Standard renters insurance does NOT automatically cover unrelated roommates. A typical policy covers the “named insured” and their relatives who live with them. If you have a roommate who is not related by blood, marriage, or adoption, they are not covered under your policy for their personal property or liability. To ensure everyone is protected, the safest and most common recommendation is for each roommate to purchase their own separate renters insurance policy. While some insurers offer a “roommate policy” where all roommates are named on one policy, this can lead to complications with claims, premium splitting, and policy changes if someone moves out. For foundational knowledge, see our guide on what renters insurance is.

Why One Policy Rarely Works for Unrelated Roommates

When asking “does renters insurance cover roommates?” it’s crucial to understand the insurance contract’s purpose. It’s designed to protect a single “insured” household, typically defined as a family unit. Insurers see unrelated roommates as separate financial entities with separate property and separate liability exposures. Combining them on one policy creates an “insurable interest” problem and complicates risk assessment.

What Happens Under a Single Policy (If You’re Not Named)?

If only one roommate has a policy and a loss occurs:

– Personal Property: Only the named insured’s belongings are covered. The roommate’s destroyed laptop or clothing would not be reimbursed.

– Liability: If the uninsured roommate causes a fire or injures a guest, the policy’s liability coverage likely would not protect them. They could be sued personally.

– Claims Payout: For shared items (like a living room TV), the insurance check would be made out only to the named insured, creating potential conflict over the money.

This leaves significant gaps in the overall renters insurance coverage for the household.

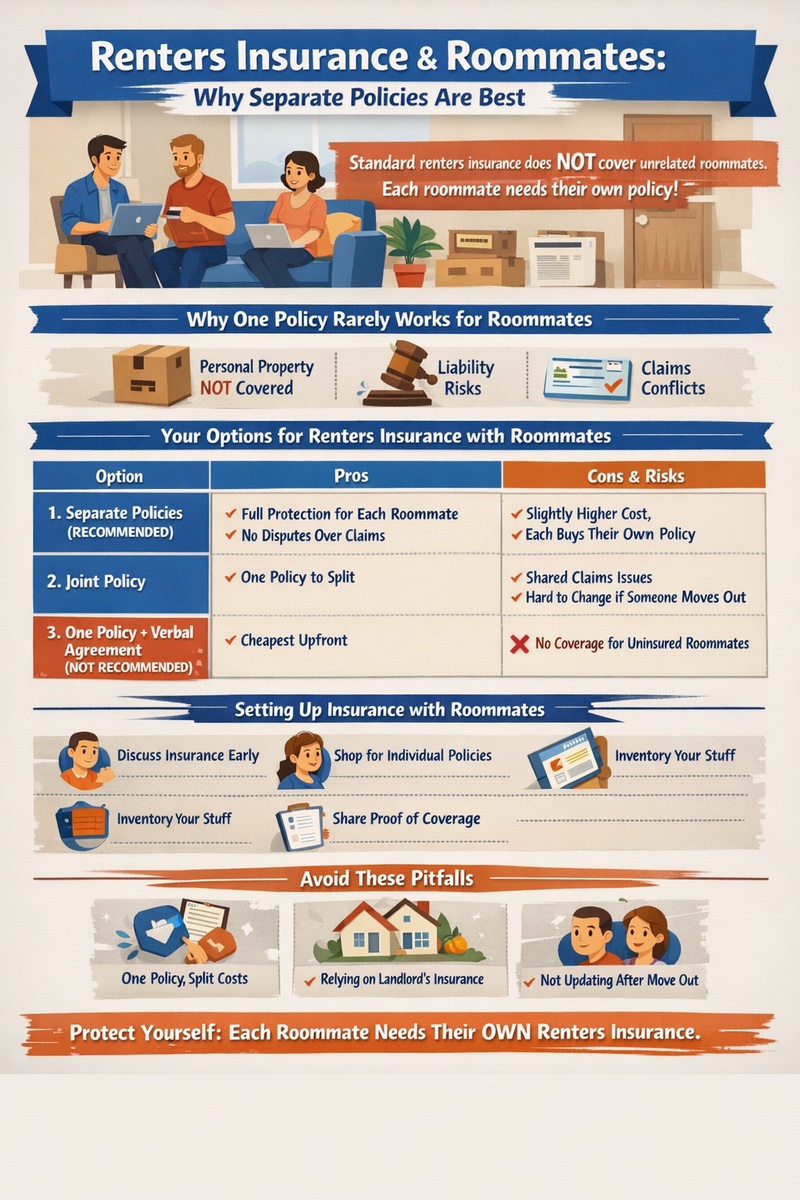

Your Options for Insuring a Household with Roommates

The following table outlines the three main approaches to renters insurance with roommates, comparing their pros, cons, and key considerations.

| Option | How It Works | Pros | Cons & Risks |

|---|---|---|---|

| 1. Separate Individual Policies (RECOMMENDED) | Each roommate buys their own renters insurance policy from the same or different companies. | – Clear, separate coverage for each person’s stuff and liability. – No disputes over claims payouts. – Easy to adjust/cancel when someone moves out. – Each person can customize their own limits and endorsements. |

– Slightly higher total cost than one shared policy (but not by much). – Requires each person to be proactive. |

| 2. Joint (Roommate) Policy | All roommates are listed as “named insureds” on a single policy. (Not all insurers offer this.) | – One bill to split. – May be slightly cheaper than two separate policies. – Ensures everyone has at least a baseline of coverage. |

– Claims checks are issued jointly, which can lead to major disputes. – One roommate’s claims history affects all policyholders. – If one roommate cancels or moves, the entire policy may need revision/cancellation. – Difficult to customize coverage per person. |

| 3. One Policy + Verbal Agreement (NOT RECOMMENDED) | One roommate buys a policy and verbally agrees to cover shared items or split claims. | – Cheapest upfront cost (only one premium). | – The uninsured roommates have NO coverage for their property or liability. – Illegal and violates the policy contract. – Guarantees massive conflict and potential lawsuits after a loss. |

Key Considerations for Shared Property

Even with separate policies, you need a plan for common items. Who owns the living room sofa, TV, or dining table? Options:

1. Designated Owner: One person owns and insures it under their policy.

2. Proportional Ownership: Each roommate insures their share of the item’s value on their own policy (hard to manage).

3. Joint Purchase Documentation: Keep receipts showing who paid what. Discuss in advance how a claim would be handled.

The best practice is to minimize shared, high-value property.

Steps to Set Up Proper Insurance with Roommates

Follow this action plan to ensure full protection and avoid headaches:

1. Have a Roommate Meeting Early. Discuss insurance as part of moving in together, just like utilities.

2. Decide on the Structure. Strongly advocate for separate individual policies. It’s the cleanest solution.

3. Shop for Quotes. Each roommate can get their own quotes. You can all use the same insurer for simplicity, but it’s not required.

4. Inventory Your Own Belongings. Each person should create their own home inventory for their bedroom and personal items. Document shared items and their ownership.

5. Purchase Policies & Share Proof. Once everyone has a policy, share certificates of insurance (COIs) with each other and your landlord if required. This proves everyone is covered.

6. Update After Life Changes. If a roommate moves out, the remaining roommates should inform their insurers of the change in household composition. The departing roommate cancels or moves their policy.

What About a Couple or Married Roommates?

If roommates are related by marriage, domestic partnership, or are a couple in a committed relationship living together, they can and should be on the same policy as named insureds. This is the standard and correct approach for a family unit.

Common Pitfalls and Disputes to Avoid

– “We’ll just split the cost of one policy.” This leaves the non-named roommates completely exposed. Don’t do it.

– Assuming your landlord’s policy covers you. It does not. This is a separate, critical misconception.

– Not updating policies after a move-out. An ex-roommate’s liability could still be tied to a joint policy if not removed.

– Underinsuring because “we share stuff.” Each person still needs adequate limits for their own clothing, electronics, furniture, and liability.

Proper planning is part of managing your overall renters insurance cost responsibly. For a full market view, explore all renters insurance options.

Conclusion: Protect Your Own Assets

In summary, does renters insurance cover roommates? Not unless they are specifically named on the policy, and even then, a joint policy is fraught with risk. The simplest, most effective, and most conflict-free strategy is for each unrelated roommate to secure their own individual renters insurance policy. This ensures that everyone’s personal property is protected, everyone has their own liability shield, and no one is left financially vulnerable due to another’s mistake or a shared disaster. Have the conversation upfront, make it a non-negotiable part of your living agreement, and enjoy your shared home with the peace of mind that comes from proper protection.

Frequently Asked Questions (FAQ)

Can my landlord require all roommates to have renters insurance?

Yes, absolutely. More landlords are making renters insurance mandatory for each tenant on the lease. The lease may specify that each occupant must provide their own certificate of insurance with minimum liability limits (e.g., $100,000). This is a growing best practice that protects both the tenant and the landlord.

What if my roommate has a dog that bites someone? Whose insurance covers it?

Liability follows the dog’s owner. If your roommate’s dog bites a guest, your roommate’s renters insurance liability coverage (if they have a policy and the breed is not excluded) should respond. Your policy would not cover your roommate’s pet. If the dog is jointly “owned,” it creates a complex liability scenario best avoided.

If we have a joint policy and my roommate causes a fire, will my belongings be covered?

Yes, your personal property should be covered under the joint policy’s personal property coverage, as you are a named insured. However, the claim will be filed under the single policy, affecting the claims history for all named insureds, which will likely lead to a premium increase or non-renewal for everyone when the policy renews.

Are subletters covered under my renters insurance?

No. If you sublet your room to someone, they are not covered under your policy. They need to purchase their own renters insurance. Furthermore, subletting may violate your lease and your insurance policy terms, potentially voiding your coverage. Always check with your landlord and insurer first.

How much does renters insurance cost per person for roommates?

Renters insurance is very affordable individually. Each policy might cost $12-$20 per month ($150-$240 annually). The total for two separate policies might be $300-$480 per year, which is only marginally more than one joint policy. The slight extra cost is worth the elimination of risk and conflict.

What documents should we keep to prove who owns what?

Keep receipts for major purchases, especially shared ones. Take a photo of the receipt with your phone and store it in the cloud. For items without receipts, take a group photo with the item on move-in day. A simple shared spreadsheet listing major items and their owners can also prevent disputes.

Where can I find a sample roommate agreement that includes insurance?

While we don’t provide legal documents, the Insurance Information Institute’s article on renters insurance underscores its importance. For a formal roommate agreement, consult legal websites or a local tenants’ rights organization for templates that include clauses on insurance responsibilities.