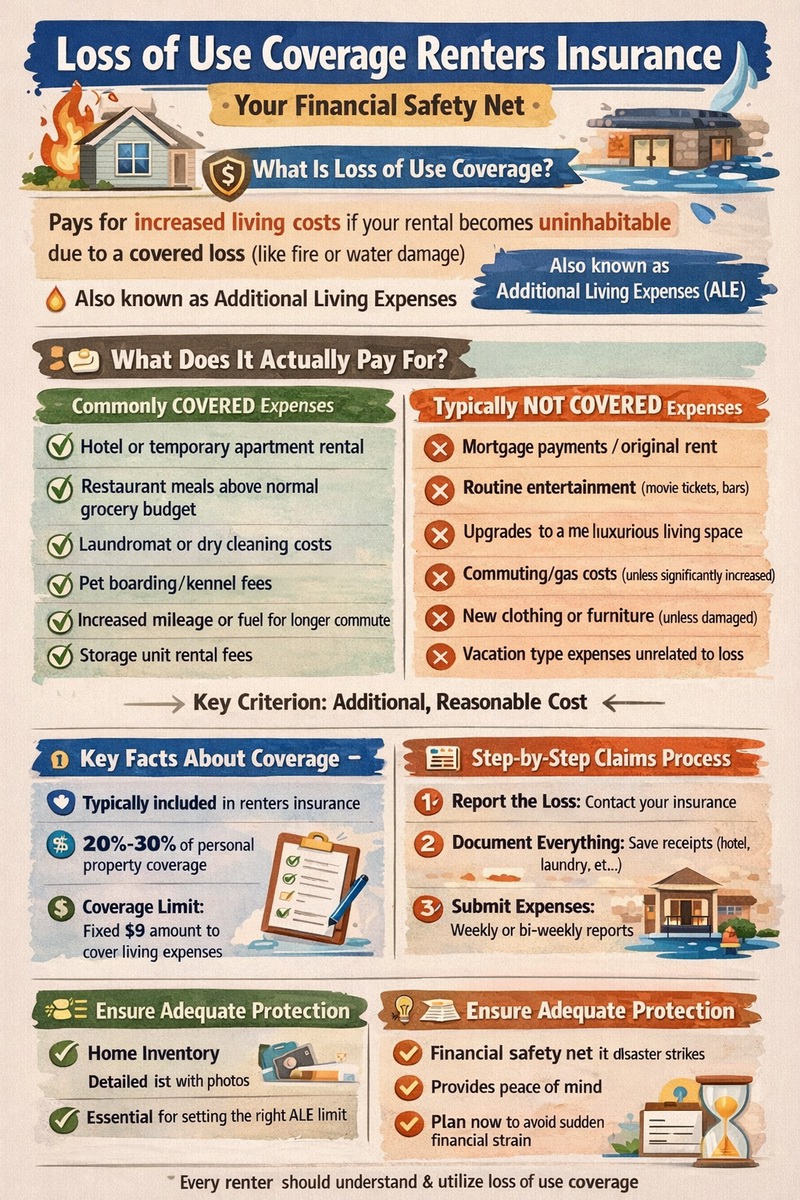

Loss of use coverage renters insurance, also known as Additional Living Expenses (ALE), is a critical component of a standard renters policy that many overlook until disaster strikes. This coverage acts as a financial safety net, paying for the increased costs you incur if your rented home becomes uninhabitable due to a covered peril like a fire, severe water damage, or other insured disaster. It covers expenses such as hotel stays, restaurant meals, laundry services, pet boarding, and even temporary rental costs, ensuring your standard of living is maintained while your primary residence is being repaired. Understanding the limits, what qualifies as a “covered loss,” and how to file a claim is essential for every renter. This coverage provides peace of mind, knowing that in a crisis, you won’t be burdened with doubling your housing costs out of pocket.

What Is Loss of Use Coverage in Renters Insurance?

Loss of use coverage is a standard inclusion in most renters insurance policies designed to protect you from the financial strain of displacement. When a covered event—such as a fire, burst pipe, or vandalism—renders your rental unit temporarily unlivable, this coverage pays for the “additional” costs of living elsewhere. It’s not meant to improve your lifestyle but to keep it as close to normal as possible during a disruptive time. The core principle is to cover the difference between your regular living expenses and your new, necessary, and higher expenses. It’s a feature that transforms a renters insurance policy from simply protecting your stuff to protecting your entire living situation.

The Definition and Purpose of ALE

Additional Living Expenses (ALE) is the technical term used by insurance companies for loss of use coverage. Its sole purpose is financial indemnification for increased costs. For example, if your normal monthly expenses for rent, utilities, and food are $1,500, and a fire forces you into a hotel and restaurants, raising your monthly costs to $3,500, ALE would cover the $2,000 difference. This prevents you from draining your savings or going into debt because of an unforeseen insured disaster, allowing you to focus on recovery rather than finances.

How It Integrates with Your Policy

Loss of use coverage is typically included as a percentage of your personal property coverage limit (Coverage C). A common percentage is 20% to 30%. For instance, if you have $30,000 in personal property coverage, your loss of use limit might be $6,000 to $9,000. This is a separate limit specifically for ALE claims. It’s crucial to know this limit, as it caps the total amount your insurer will pay for your temporary living expenses, regardless of how long repairs take.

What Does Loss of Use Coverage Actually Pay For?

Loss of use coverage renters insurance is remarkably practical, covering a wide array of necessary expenses incurred because you cannot live in your home. The key criterion is that the expense must be “additional” and “reasonable.” Insurance adjusters will review claims with this lens, ensuring costs align with maintaining your pre-loss standard of living without luxury upgrades.

Primary Housing and Accommodation Costs

This is the most significant category. ALE will cover the cost of a temporary place to live. This could be a hotel, a motel, a short-term rental apartment, or an extended-stay suite. The covered cost should be reasonably comparable to your original living situation; you cannot typically claim a penthouse suite if you lived in a studio apartment. The coverage includes the rent or room rate, plus any mandatory taxes and fees associated with the temporary lodging.

Food, Laundry, and Daily Living Expenses

When you don’t have access to a kitchen, eating out becomes a necessity, not a luxury. ALE covers the increased cost of meals. Insurers usually calculate this by comparing what you normally spend on groceries to what you now spend on restaurants. They may use a per diem rate (a daily allowance). Similarly, if you need to use a laundromat because your temporary housing lacks laundry facilities, those extra costs are covered. Storage unit fees for your belongings during repairs are also a common reimbursable expense.

Storage unit rental feesExpenses not related to the loss of use (e.g., a vacation you had planned)

| Commonly COVERED Expenses | Typically NOT COVERED Expenses |

|---|---|

| Hotel or temporary apartment rental | Mortgage payments or your original rent (paid to landlord) |

| Restaurant meals above normal grocery budget | Routine entertainment (movie tickets, bars) |

| Laundromat or dry cleaning costs | Upgrades to a more luxurious living space |

| Pet boarding/kennel fees | Commuting/gas costs unless significantly increased |

| Increased mileage or fuel for a longer commute | New clothing or furniture (unless damaged and claimed under personal property) |

Key Factors, Limits, and How to File a Claim

To effectively utilize loss of use coverage renters insurance, you must understand its triggers, limitations, and the proper claims process. Being proactive and organized can make a significant difference in how smoothly your claim is processed and paid.

What Triggers Loss of Use Coverage?

The coverage is only activated by a “covered peril” that makes your home “uninhabitable.” Covered perils are listed in your policy and typically include fire, lightning, windstorm, hail, theft, vandalism, and damage from falling objects. The definition of uninhabitable is key: it means the property is unsafe or unfit to live in due to the damage. A minor repair that is an inconvenience does not qualify. The determination is often made by a claims adjuster or local authorities (like the fire department condemning the building).

Understanding Your Policy Limits and Timeframe

As mentioned, your ALE limit is a percentage of your personal property coverage. This is a finite amount. Coverage continues until one of two things happens: your home is repaired and ready to occupy, or you reach your policy limit. There is also typically a “time element” involved; the expenses must be incurred during the “period of restoration.” It’s vital to communicate with your adjuster about estimated repair times and keep track of your spending against your limit. For a full understanding of how policy limits work within your overall renters insurance coverage, reviewing your policy details is essential.

The Step-by-Step Claims Process for ALE

1. Report the Loss: Immediately contact your insurance company to report the damage and initiate a claim. Inform them you will need loss of use benefits.

2. Document Everything: Keep meticulous records. Save all receipts for hotels, meals, laundry, pet boarding, and mileage. Take photos of the damage to your rental unit.

3. Understand Your Benefits: Ask your claims adjuster to explain your specific ALE limit, any per diem rates for food, and what documentation they require.

4. Submit Expenses Regularly: Don’t wait until the end. Submit your receipts and a log of expenses weekly or bi-weekly for reimbursement. This helps manage your cash flow and keeps the claim active.

5. Maintain Communication: Stay in close contact with your adjuster regarding the repair timeline. If repairs are delayed, inform them, as this may affect the duration of your ALE benefits.

Real-World Scenarios and Common Misconceptions

Examining practical examples helps clarify how loss of use coverage renters insurance functions in everyday crises. It also dispels common myths that can leave renters underprotected or confused about their benefits.

Scenario 1: Kitchen Fire in an Apartment

A cooking fire causes significant smoke and fire damage to your apartment. The fire department declares it unsafe due to structural and air quality concerns. Your loss of use coverage would pay for a hotel for you and your family. It would cover restaurant meals because you have no kitchen. It would also cover extra gas costs if the hotel is farther from your workplace. This continues until the landlord completes repairs and the unit is certified safe, or until you exhaust your ALE limit.

Scenario 2: Major Water Damage from a Burst Pipe

A pipe bursts in the unit above you, flooding your apartment and damaging floors and electrical outlets. The landlord says repairs will take six weeks. Your ALE coverage would pay for a short-term furnished rental. It would cover the cost of using a laundromat if the rental doesn’t have a washer/dryer. If you have a pet that isn’t allowed in the temporary rental, boarding fees would be covered. The coverage helps you maintain a normal routine despite the major disruption.

Debunking Common Myths About ALE

Myth: “My landlord will pay for my hotel.”

Truth: The landlord’s insurance covers damage to the building, not your temporary living costs. That’s your insurer’s role via ALE.

Myth: “I can upgrade to a nicer place since it’s covered.”

Truth: Insurers pay for costs that are reasonably comparable to your previous living standard. A major upgrade likely won’t be fully reimbursed.

Myth: “It covers all my expenses with no limit.”

Truth: It covers *additional* expenses up to a strict policy limit (e.g., 20% of personal property coverage). You must manage expenses within this cap.

How to Ensure You Have Adequate Loss of Use Protection

Given that loss of use coverage renters insurance is tied to your personal property limit, ensuring you have enough overall coverage is the first step to having sufficient ALE. A common mistake is undervaluing belongings, which consequently provides a dangerously low ALE limit for a prolonged displacement.

Conducting a Thorough Home Inventory

The foundation of adequate renters insurance is a detailed home inventory. List all your possessions with descriptions, purchase dates, and estimated values. Use photos or video. This serves two purposes: it ensures you purchase enough personal property coverage, and by extension, it raises your ALE limit. Online tools or apps can help with this process. Remember, the cost to replace all your belongings new (Replacement Cost Value) is often much higher than you think.

Evaluating and Increasing Your ALE Limit

Once you know your personal property value, review your policy’s ALE percentage. If it’s 20%, calculate that amount. Ask yourself: “If I had to live in a hotel and eat out for 3-6 months, would this amount cover it?” In high-cost-of-living areas, a 30% limit may be more appropriate. Many insurers allow you to increase this percentage for a slightly higher premium, which is a wise investment. Understanding these calculations is part of evaluating your overall renters insurance cost and value.

The Importance of “Fair Rental Value” Coverage

Some policies also include a small amount of “Fair Rental Value” coverage, which is different from ALE. This applies if you were subletting part of your unit and lose that rental income due to a covered loss. For most standard renters, ALE is the primary concern. However, understanding all parts of your policy, including seeking clarity from authoritative sources like the Insurance Information Institute, ensures you have no gaps in your financial protection.

Conclusion

Loss of use coverage renters insurance is an indispensable component of a well-structured policy, offering critical financial support when you are most vulnerable. It goes beyond protecting physical possessions to safeguard your living stability after a disaster. By understanding what it covers, how it’s triggered, and the importance of your policy limits, you can confidently navigate a displacement knowing your additional living expenses are secured. Every renter should review their policy today, confirm their ALE limit, and consider increasing it if necessary. This small step, often for a minimal increase in premium, provides enormous peace of mind. For comprehensive protection that covers your belongings, your liability, and your ability to maintain a home, a robust renters insurance policy with strong loss of use coverage is not just a recommendation—it’s a fundamental part of responsible renting.

Frequently Asked Questions (FAQ)

Does loss of use coverage pay for my regular rent?

No. Loss of use coverage pays for your *additional* living expenses, not your ongoing rent or mortgage. You are still contractually obligated to pay rent to your landlord during repairs unless your lease states otherwise. ALE covers the cost of your temporary housing *on top of* your existing rent obligation.

How long does loss of use coverage last?

It lasts for the “reasonable time” required to repair or replace your rented home, up to your policy limit. There is no set number of days. If repairs take two months, coverage lasts two months. If they take six months but you hit your financial limit after four months, coverage stops. The timeframe is directly tied to the repair timeline and your policy’s maximum payout.

What if I can stay with family or friends for free?

If you stay with family or friends for free, you may still be eligible for some ALE benefits. Many policies will pay a “customary hospitality” rate, which is a reduced per diem amount intended to compensate your hosts for the extra utilities and food costs they incur because of you. You should still discuss this with your claims adjuster and keep records of any related expenses.

Does it cover expenses for my pets?

Yes, in most cases. If your temporary housing does not allow pets, or if it’s impractical to bring them, the reasonable cost of boarding your pets at a kennel or similar facility is typically covered as an additional living expense. Always save the receipts and confirm with your adjuster before incurring the cost.

Is there a deductible for loss of use claims?

Generally, no. The deductible on your renters insurance policy typically applies to claims for personal property damage (Coverage C). Since loss of use (Coverage D) is a separate coverage for additional expenses, it is usually paid without a deductible. However, you should always verify this with your specific policy, as terms can vary.

What if the disaster is my fault, like a kitchen fire I started?

Your loss of use coverage should still apply. Renters insurance covers “sudden and accidental” losses, even if you are negligent (like accidentally starting a fire). It would not cover intentional damage. So, if you accidentally cause a covered loss that makes your home uninhabitable, your ALE benefits are still available to you.

Can I choose any hotel I want?

You have a choice, but it must be reasonable. The insurance company will expect you to choose lodging that is reasonably comparable to your original living situation in terms of size and quality. Choosing a luxury resort when a standard hotel suite is available may result in the insurer only reimbursing you for the reasonable cost, leaving you to pay the difference.