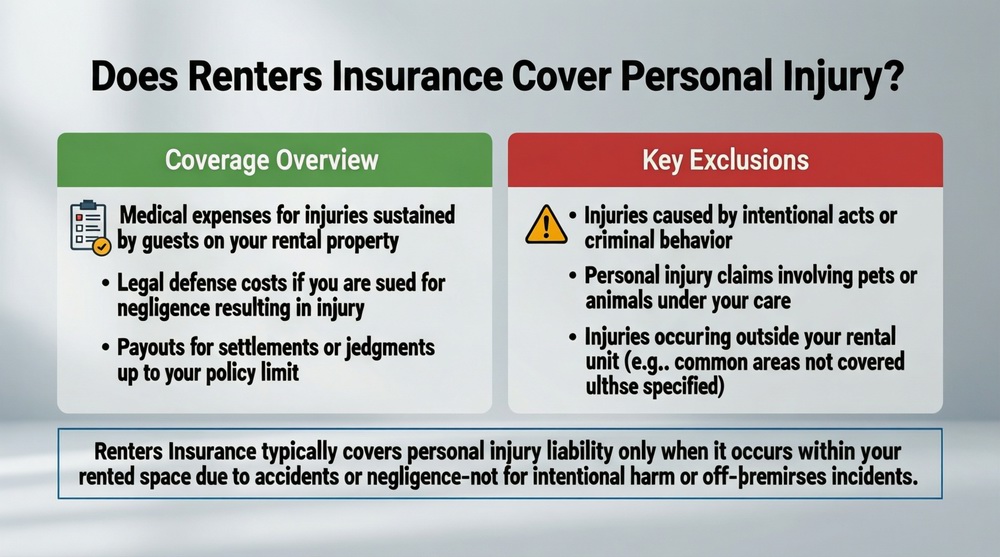

Yes, renters insurance does cover personal injury through two distinct but complementary coverages: Personal Liability (Coverage E) and Medical Payments to Others (Coverage F). If you are found legally responsible (“liable”) for someone’s bodily injury (e.g., a guest slips on your wet floor and breaks a wrist), your liability coverage pays for their medical bills, lost wages, and your legal defense, up to your policy limit. Medical Payments is a no-fault coverage that pays smaller medical bills (e.g., $1,000-$5,000) for guests injured in your home, regardless of who is at fault. However, it’s crucial to understand that “personal injury” in insurance typically refers to physical bodily injury, not non-physical harms like emotional distress or libel, unless you have a specific “personal injury” endorsement. For the basics, see our guide on what renters insurance is.

Personal Liability Coverage: Your Financial Shield

When asking “does renters insurance cover personal injury?” in the context of being sued, you’re referring to Coverage E: Personal Liability. This is the core protection against financial ruin if you are held legally liable for causing bodily injury or property damage to others. It covers the injured party’s economic and non-economic damages, as well as your legal costs.

What Does Personal Liability Cover?

Liability coverage activates if you are found negligent and that negligence causes injury. Common covered scenarios include:

– Slip and Fall Accidents: A guest trips over a loose rug or slips on a recently mopped floor.

– Dog Bites: Your pet injures a visitor or neighbor (subject to breed exclusions).

– Accidents Away From Home: You accidentally injure someone while playing sports or cause damage elsewhere (e.g., your child hits a baseball through a neighbor’s window, injuring someone inside).

– Injuries from a Condition on Your Property: A falling balcony railing or poorly maintained step causes injury.

The coverage pays for the injured person’s medical expenses, rehabilitation, lost income, and “pain and suffering.” It also pays for your attorney fees, court costs, and any settlement or judgment up to your policy limit (e.g., $100,000, $300,000). This is a fundamental part of your renters insurance coverage.

Choosing the Right Liability Limit

A single serious injury can result in a lawsuit for hundreds of thousands of dollars. Standard limits of $100,000 are often inadequate. It is strongly recommended that renters carry at least $300,000 to $500,000 in personal liability coverage. The premium increase for higher limits is usually very small. For even greater protection, consider an umbrella policy, which provides an additional $1 million or more in coverage.

Medical Payments to Others: No-Fault, Immediate Help

Medical Payments (MedPay) is designed to prevent small accidents from turning into big lawsuits. It provides prompt payment for necessary medical expenses when someone is injured on your property, regardless of who is at fault.

How Medical Payments Coverage Works

– Scope: Covers medical and dental expenses, ambulance fees, X-rays, and even crutches.

– Limit: Typically $1,000 to $5,000 per person, per accident.

– Who is Covered: Guests and social visitors in your home. It usually does not cover you or members of your household.

– Example: A guest cuts their hand on a broken glass in your kitchen sink. They go to the ER for stitches, costing $800. They can submit the bill to your insurer under MedPay, and it will be paid quickly without determining fault or involving liability coverage. This goodwill gesture can often prevent a larger liability claim.

What “Personal Injury” Coverage Typically Does NOT Include

It’s vital to understand the insurance definition of “personal injury.” In standard renters policies, it means physical bodily injury. It does not cover:

| Type of Injury / Claim | Covered by Standard Liability/MedPay? | Explanation & Alternatives |

|---|---|---|

| Bodily Injury from a Slip and Fall | YES (Liability & MedPay) | The core purpose of the coverage. |

| Libel, Slander, Defamation | NO (unless endorsed) | Considered “personal injury” in a legal sense but requires a separate “Personal Injury” endorsement to a renters policy. |

| False Arrest, Invasion of Privacy | NO (unless endorsed) | Also falls under the “personal injury” endorsement category. |

| Emotional Distress (without physical injury) | Typically NO | Very difficult to claim under standard bodily injury liability. |

| Injuries to You or Household Members | NO | Your own medical bills are covered by your health insurance, not renters insurance. |

| Business or Professional Liability | NO | If you run a business from home and a client is injured, you need separate business insurance. |

| Intentional Injuries | NO | Any harm you intentionally cause is excluded. |

The “Personal Injury” Endorsement for Non-Physical Harms

For protection against lawsuits alleging libel, slander, defamation, false arrest, or invasion of privacy, you can add a “Personal Injury” endorsement (not to be confused with “bodily injury liability”) to your renters policy. This is particularly relevant for bloggers, social media influencers, or anyone in a public-facing role. Ask your agent about its availability and cost.

The Claims Process for a Personal Injury Incident

If someone is injured in or because of your rental, take these steps:

1. Ensure Safety and Provide Aid: Administer first aid if appropriate and call 911 for serious injuries.

2. Be Compassionate, But Do Not Admit Fault. Avoid statements like “I’m so sorry, this is all my fault.” Simply express concern for their well-being.

3. Document the Incident. Take photos of the accident scene, note the names and contact information of any witnesses, and write down your own account while details are fresh.

4. Notify Your Insurance Company. Contact your renters insurance provider promptly to report the incident, even if it seems minor. They can advise if a MedPay or liability claim is likely.

5. Cooperate with Your Insurer. Provide all documentation and information. If a lawsuit is filed, your insurer will appoint a lawyer to defend you.

6. Do Not Discuss the Case or Make Payments. Refer all communications from the injured party or their attorney to your insurance adjuster.

How Your Deductible Applies

The deductible on your renters insurance typically does not apply to liability or medical payments claims. If a MedPay claim is $1,000, the insurer pays the full $1,000. If a liability settlement is $50,000, the insurer pays $50,000 (up to your limit). Your deductible usually only applies to claims for your own personal property.

Maximizing Your Protection: Limits and Umbrella Policies

Given the high cost of medical care and litigation, carrying adequate limits is non-negotiable. Review your policy to ensure your liability limit reflects your net worth and risk exposure. As your assets grow, so should your liability limit. A personal umbrella policy is a cost-effective way to add $1 million or more in liability coverage on top of your renters (and auto) insurance. For a few hundred dollars a year, it provides catastrophic protection. Understanding these layers is part of managing your overall renters insurance cost effectively. Explore all renters insurance options to ensure you have robust liability protection.

Conclusion: Essential Protection for a Litigious World

So, does renters insurance cover personal injury? Yes, it provides a critical two-tiered defense. Medical Payments offers a quick, no-fault way to handle minor injuries, potentially preventing disputes. Personal Liability provides a robust legal and financial defense if you are sued for more serious bodily injury. While it doesn’t cover non-physical personal injury claims without an endorsement, its core function is to protect your financial future from the potentially devastating costs of an accident for which you are found responsible. Don’t skimp on this coverage—increase your limits, consider an umbrella policy, and rest easier knowing you have a strong safety net in place.

Frequently Asked Questions (FAQ)

Does renters insurance cover my own medical bills if I’m injured at home?

No. Renters insurance is designed to protect you from claims made by others and to protect your belongings. Your own medical bills from an accident in your home are covered by your health insurance or, in some cases like a slip and fall, possibly by disability insurance. Medical Payments (MedPay) is exclusively for guests.

If my dog bites someone, am I covered?

Yes, typically, but with important caveats. Dog bites are a common liability claim. However, many insurers have breed restrictions and may exclude coverage for breeds like Pit Bulls, Rottweilers, or dogs with a prior bite history. You must disclose your pet, and if it’s a restricted breed, you may need to find a specialty insurer or a separate animal liability policy.

What if someone is injured at a party I’m hosting?

Your renters liability coverage generally applies to social gatherings at your home. If a guest is injured (e.g., trips, burns themselves, gets in a fight), your liability coverage could respond. However, if you serve alcohol and someone leaves your party and causes a car accident, you could face “social host liability.” Coverage for this varies by state law and policy; some policies may exclude it. Serve alcohol responsibly.

Are delivery persons or contractors covered if injured at my home?

Yes, typically. If a mail carrier, food delivery person, or hired contractor (like a plumber) is injured on your property due to a hazardous condition (ice on steps, a loose floorboard), your liability coverage may apply. However, hired contractors should carry their own workers’ compensation insurance, which would be primary for work-related injuries.

How does renters insurance handle a lawsuit?

Your insurance company has a “duty to defend” you. If you are sued for a covered incident, they will appoint and pay for a defense attorney. They will investigate the claim, negotiate with the plaintiff’s attorney, and if a settlement is reached or a judgment is awarded (up to your policy limit), they will pay it. You are responsible for any amount that exceeds your policy limit.

Does medical payments coverage encourage people to sue me?

It’s designed to do the opposite. By offering to pay small medical bills quickly and without argument, it fosters goodwill and can prevent the injured party from hiring a lawyer to pursue a larger liability claim. It’s a proactive, relatively inexpensive way to manage minor incidents.

Where can I find more information on liability risks?

The Insurance Information Institute’s guide to renters insurance provides authoritative, detailed explanations of liability coverage, medical payments, and how they work together to protect you from personal injury claims.