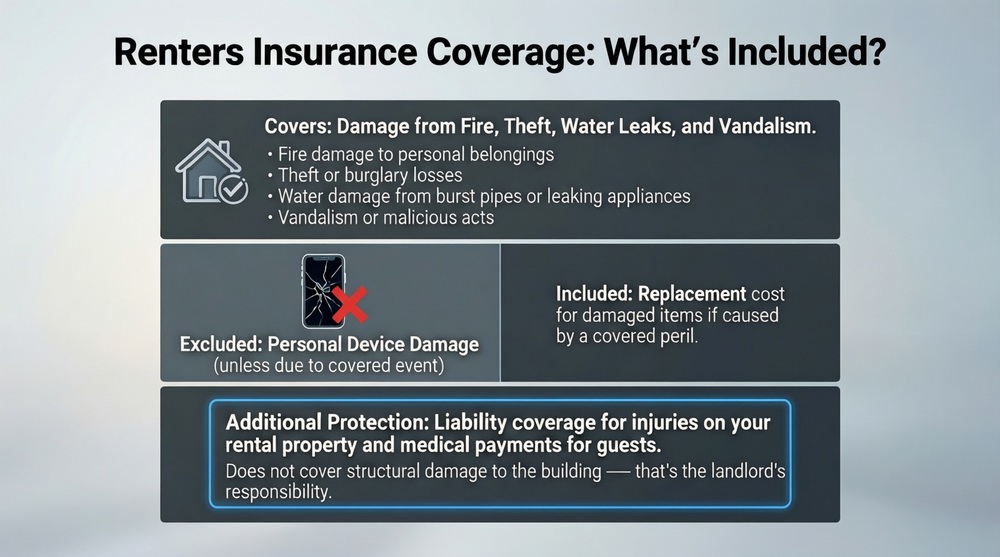

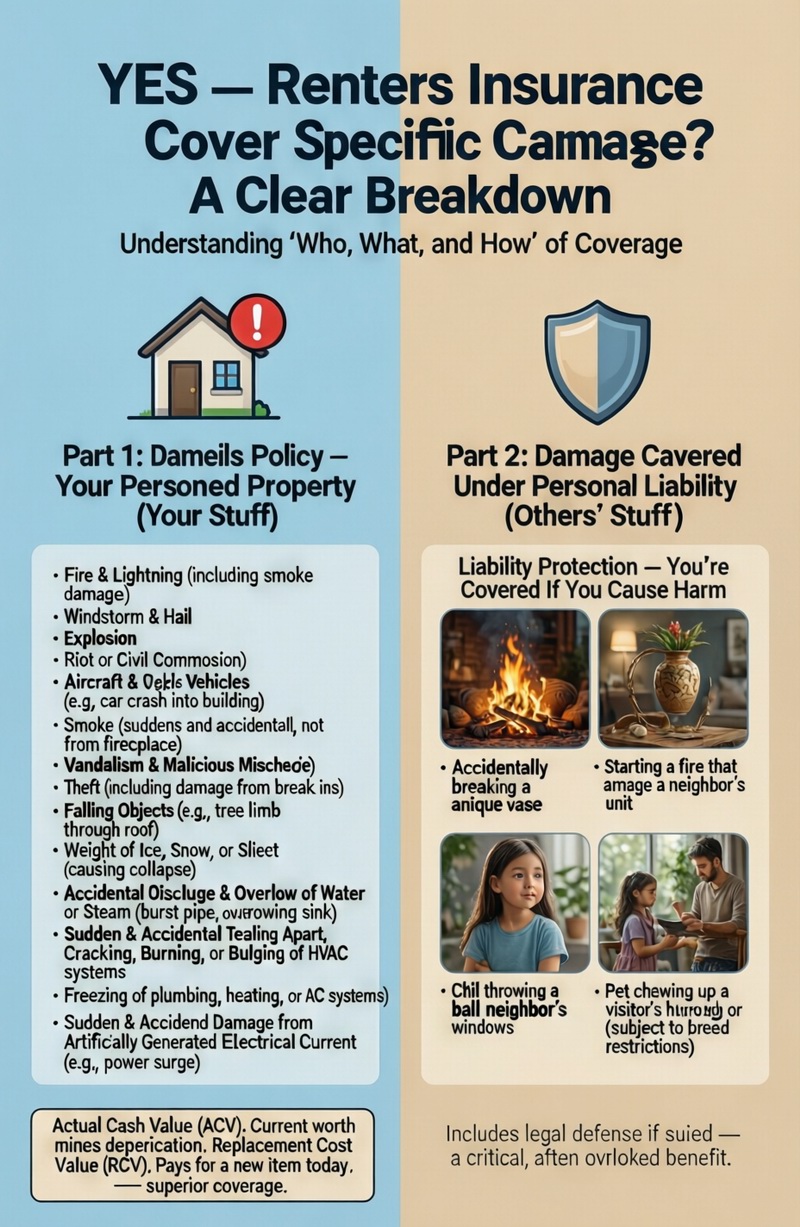

Yes, renters insurance does cover damage, but it’s crucial to understand the “who, what, and how.” It covers two main types: 1) Damage to Your Personal Belongings caused by specific “named perils” like fire, theft, vandalism, windstorms, and certain water damage (e.g., from a burst pipe). 2) Damage You Cause to Others’ Property under your liability coverage, like accidentally breaking a neighbor’s expensive window. However, it does NOT cover damage to the physical structure of your rental apartment (that’s your landlord’s responsibility) or damage from certain excluded causes like floods, earthquakes, and routine wear and tear. The key is the cause of the damage. For a foundational overview, start with our article on what renters insurance is.

Part 1: Damage to Your Personal Property (Your Stuff)

When asking “does renters insurance cover damage” to the items you own, the answer depends entirely on the cause (or “peril”). Standard renters insurance (HO-4 policy) is a “named perils” policy. This means it only covers damage from the causes specifically listed in your policy document. If the cause isn’t on the list, the damage isn’t covered.

Common Covered Perils for Personal Property

Your belongings are typically covered for damage resulting from:

– Fire & Lightning: Including smoke damage from a fire.

– Windstorm & Hail: Damage from a severe storm, like a broken window leading to rain damage inside.

– Explosion

– Riot or Civil Commotion

– Aircraft & Vehicles: If a car crashes into your building and damages your things.

– Smoke: Sudden and accidental damage from smoke (not from a fireplace).

– Vandalism & Malicious Mischief

– Theft: Includes damage caused during a break-in (e.g., a broken door or window).

– Falling Objects: A tree limb crashes through the roof onto your TV.

– Weight of Ice, Snow, or Sleet: Collapse damage.

– Accidental Discharge or Overflow of Water or Steam: A bursting washing machine hose, overflowing sink, or burst pipe. This is a critical coverage for renters.

– Sudden & Accidental Tearing Apart, Cracking, Burning, or Bulging of a steam, heating, or AC system.

– Freezing of plumbing, heating, or AC systems.

– Sudden & Accidental Damage from Artificially Generated Electrical Current: Power surges (but often not for electronics unless specifically covered).

This list forms the core of your renters insurance coverage for belongings.

Understanding Valuation: ACV vs. RCV

Even if damage is covered, how much you get paid depends on your policy’s valuation clause. Actual Cash Value (ACV) pays the item’s current worth minus depreciation. Replacement Cost Value (RCV) pays the cost to buy a new, comparable item today. RCV is far superior and worth the slightly higher premium.

Part 2: Damage Covered Under Personal Liability (Others’ Stuff)

The liability portion of your renters insurance answers “does renters insurance cover damage” that you cause. If you are found legally responsible (“liable”) for damaging someone else’s property, Coverage E (Personal Liability) pays for the repairs or replacement, up to your policy limit.

Common Liability Scenarios for Damage

– Accidental Damage in Your Home: You accidentally knock over and shatter a friend’s expensive antique vase.

– Damage to a Neighbor’s Property: A fire you accidentally start spreads and damages the adjacent unit. Your liability covers their property damage, while your personal property coverage covers your own stuff.

– Damage Away From Home: Your child accidentally throws a baseball through a neighbor’s window while playing in the park.

– Pet Damage: Your dog chews up a visitor’s designer handbag or damages a neighbor’s furniture. (Note: Breed restrictions may apply).

Liability coverage also provides a legal defense if you are sued over the damage. This is a critical, often overlooked protection.

What Damage Is NOT Covered? Critical Exclusions

Understanding exclusions is just as important as knowing what’s covered. The following table clarifies common damage scenarios and whether they are typically covered, helping you answer “does renters insurance cover damage” in tricky situations.

| Type of Damage / Cause | Typically Covered? | Explanation & Alternative |

|---|---|---|

| Damage from a burst pipe in your wall | YES (Personal Property) | Falls under “accidental discharge of water.” Covers your damaged furniture, electronics, etc. Landlord fixes the pipe and building. |

| Flood damage from heavy rain or river overflow | NO | Standard policies exclude “flood.” Requires separate flood insurance (NFIP). |

| Earthquake damage | NO | Excluded. Requires a separate earthquake endorsement or policy. |

| Normal wear and tear | NO | Insurance is for sudden, accidental losses, not deterioration (e.g., a worn-out sofa). |

| Bed bug or pest infestation damage | NO | Considered a maintenance issue. Excluded. |

| Mold damage from long-term humidity | NO | Excluded as “gradual damage.” Mold resulting from a covered water loss (like a sudden pipe burst) may be covered for remediation. |

| Damage from sewer or drain backup | NO (unless endorsed) | Often excluded. Can be added via a “Water Backup of Sewers and Drains” endorsement. |

| Damage you intentionally cause | NO | Intentional acts are excluded from both property and liability coverage. |

| Damage to the rental building itself | NO (for your policy) | This is the landlord’s responsibility, covered by their property insurance. Your liability may cover it if you are at fault. |

| Car damage (to your own vehicle) | NO | Covered by your auto insurance policy, not renters insurance. |

The Landlord’s Property vs. Your Property

This is a fundamental distinction. Your renters insurance covers items that are not permanently attached: your furniture, clothes, electronics. It does not cover damage to permanently installed items like carpeting, light fixtures, appliances provided by the landlord, or the walls themselves. If you cause damage to the landlord’s property (e.g., put a hole in the wall), your liability coverage may pay for the repairs.

Navigating Water Damage: A Special Category

Water damage is a major area of confusion. Renters insurance does cover damage from water that originates inside your unit from a sudden, accidental event (burst pipe, overflowing toilet, leaking appliance). It does not cover water that comes from outside (flooding, groundwater seepage, sewer backup unless endorsed). Knowing the source is key to a successful claim.

The Claims Process for Covered Damage

If you experience covered damage, take these steps:

1. Mitigate Further Damage: Take reasonable steps to prevent more loss (e.g., put a bucket under a leak, board up a broken window).

2. Document Everything: Take photos and videos of the damage before cleaning up.

3. Report to Authorities/Landlord: For theft or vandalism, file a police report. For major damage (fire, pipe burst), notify your landlord immediately.

4. Contact Your Insurance Company: File a claim promptly. Provide your policy number, details, and documentation.

5. Create an Inventory: List all damaged items with descriptions and estimated values. A pre-existing home inventory is invaluable.

6. Cooperate with the Adjuster: They will investigate the cause and assess the damage to determine the payout.

How Your Deductible Works

Your deductible is the amount you pay out-of-pocket on each claim before insurance kicks in. If you have $2,000 in covered damage and a $500 deductible, you receive $1,500 from the insurer. For small damages close to your deductible, it may not be worth filing a claim, as it could raise your future premiums.

Conclusion: A Powerful but Specific Safety Net

So, does renters insurance cover damage? Yes, it provides a powerful financial safety net for a wide array of sudden, accidental damage to your belongings and for damage you accidentally cause to others. Its strength lies in its specificity—it clearly defines what is and isn’t covered. By understanding the named perils, the critical exclusions (especially flood and earthquake), and the difference between your property and the building, you can set accurate expectations and avoid unpleasant surprises. Ensure you have adequate limits and Replacement Cost coverage to make the most of this essential protection. For help determining the right amount, see our guide on renters insurance cost and limits, and explore all renters insurance options to find the best policy for your needs.

Frequently Asked Questions (FAQ)

Does renters insurance cover water damage from a leaking roof?

It depends on how the roof leaked. If a windstorm during a hurricane tears off shingles, allowing rain to enter suddenly, the resulting water damage to your belongings is likely covered (wind is a named peril). If the roof has a slow, long-term leak the landlord failed to fix, the water damage to your items is likely excluded as it’s considered a maintenance issue. The landlord would be responsible.

If my neighbor’s negligence damages my belongings, am I covered?

Yes, under your own policy first. Your renters insurance covers your belongings regardless of who is at fault. You would file a claim with your insurer, who would pay you (minus your deductible). Your insurer may then pursue your neighbor or their insurance company to recover the money paid out (a process called subrogation).

Does renters insurance cover damage from a power surge?

Maybe. Standard policies cover “sudden and accidental damage from artificially generated electrical current,” but this often excludes damage to the electrical item itself (like a fried computer or TV). Some insurers exclude all electronic damage from power surges unless you have specific equipment breakdown coverage or a special endorsement. Check your policy wording.

Are my belongings covered if they’re damaged in my car?

Yes. Your renters insurance provides “off-premises” coverage, typically 10% of your total personal property limit. If your laptop is stolen from your car or damaged by a covered event (like a fire) while in your car, it’s covered under your renters policy. Damage to the car itself is covered by your auto insurance.

Does renters insurance cover accidental damage I cause to my own property?

Generally, no. Renters insurance is for sudden, accidental losses from external perils (fire, theft, burst pipe). It does not cover damage from your own clumsiness or mistakes, like spilling red wine on your own carpet or dropping your smartphone. Some policies may offer limited “breakage” coverage for specific scheduled items like fine art.

What if the damage is caused by my pet to my own things?

No. Damage your pet causes to your own belongings (chewed furniture, scratched floors, ruined shoes) is not covered by renters insurance. This is considered a maintenance or responsibility issue. Liability coverage only applies if your pet damages someone else’s property or injures someone.

Where can I find official policy language examples?

For a clear, authoritative explanation of standard insurance policy forms and coverages, the Insurance Information Institute’s guide to renters insurance breaks down the HO-4 form and common provisions, helping you understand the official language behind what damage is covered.