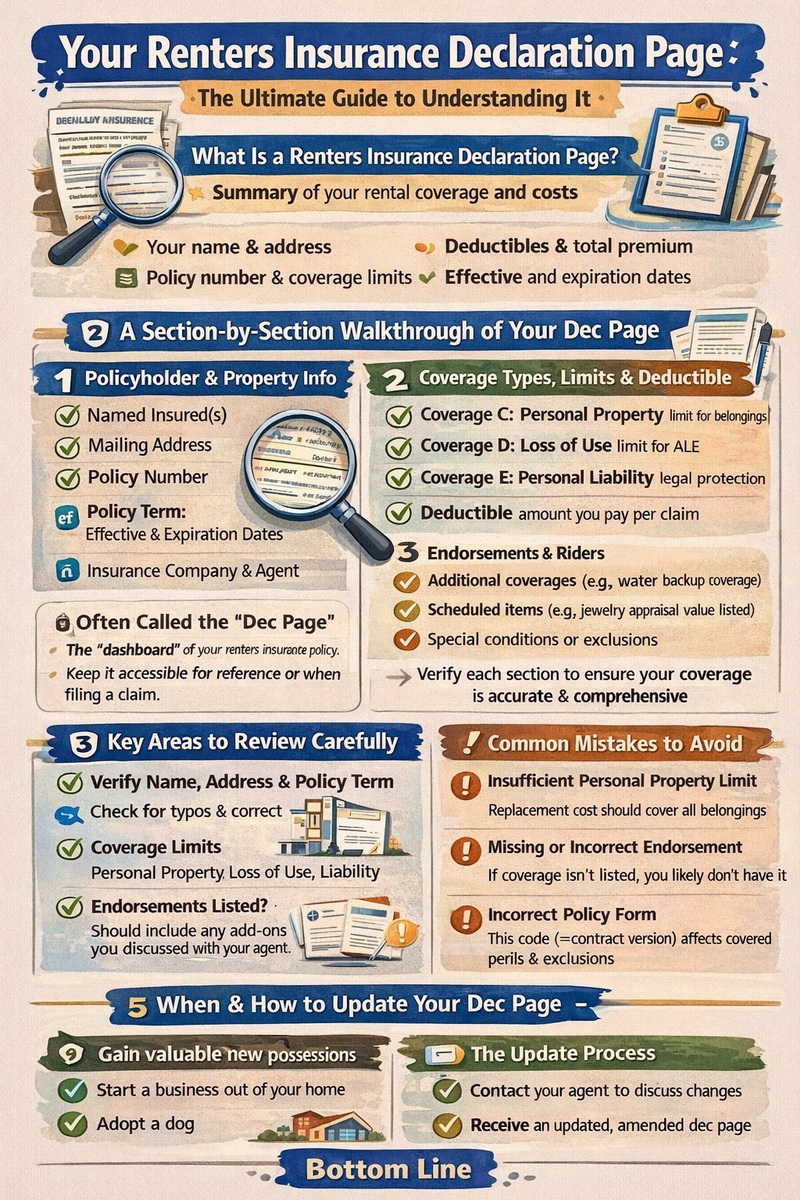

A renters insurance declaration page is the cornerstone of your policy, serving as a personalized snapshot of your coverage, limits, and costs. Often called the “dec page,” this front-page document summarizes the critical details of your agreement with the insurance company. It lists your name and address, policy number, effective dates, the exact coverages you’ve purchased (like personal property, liability, and loss of use), the associated limits and deductibles, and your total premium. Understanding your declaration page is non-negotiable for ensuring you have the right protection. It allows you to verify information is correct, confirm you’re not underinsured, and serves as the go-to reference in a crisis when you need to file a claim. This guide will dissect every section, explain common terms, and provide actionable steps for reviewing your document to guarantee your financial safety net is exactly as you intended.

What Is a Renters Insurance Declaration Page?

The renters insurance declaration page is the first and most important document in your policy packet. It is not the full contract but a concise, customized summary of its key elements created specifically for you. Think of it as the “dashboard” or “executive summary” of your renters insurance policy. Insurance companies are required to provide this document when you purchase or renew a policy. Its primary function is to offer immediate clarity on what is insured, for how much, under what terms, and at what price. Keeping this page accessible—whether in a physical file or digitally—is crucial, as you will need to reference your policy number and coverage details when speaking to your agent or filing a claim.

The Dec Page vs. The Full Policy

It’s vital to distinguish the declaration page from the complete policy wording. The dec page shows *your specific choices*: your limits, your deductible, your premium. The full policy booklet (often sent separately or available online) contains the standard “insuring agreement,” definitions, conditions, exclusions, and endorsements that apply universally. The declaration page personalizes those broad terms to your situation. Always review both, but the dec page is your quick-reference guide for the personalized aspects of your coverage.

Why This Single Page Is So Critical

The declaration page holds supreme importance for three reasons: Verification, Communication, and Action. It allows you to **verify** all personal information and coverage selections are accurate. It enables clear **communication** with your insurer, as you can cite specific coverage letters and limit amounts. Most importantly, it dictates the **action** and payout in a claim; the adjuster will use this document to determine what is covered and up to what financial amount. An error here can lead to being underinsured or having a claim denied.

A Section-by-Section Breakdown of Your Declaration Page

While formats vary by insurer, every renters insurance declaration page contains standard sections. Learning to navigate this document empowers you as a policyholder. Below is a detailed walkthrough of the common elements you will encounter and what they mean for your protection.

1. Policyholder and Property Information

This top section identifies you and the insured location. It includes:

- Named Insured(s): Your full legal name(s). If you have a roommate, ensure they are listed here if they are meant to be covered. A policy typically only covers named insureds.

- Mailing Address & Policy Address: The location of the rental property being insured. Verify this address is 100% correct.

- Policy Number: Your unique identifier. You’ll need this for all correspondence and claims.

- Policy Term: The effective date and expiration date. Coverage is only active between these dates.

- Insurance Company & Agent: The carrier underwriting the policy and your agent’s or agency’s contact information.

A single typo in your name or address can cause complications during a claim, making a careful review essential.

2. Coverage Sections, Limits, and Deductibles

This is the heart of the renters insurance declaration page. It outlines the types of coverage you have and their corresponding financial limits. Each is usually denoted by a “Coverage Letter” (e.g., Coverage A, B, C, D, E).

- Coverage C – Personal Property: The limit for your belongings. This is the maximum amount the insurer will pay if all your possessions are destroyed. Ensure this number reflects a realistic replacement cost, not just the cash value of old items.

- Coverage D – Loss of Use/Additional Living Expenses (ALE): Usually a percentage of your Coverage C limit (e.g., 20%). This pays for hotel and food if you’re displaced.

- Coverage E – Personal Liability: Crucial protection if you’re sued for injury or property damage. Standard limits start at $100,000, but $300,000+ is recommended.

- Coverage F – Medical Payments to Others: Covers minor medical bills for guests injured in your home, regardless of fault.

- Deductible: The amount you pay out-of-pocket on a property claim before insurance kicks in (e.g., $500). This is usually applied per claim.

For a comprehensive look at what these coverages entail, see our guide on renters insurance coverage details.

| Coverage Type (Typical Letter) | What It Protects | What to Check on Your Dec Page |

|---|---|---|

| Coverage C: Personal Property | Your belongings (furniture, electronics, clothing) from named perils like fire, theft, vandalism. | Is the limit sufficient? Is it “Actual Cash Value” (ACV) or “Replacement Cost Value” (RCV)? RCV is preferable. |

| Coverage D: Loss of Use | Additional living expenses if your rental is uninhabitable. | Confirm the limit (e.g., “30% of Coverage C”) is adequate for your area’s temporary housing costs. |

| Coverage E: Personal Liability | Your legal responsibility for injuries or property damage to others. | The limit should be high enough to protect your assets and future income ($300,000+ is wise). |

| Coverage F: Medical Payments | Small medical bills for guests hurt on your property. | Typically $1,000 to $5,000. Ensure it’s listed. |

| Deductible | Your share of a covered loss. | The dollar amount (e.g., $500, $1,000). A higher deductible lowers your premium but increases your out-of-pocket cost per claim. |

3. Endorsements, Riders, and Scheduled Personal Property

This section lists any add-ons or modifications to the standard policy. These are crucial as they extend or restrict coverage. Common items listed here include:

- Water Backup Coverage: Adds protection for sewer or drain backups.

- Identity Theft Coverage: Provides services and reimbursement for identity fraud expenses.

- Scheduled Personal Property: Items like expensive jewelry, musical instruments, or fine art that are listed individually with their appraised value because they exceed standard sub-limits.

- Earthquake or Flood: If purchased, these separate coverages will be noted here.

If you paid for an endorsement, it MUST appear on your renters insurance declaration page. Its absence means you likely don’t have that coverage.

How to Read and Audit Your Declaration Page for Errors

Receiving your declaration page is not a passive event; it requires an active review. A thorough audit ensures the contract matches your understanding and needs. Follow this checklist to verify your document is correct and your coverage is robust.

Step 1: Verify Personal and Policy Details

Immediately check for accuracy in:

- Spelling of your name(s).

- Complete and correct rental property address.

- Policy dates: Does the term align with your lease?

- Policy number is present and legible.

Contact your agent immediately to correct any errors in these foundational details.

Step 2: Scrutinize Coverage Limits Against Your Needs

This is the most critical audit step. Compare the limits on the page to your actual needs.

- Personal Property Limit: Does it match or exceed the total replacement value from your home inventory? If you’ve acquired new high-value items, this limit may need an increase.

- Liability Limit: In our litigious society, a $100,000 limit may be insufficient. Consider your net worth and potential future income. Increasing to $300,000 or $500,000 is often a smart, affordable move.

- Deductible: Can you comfortably afford to pay this amount if you have a claim? If not, you may need a lower deductible, which will increase your premium.

Understanding how these limits affect your premium can be complex; our resource on renters insurance cost can help you balance protection and price.

Step 3: Confirm Endorsements and Understand Exclusions

Locate the endorsements section. Are all the add-ons you discussed with your agent listed? If you wanted water backup or replacement cost coverage, are they explicitly stated? The flip side is understanding what’s *not* covered. While exclusions are detailed in the full policy, the declaration page may note major ones (like “Flood coverage not included”). Use this as a prompt to ask about separate policies for excluded perils you’re concerned about.

Common Mistakes and Red Flags to Identify

Even with careful review, some issues are commonly missed. Being aware of these red flags on your renters insurance declaration page can prevent devastating surprises later.

Mistake 1: Insufficient Personal Property Limit

The most frequent error is being underinsured. Many renters accept a default limit (e.g., $15,000) without realizing the replacement cost of their belongings is much higher. A detailed room-by-room inventory is the only way to combat this. Remember, this limit must cover everything from your sofa and TV to your clothing, kitchenware, and electronics.

Mistake 2: Missing or Incorrect Endorsements

You verbally requested “replacement cost” for your belongings, but the dec page still shows “actual cash value.” This is a major difference that significantly affects claim payouts. If an endorsement you believe you purchased is missing, contact your agent *in writing* to have it added and request an updated declaration page as proof.

Mistake 3: Overlooking the “Form” or “Edition” Number

Often near the top, you might see something like “Form HO-04” or “Edition 07-19.” This identifies which version of the insurer’s policy language applies. While it seems minor, different forms can have different covered perils and exclusions. Ensure you have the latest full policy document that matches this form number for your records. For authoritative information on standard policy forms and consumer rights, resources like the National Association of Insurance Commissioners (NAIC) are invaluable.

Taking Action: When and How to Update Your Declaration Page

Your renters insurance declaration page is a living document that should evolve with your life. Certain life events trigger an immediate need to review and potentially update your policy, generating a new dec page.

Life Events That Require a Policy Update

Contact your agent to update your policy and get a new declaration page if you:

- Acquire significant new valuables (e.g., an engagement ring, high-end laptop, musical instrument).

- Start a business from home that involves equipment or client visits.

- Get a dog (certain breeds may affect liability coverage).

- Move to a new rental property.

- Renovate your rental in a way that adds value to your possessions.

Failure to update your policy can result in a claim being denied for underinsurance or non-disclosure.

The Process for Making Changes

To make a change, contact your agent or insurer directly. They will:

- Discuss the change and its impact on your premium.

- Issue a “policy endorsement” or “rider” that formally amends the contract.

- Provide you with a new, updated renters insurance declaration page that reflects the change.

Never assume a change is effective until you receive and review that updated document. Store all old dec pages together to maintain a history of your coverage.

Conclusion

Your renters insurance declaration page is far more than a bill or a formality; it is the definitive blueprint of your financial protection as a renter. Taking the time to understand every section, from your personal liability limit to the list of endorsements, empowers you to take control of your insurance. A careful, annual audit of this document, especially after major life changes, is a non-negotiable habit for savvy renters. It ensures you are neither overpaying for unnecessary coverage nor—more dangerously—underinsured against life’s unexpected events. By using this guide to decode your dec page, you transform from a passive policyholder into an informed consumer, confident that your renters insurance safety net is securely in place, exactly as you designed it. Keep it safe, know it well, and you’ll have peace of mind that extends far beyond your rental’s walls.

Frequently Asked Questions (FAQ)

Is the declaration page proof of insurance?

Yes, the renters insurance declaration page is universally accepted as proof of insurance. Most landlords and property management companies require a copy of this specific document before you move in, as it concisely shows your coverage limits and effective dates. It serves as your official certificate of insurance.

How often should I review my declaration page?

You should review your renters insurance declaration page thoroughly at three key times: 1) When you first receive a new policy, 2) At every annual renewal, and 3) Any time you experience a significant life change (like acquiring expensive items or moving). An annual review is the minimum best practice to ensure your coverage keeps pace with your life.

What’s the difference between “RCV” and “ACV” on my dec page?

This is a critical distinction often found in the personal property section. Replacement Cost Value (RCV) means the insurer will pay the cost to replace a damaged item with a new one of similar kind and quality, without deducting for depreciation. Actual Cash Value (ACV) pays the replacement cost minus depreciation (age, wear, and tear). RCV results in much higher claim payouts and is highly recommended, though it comes with a slightly higher premium.

Why is my premium different on the dec page than the quote I received?

The final premium on your renters insurance declaration page can differ from an initial quote for a few reasons: The insurer may have run a soft credit check (where permitted) which affected your rate, you may have selected different deductible or limit options during the final application, or applicable state taxes and fees were added. The dec page shows the final, binding premium you are obligated to pay.

Can I make a claim using just the declaration page?

You can and should initiate a claim using the information on your declaration page (especially your policy number). However, the actual claims adjustment process will be governed by the full policy terms, conditions, and exclusions detailed in the complete policy booklet. The adjuster will use the dec page to identify your coverages and limits but will reference the full contract for specific rules.

What if I lose my declaration page?

If you lose your renters insurance declaration page, contact your insurance agent or company immediately. They can email, fax, or mail you a duplicate copy at no charge. Most insurers also provide 24/7 online portals or mobile apps where you can view and download your current dec page and other policy documents instantly.

Does my roommate need to be on my declaration page?

If you want your roommate to have coverage under the policy, they must be listed as a “named insured” on the renters insurance declaration page. If they are not listed, their belongings will not be covered, and they likely cannot file a liability claim under your policy. It’s best for roommates to have a joint policy or separate individual policies to avoid coverage gaps and conflicts.