The answer to “does renters insurance cover power outage” is nuanced: it depends on the *cause* of the outage and the *type of damage* that results. Standard renters insurance does not cover the power outage itself or direct losses from the lack of electricity. However, if the outage is caused by a *covered peril* listed in your policy—such as a lightning strike, windstorm, hail, or a vehicle damaging a utility pole—then any resulting damage to your personal property *may* be covered. This typically includes food spoilage in a refrigerator or freezer and damage to electronics from a power surge that occurs when power is restored. Furthermore, if the outage makes your rental unit uninhabitable (e.g., no heat in winter), your policy’s loss of use coverage can pay for temporary housing and meals. This guide will clarify the specific scenarios where coverage applies, what documentation you need, and the critical exclusions every renter must understand.

Understanding the Core Principle: Covered Perils

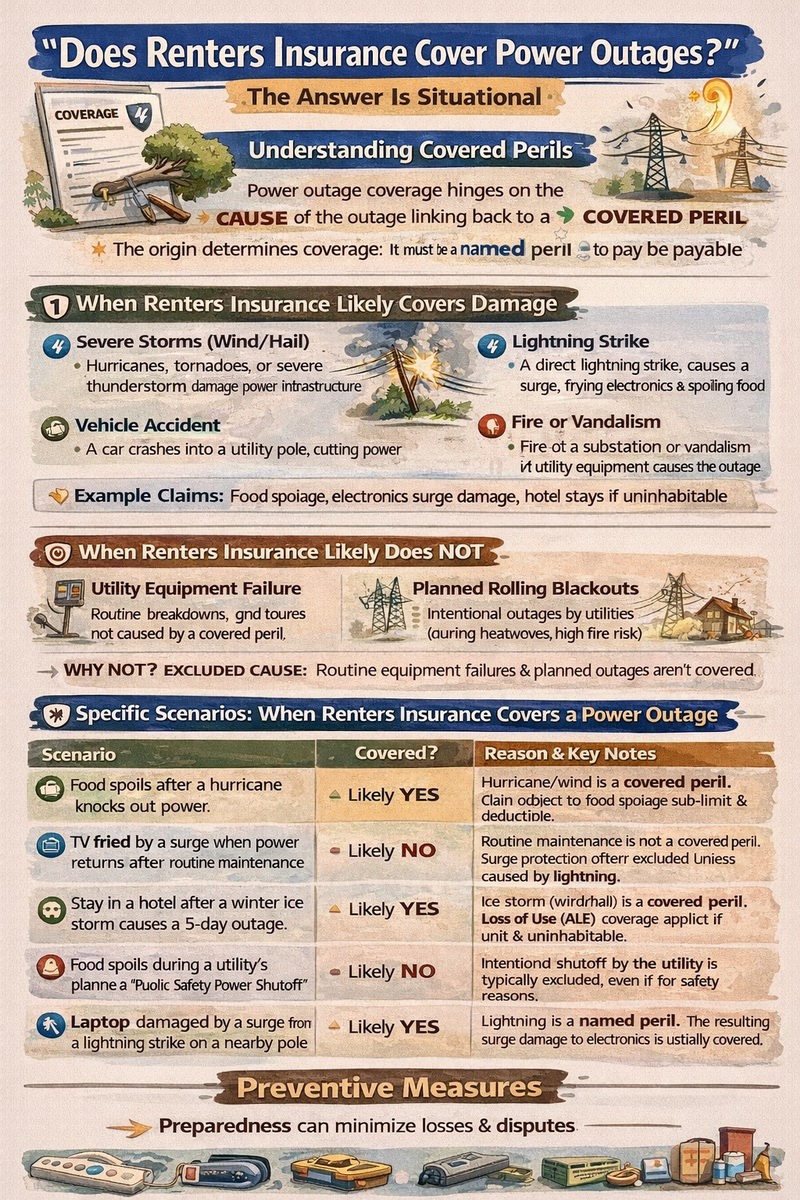

To answer “does renters insurance cover power outage,” you must first understand the “covered perils” model. A standard renters insurance policy (an HO-4 form) is not an “all-risk” policy for your belongings. Instead, it only covers losses caused by specific perils named in the policy. Common named perils include fire, lightning, windstorm, hail, theft, vandalism, and damage from vehicles or aircraft. The power outage is not a peril itself; it is an *event*. Coverage hinges on whether a *covered peril* caused the outage, and then whether that outage led to direct damage to your insured personal property.

The “Named Peril” Trigger for Coverage

If a tree limb knocked down by a windstorm (a covered peril) falls on a power line and causes an outage that lasts for days, the root cause is the windstorm. Therefore, any resulting covered damage, like spoiled food, could be claimed. Conversely, if the outage is due to routine grid maintenance, a rolling blackout due to high demand, or general equipment failure by the utility company (none of which are named perils), then any resulting loss is almost certainly not covered. The distinction is always in the originating cause listed in your policy documents.

Food Spoilage: The Most Common Claim Scenario

One of the most frequent claims related to power outages is for spoiled food. Many renters insurance policies include a specific sub-limit for food spoilage, typically ranging from $500 to $1,000, but *only if the spoilage results from a covered peril*. For example, if lightning strikes a transformer and causes an outage that spoils your refrigerator’s contents, you could file a claim up to that sub-limit, minus your deductible. It’s crucial to check your policy for this specific provision and its limit, as it’s not always automatically included or may have a very low limit.

Specific Scenarios: When You Are (and Aren’t) Covered

Let’s apply the “covered peril” principle to real-world situations to clearly see when the answer to “does renters insurance cover power outage” is yes or no. This breakdown will help you quickly assess potential coverage.

When Renters Insurance LIKELY Provides Coverage

- Outage from a Severe Storm (Wind/Hail): A hurricane, tornado, or severe thunderstorm damages power infrastructure. Resulting food spoilage or surge damage when power returns may be covered.

- Lightning Strike: A direct lightning strike to a power line or transformer causes a surge and outage, frying your electronics and spoiling food. Both the surge damage and spoilage are typically covered.

- Vehicle Accident: A car crashes into a utility pole, cutting power. Damage from the resulting outage may be covered.

- Fire or Vandalism: If a fire (a covered peril) at a substation or vandalism to utility equipment causes the outage, related losses could be covered.

- Inhabitability Triggers Loss of Use: If a winter storm causes a days-long outage, rendering your apartment uninhabitable due to no heat, your loss of use coverage can pay for a hotel and restaurant meals.

When Renters Insurance Likely Does NOT Provide Coverage

- Utility Company Equipment Failure: General wear and tear, overload, or non-covered failure of utility equipment.

- Planned Rolling Blackouts/Brownouts: Outages implemented by the grid operator to prevent a larger failure.

- Power Surge from Grid Restoration (if not preceded by a covered peril): A surge that happens when the utility turns the power back on after routine work is usually not covered unless a covered peril caused the initial outage.

- Voluntary Power Shutoffs: Some utilities preemptively cut power during high fire-risk conditions (like California’s PSPS events). These are often excluded as they are intentional, utility-controlled acts.

- Damage from Melting Ice/Frozen Pipes: If an outage causes your heat to fail and pipes freeze and burst, the water damage may be covered, but the cost to repair the pipes (the landlord’s responsibility) is not. The spoilage of food due to the lack of refrigeration would be a separate consideration based on the cause of the outage.

| Scenario | Covered? | Reason & Key Notes |

|---|---|---|

| Food spoils after a hurricane knocks out power. | Likely YES | Hurricane/wind is a covered peril. Claim subject to food spoilage sub-limit and deductible. |

| TV fried by a surge when power returns after routine maintenance. | Likely NO | Routine maintenance is not a covered peril. Surge protection is often an excluded peril unless caused by lightning. |

| Stay in a hotel after a winter ice storm causes a 5-day outage with no heat. | Likely YES | Ice storm (wind/hail) is a covered peril. Loss of Use (ALE) coverage applies if the unit is uninhabitable. |

| Food spoils during a utility’s planned “Public Safety Power Shutoff.” | Likely NO | Intentional shutoff by the utility is typically excluded, even if for safety reasons. |

| Laptop damaged by a surge from a lightning strike on a nearby pole. | Likely YES | Lightning is a named peril. The resulting surge damage to electronics is usually covered. |

Key Coverages to Review in Your Policy

To accurately determine if your policy answers “does renters insurance cover power outage” in your favor, you need to examine specific sections and endorsements. Knowledge of these details turns speculation into certainty.

Personal Property Coverage and Sub-Limits

Review your policy’s personal property section for:

- Food Spoilage Limit: Often listed as a special sub-limit (e.g., “$500 for loss of perishable food items”). This is the maximum payable for spoiled food, regardless of your main property limit.

- Off-Premises Coverage: If you have food in a standalone freezer in a storage unit or garage, check if it’s covered. Some policies only cover property at your listed residence.

- Perils Listed: Locate the official list of “covered perils” (e.g., “Section I – Perils Insured Against”). This is your definitive guide.

Loss of Use / Additional Living Expenses (ALE)

This is often the most valuable coverage in a prolonged outage. If a *covered peril* causes damage that makes your rental uninhabitable, ALE pays for:

- Hotel or temporary rental costs.

- Restaurant meals (above your normal grocery budget).

- Additional transportation or storage costs.

The key is “uninhabitable.” Loss of power for a few hours is an inconvenience. Loss of power for days in extreme temperatures, leading to no heat, air conditioning, or running water (if on a well pump), likely meets the threshold. You must still pay your rent, but ALE covers the *additional* costs of living elsewhere.

Optional Endorsements: Surge Protection and Refrigerated Property

Some insurers offer endorsements that broaden coverage:

- Electronic Equipment/Surge Protection: While standard policies may cover surges caused by lightning, this endorsement can extend coverage to surges from other causes, including grid restoration. It often has a higher sub-limit for electronics.

- Increased Refrigerated Property Limit: You can sometimes increase the low standard food spoilage limit for an additional premium, which is wise if you have a well-stocked freezer.

Adding these endorsements can provide more comprehensive answers to “does renters insurance cover power outage” by filling common gaps. For insights on how these additions affect your overall renters insurance cost, consult with your agent.

How to File a Claim for Power Outage Damage

If you believe you have a covered loss, following the correct procedure is essential for a smooth claims process. Proper documentation is your strongest asset.

Step 1: Document the Cause and the Damage

As soon as it is safe, begin documenting everything.

- Cause: Take note of official reports. Check your utility company’s outage map or announcements, local news reports citing the cause (e.g., “winds downed lines”), and take photos of any visible damage in your area (like downed trees on lines).

- Damage: Photograph and video all spoiled food before discarding it. List each item with its approximate purchase price and age. For damaged electronics, take clear photos showing the damage and any burn marks. Keep the damaged item if possible, as the adjuster may want to inspect it.

- Expenses: Save all receipts for hotel stays, meals, ice purchased to save food, etc.

Step 2: Contact Your Insurance Company

Report the claim to your insurer promptly. Be prepared to explain:

- The date and time of the outage.

- The believed cause (e.g., “the news reported it was due to the severe thunderstorm that passed through”).

- A general list of damaged property and estimated loss.

The adjuster will determine if the cause is a covered peril under your policy. They may also request a copy of the utility company’s outage report or other proof of cause.

Step 3: Mitigate Further Loss and Work with the Adjuster

You have a “duty to mitigate” loss. This means taking reasonable steps to prevent further damage. For example, if power is restored but your refrigerator is now broken, getting it repaired or replacing spoiled food immediately is expected. Keep receipts for these mitigation expenses. Cooperate fully with the adjuster, providing all requested documentation. Remember, the payout for spoiled food will be subject to your policy’s sub-limit and your deductible.

Preventive Measures and Proactive Planning

While insurance is a reactive safety net, proactive steps can minimize your risk and potential loss from a power outage, making the question “does renters insurance cover power outage” less urgent.

Home Preparedness Strategies

- Use Surge Protectors: Plug expensive electronics into high-quality surge protectors, not just power strips. Consider a whole-home surge protector if you own major appliances.

- Invest in a Generator: For renters, a small, portable, battery-powered generator or power station can keep refrigerators, phones, and small appliances running during short outages.

- Food Management: Keep refrigerator and freezer doors closed during an outage. A full freezer will stay cold longer. Use ice packs and group items together.

- Maintain an Emergency Kit: Include flashlights, batteries, a battery-powered radio, non-perishable food, water, and a first-aid kit.

Understanding Your Utility’s Policies and Resources

Know your rights and your utility’s responsibilities. Some utilities, especially in areas prone to wildfires, have very specific policies about Public Safety Power Shutoffs (PSPS). Understanding these can help you plan. Additionally, in some rare cases, if the outage was due to utility negligence, you may have recourse against them directly, but this is a separate legal matter from an insurance claim and typically difficult to prove. Your renters insurance is a more reliable path for recovery when a covered peril is involved.

Conclusion

So, does renters insurance cover power outage? The definitive answer is: it can, but not for the outage itself. Coverage is activated when a *covered peril* like lightning, wind, or hail causes the outage, which then leads to direct damage like food spoilage, electronics surge damage, or a living situation that becomes uninhabitable. The cornerstone of a successful claim is linking the loss back to a named peril in your policy. Renters must proactively review their policy for specific sub-limits on food spoilage, understand the breadth of their loss of use coverage, and consider adding endorsements for enhanced surge protection. By combining a clear understanding of your renters insurance policy with practical preparedness steps, you can navigate a power outage with confidence, knowing exactly what financial protections you have in place.

Frequently Asked Questions (FAQ)

Does renters insurance cover a hotel if the power goes out?

It might, under specific conditions. If the power outage is caused by a covered peril (like a storm) and your rental unit becomes *uninhabitable* as a result—for example, no heat in freezing temperatures or no air conditioning in extreme heat—then the Loss of Use (ALE) portion of your policy can cover reasonable hotel costs and extra food expenses. A simple outage of a few hours typically does not qualify as making the home uninhabitable.

Will renters insurance replace all the food in my fridge and freezer?

Not necessarily, and not without limits. Most policies have a specific sub-limit for food spoilage, often between $500 and $1,000, and only if the spoilage results from a covered cause. You will also have to pay your deductible. The reimbursement is typically for the actual cash value of the food (what it was worth spoiled, not what you paid). The total payout cannot exceed the sub-limit stated in your policy.

Are power surges covered by renters insurance?

Coverage for power surges is usually limited. Most standard policies explicitly *exclude* damage from power surges *unless* the surge is caused by lightning (a named peril). If a lightning strike causes a surge that fries your TV, it’s likely covered. If a surge occurs when the utility company restores power after routine work, it is likely not covered unless you have purchased a specific “surge protection” or “electronic equipment” endorsement.

What if the power outage causes my pipes to freeze and burst?

This creates a two-part scenario. First, the water damage from the burst pipes to your personal property (soaked furniture, damaged electronics) is typically covered by renters insurance, as water discharge from a plumbing system is often a named peril. However, the cost to repair the actual pipes is the landlord’s responsibility. The initial cause—the power outage—must still be traced to a covered peril (like a winter storm) for the entire chain of events to be covered under your policy.

Does renters insurance cover losses from a rolling blackout?

Almost certainly not. Rolling blackouts or brownouts are intentional, controlled actions by the utility company or grid operator to manage overall system load. Because they are planned and not caused by a sudden, accidental covered peril like a storm or lightning, any resulting food spoilage or inconvenience is not covered by a standard renters insurance policy.

Can I get compensation from the utility company instead?

It is very rare and difficult. Utility companies are generally protected by tariffs and laws that limit their liability for service interruptions, unless you can prove gross negligence. Filing a claim with your own renters insurance (if the cause is covered) is almost always a faster and more reliable path to compensation than suing the utility.

Should I buy a generator, and will it affect my insurance?

A portable generator is an excellent preparedness tool but comes with risks. If you purchase one, ensure you use it safely (outdoors, away from windows, to prevent carbon monoxide poisoning). Owning a generator typically doesn’t affect your insurance premium, but using it improperly and causing a fire (which then damages your property) could lead to a covered claim for the fire damage, provided you weren’t negligent in its operation.