Choosing the correct renters insurance liability coverage amount is one of the most important financial decisions you can make as a tenant. While many policies default to $100,000, this is often dangerously inadequate. We recommend a minimum of $300,000 to $500,000 in liability coverage. If you have significant assets, a higher net worth, or increased risk (e.g., a dog, a swimming pool, frequent guests), you should strongly consider a personal umbrella policy providing an additional $1 million or more in coverage. The incremental cost to increase your liability limit is very small, but the financial protection it provides is immense. For context, start with our guide on what renters insurance is.

Why Your Liability Coverage Amount Matters

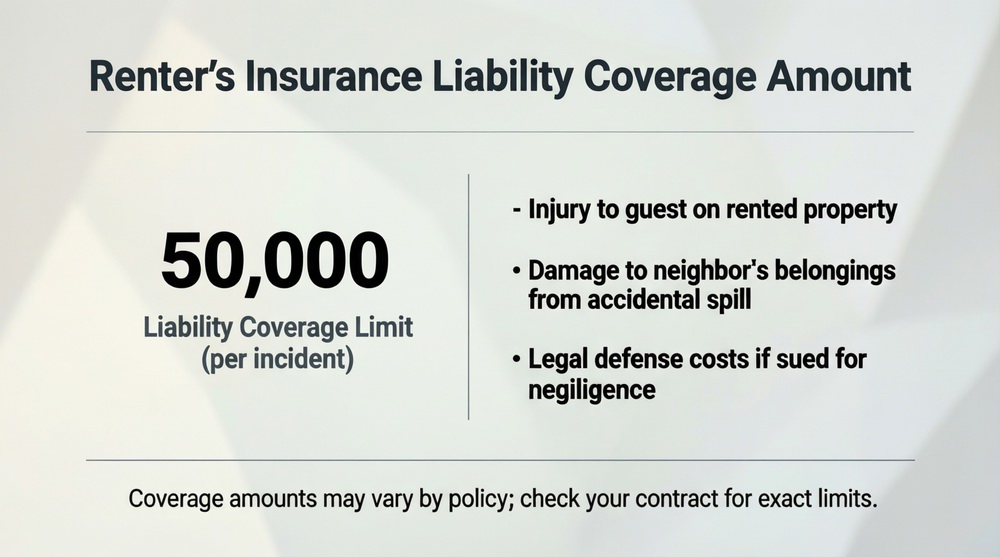

Personal liability coverage (Coverage E) protects you if you are found legally responsible for bodily injury or property damage to others. It pays for the injured party’s medical bills, lost wages, pain and suffering, and your legal defense costs. In our litigious society, a single accident—a guest’s slip and fall, a dog bite, a kitchen fire that spreads—can result in a lawsuit seeking hundreds of thousands of dollars. If a judgment exceeds your renters insurance liability coverage amount, your personal assets (savings, investments, even future wages) can be seized to satisfy the debt. This coverage is the cornerstone of your renters insurance coverage.

Real-World Cost Examples of Liability Claims

– Dog Bite: The average cost per claim nationally exceeds $64,000. Severe injuries requiring surgery and resulting in scarring can easily exceed $250,000.

– Slip and Fall: A guest breaks a hip, requiring surgery and rehab. Medical bills + lost wages + pain and suffering can reach $300,000+.

– Property Damage: You accidentally start a kitchen fire that damages multiple units in your apartment building. Repair costs and loss of use for neighbors could total $500,000 or more.

These figures demonstrate why a $100,000 limit is a starting point, not a safe harbor.

How to Determine Your Optimal Liability Coverage Amount

Your ideal renters insurance liability coverage amount is not one-size-fits-all. It should be based on a calculated assessment of your assets and your risk exposure.

| Factor to Consider | Recommended Liability Coverage Amount | Rationale |

|---|---|---|

| Minimal Assets, Low Risk (Student, first apartment) | $100,000 – $300,000 | Meets basic lease requirements and provides fundamental protection. Still, $300K is a safer minimum. |

| Moderate Assets (Savings, investments, car equity) | $300,000 – $500,000 | Protects your accumulated net worth from a single lawsuit. The most common recommendation for the average professional renter. |

| High Net Worth / High Risk (Substantial savings, dog of a restricted breed, host frequent gatherings, have a home business) | $500,000 + UMBRELLA POLICY | Your assets are a target in a lawsuit. An umbrella policy provides excess liability coverage ($1M-$5M) at a low cost, protecting everything you’ve built. |

| Landlord Lease Requirement | At least the lease minimum (Often $100K) | You must meet this to comply with your lease, but you can and should purchase more than the required minimum for your own protection. |

The Asset Calculation Method

Add up the value of all assets you need to protect:

– Cash in checking/savings accounts

– Investment portfolios (stocks, bonds, mutual funds)

– Retirement accounts (Though often protected, it’s best not to risk it)

– Equity in vehicles or other property

– Value of valuable personal property (jewelry, art, collectibles)

– Future Income: A court can garnish your wages. Your earning potential is a major asset.

Your liability coverage limit should at least equal your total protectable net worth. Many advisors recommend carrying enough to cover twice your net worth.

Assessing Your Personal Risk Factors

Your lifestyle increases your needed renters insurance liability coverage amount.

– Pets: Dog ownership, especially of breeds insurers consider high-risk, significantly increases liability exposure.

– Social Hosting: Frequent parties increase the chance of an accident or alcohol-related incident.

– High-Value Possessions: Owning items that could cause severe injury if misused (e.g., certain sports equipment).

– Youthful Household Members: Children or young adults whose activities could lead to an incident.

– Home Business Activity: Even minor business activity can void standard liability coverage; you need a separate policy or endorsement.

The Power of a Personal Umbrella Policy

When your needed protection exceeds standard renters policy limits (often capped at $500,000), a personal umbrella policy is the most cost-effective solution. It’s a separate policy that provides excess liability coverage on top of your underlying renters (and auto) insurance.

How it works: If you have a $300,000 renters liability limit and a $1 million umbrella, you have $1.3 million in total protection. If a $1 million lawsuit settles, your renters insurance pays the first $300,000, and your umbrella policy pays the next $700,000.

Cost: Typically $150-$300 per year for the first $1 million in coverage—a small price for massive peace of mind.

Requirement: Umbrella insurers usually require you to have high underlying limits (e.g., $300K or $500K) on your renters and auto policies first.

How Much Does Increasing Your Liability Limit Cost?

One of the best features of liability insurance is that increasing your limit is very inexpensive. The premium difference between $100,000 and $300,000 in liability coverage is often only $20 to $40 per year. Jumping from $100,000 to $500,000 might cost an extra $50 annually. This is because the vast majority of claims fall below $100,000, so insurers price higher limits very competitively. This small investment is a critical part of managing your overall renters insurance cost effectively. For the right policy, explore all renters insurance options.

Sample Premium Impact

Based on industry averages:

– Renters Policy with $100,000 Liability: $180/year

– Same Policy with $300,000 Liability: $200/year (+$20)

– Same Policy with $500,000 Liability: $210/year (+$30)

For pennies a day, you can triple or quintuple your protection.

Steps to Review and Adjust Your Liability Coverage

1. Review Your Current Policy Declarations Page. Find the listed liability limit.

2. Calculate Your Total Assets and Net Worth.

3. Evaluate Your Risk Factors. Be honest about pets, social habits, etc.

4. Call Your Insurance Agent or Company. Ask for quotes to increase your liability limit to $300,000 and $500,000.

5. Ask About an Umbrella Policy Quote. Inquire about the cost and underlying requirements.

6. Make the Change. Increase your limit immediately. The increased premium is pro-rated.

7. Re-evaluate Annually. As your assets and life change, so should your liability coverage.

Conclusion: Don’t Underestimate Your Exposure

Selecting an adequate renters insurance liability coverage amount is not about fear; it’s about prudent financial planning. In a world where medical bills are astronomical and lawsuits are common, carrying only the minimum is a gamble with your financial future. For a few extra dollars per month, you can secure a robust liability shield of $300,000 or $500,000 and sleep soundly knowing that a single accident won’t wipe out your savings or jeopardize your future earnings. If your assets warrant it, layer on an umbrella policy for complete, high-limit protection. Don’t wait for an incident to discover you’re underinsured—increase your limits today.

Frequently Asked Questions (FAQ)

Can my landlord require a specific liability coverage amount?

Yes, and they often do. It is standard practice for lease agreements to require tenants to carry a minimum amount of liability insurance, commonly $100,000. You must provide a certificate of insurance proving you meet this requirement. However, you are free to purchase a higher limit for your own protection.

Does liability coverage protect me if I’m sued for libel or slander?

No, not under standard liability coverage. Standard Coverage E is for bodily injury and property damage liability. Lawsuits for personal injury (libel, slander, defamation, false arrest) typically require a separate “Personal Injury” endorsement to your renters policy. Ask your agent about this addition.

What happens if a claim exceeds my liability limit?

You are personally responsible for the amount that exceeds your policy limit. The injured party can pursue your personal assets through legal means, including garnishing your wages or placing liens on your property. This is called “excess liability” and is precisely what higher limits and umbrella policies are designed to prevent.

Is there a maximum liability limit I can get on a renters policy?

Most standard renters insurance policies max out at $500,000 in personal liability coverage. If you need more, you must purchase a personal umbrella policy, which provides coverage in increments of $1 million and sits on top of your underlying renters and auto liability limits.

Does my liability coverage follow me when I travel?

Yes, generally. Your renters liability coverage is typically worldwide. If you accidentally injure someone or damage property while on vacation, your policy may provide coverage. There are exceptions for certain activities (like owning foreign property), so check your policy wording.

How does Medical Payments to Others differ from liability coverage?

Medical Payments (MedPay) is a no-fault coverage that pays small medical bills (e.g., $1,000-$5,000) for guests injured in your home, regardless of who is at fault. It’s designed to prevent minor incidents from becoming lawsuits. Liability coverage is for when you are legally at fault for larger injuries or damages and includes legal defense.

Where can I find more information on personal liability risks?

The Insurance Information Institute’s guide to umbrella liability policies provides excellent context on why high liability limits are important and how umbrella policies work, which directly informs decisions about your renters liability coverage amount.