an electronics sub-limit. However, a gold Apple Watch Edition might be considered jewelry. Clarify with your insurer and consider scheduling high-end smartwatches if their value exceeds standard limits.

What happens if the market value of my jewelry increases after I schedule it?

You are responsible for updating the scheduled value. If your jewelry appreciates and you have a total loss, you will only receive the amount for which it was scheduled. This is why updating appraisals every 3-5 years is crucial.

Does scheduling cover jewelry while I’m traveling?

Yes. Scheduled jewelry typically has worldwide coverage. Your ring is covered if it’s stolen from your hotel room or lost while you’re on vacation. This is a significant advantage over the standard policy.

Can I schedule inherited jewelry without a receipt?

Yes, but you will need a current appraisal from a certified gemologist to establish its value for insurance purposes. The appraisal serves as the proof of value needed to create the schedule.

Where can I find a reputable appraiser?

Look for an appraiser with credentials from recognized organizations like the American Gem Society (AGS), the Gemological Institute of America (GIA), or the International Society of Appraisers (ISA). Your insurer may also have a list of preferred providers. For general guidance on protecting valuables, the Insurance Information Institute’s jewelry insurance article offers excellent advice.