For individuals who both drive a car and rent their home, managing insurance efficiently is a smart financial move. The term “auto renters insurance” typically refers to the powerful strategy of bundling your auto insurance and renters insurance policies with the same provider. This approach is not a single, combined policy, but rather purchasing both lines of coverage from one insurer to unlock significant discounts and streamline management. Bundling auto and renters insurance is one of the most effective ways for renters to secure comprehensive protection while saving money. This guide will explain exactly how bundling works, detail the substantial financial benefits, explore the coverage advantages beyond just price, and provide a step-by-step plan for finding the best auto renters insurance bundle for your unique needs and budget.

Understanding the Auto Renters Insurance Bundle

An auto renters insurance bundle means you have two separate policies—one for your vehicle and one for your rental home—from the same insurance company. While they are distinct contracts with different coverages, deductibles, and limits, holding them together under one insurer’s umbrella qualifies you for a “multi-policy” or “bundling” discount. This discount is applied to the premium of both policies, leading to a lower total insurance cost than if you purchased each policy from different companies. The concept leverages the insurer’s desire to retain more of your business and reduce their customer acquisition costs. Beyond savings, bundling simplifies your financial life: you have a single point of contact for questions, one renewal date to remember (often they can be aligned), and one convenient payment, typically made through a unified online portal or mobile app.

How Bundling Works: Two Policies, One Insurer

The mechanics of an auto renters insurance bundle are straightforward. You begin by obtaining a quote from an insurer that offers both auto and renters insurance. You will provide information for both your vehicle (make, model, driving history) and your rental property (location, desired coverage limits). The insurer will then generate a combined quote that shows the individual cost of each policy with the multi-policy discount applied. It is important to review each policy’s details separately to ensure both provide the coverage you need. The renters policy covers your personal property, liability, and additional living expenses. The auto policy covers liability for bodily injury and property damage you cause, collision, comprehensive damage to your own car, and other standard protections. Together, they form a comprehensive safety net for your major assets and risks. For a clear understanding of the renters component, explore what renters insurance is and its core protections.

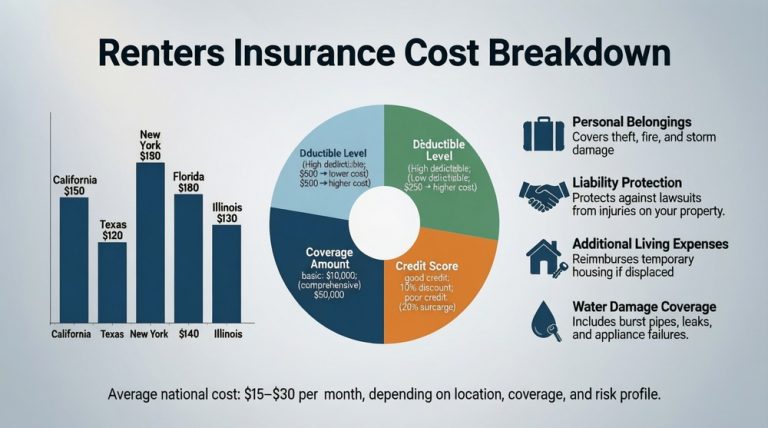

The Financial Benefits: How Much Can You Save?

The primary incentive for bundling auto renters insurance is the substantial discount. On average, customers save between 10% and 25% on their total premium when they bundle two or more policies. In dollar terms, if your auto insurance costs $1,200 per year and your renters insurance costs $200 per year, a 20% bundle discount would save you $280 annually ($1,400 total premium x 20%). This makes the already affordable renters insurance even more cost-effective, often reducing its net cost to just over $100 per year. The exact discount percentage varies by company, your location, driving record, and other risk factors, but it is almost universally offered by major insurers like State Farm, Allstate, GEICO, and Progressive. This saving is the most compelling answer to why bundling auto renters insurance is a financially savvy decision for nearly every renting driver.

Coverage and Convenience Advantages of Bundling

While savings are the headline, the benefits of an auto renters insurance bundle extend beyond the price tag. A major advantage is simplified management. With both policies under one roof, you have a single insurance agent or customer service team to contact for changes, questions, or claims. This can be invaluable during stressful situations like a car accident that also involves property you had in the vehicle. Furthermore, bundling can sometimes provide enhanced coverage options or more favorable terms. Some insurers offer features like a single deductible for a loss that affects both your car and your home contents (though this is rare), or they may be more flexible with payment plans. The convenience of a unified digital experience—managing both policies, making payments, and storing ID cards in one app—cannot be overstated. It reduces administrative hassle and minimizes the risk of a coverage lapse due to missed separate payments.

Enhanced Service and Claims Handling

Being a multi-policy customer often elevates your status with an insurer. You may receive priority service or have access to dedicated support lines. In the event of a claim that overlaps both policies—for example, if items are stolen from your car—you only need to navigate one company’s claims process. While you would still file separate claims under each policy, working with the same claims adjuster or team can streamline communication and documentation. Your established relationship as a bundled customer can also foster better service. It is important, however, to ensure that the quality of each individual policy’s renters insurance coverage and auto coverage meets your standards. The best bundle is one where both policies are robust and the insurer has a strong reputation for fair claims settlement in both product lines.

Potential Drawbacks and Considerations

Despite the clear advantages, a blind commitment to bundling auto renters insurance is not always the best move. The primary consideration is that the bundled discount must outweigh any potential premium savings you could get by shopping each policy separately with different insurers. Sometimes, one company may have exceptionally competitive auto rates but mediocre renters rates, or vice-versa. You should always get individual quotes from at least three insurers for both auto and renters insurance, and then ask each for their bundled price. This comparison ensures you are getting the best overall value, not just a discount on potentially higher base rates. Additionally, if you have a poor driving record or claims history, it might affect the pricing of your entire bundle, so exploring separate insurers for each policy could be beneficial. For context on standalone renters pricing, see our guide on renters insurance cost.

How to Find and Secure the Best Auto Renters Insurance Bundle

Securing the optimal auto renters insurance bundle requires a methodical shopping approach. Start by gathering all necessary information: your auto insurance declarations page, your driver’s license number, vehicle VIN, and details about your rental home and an estimated value of your belongings. Next, research insurers known for competitive bundling. Major national carriers (State Farm, Allstate, Progressive, GEICO, Liberty Mutual) are strong candidates, but also check large regional providers and those you may have access to through employers or membership organizations (like USAA or AAA). Obtain quotes in two ways: first, get individual quotes for auto and renters from each company, and second, ask for a bundled quote. Use comparison websites and independent agencies, like Tejribati, to view multiple options. When comparing, ensure the coverage limits and deductibles are identical across all quotes for a true apples-to-apples comparison.

Key Questions to Ask When Getting Bundled Quotes

When speaking with agents or using online quote tools, ask specific questions to unlock the best auto renters insurance bundle. First, ask, “What is the exact multi-policy discount percentage for bundling these two policies?” Second, inquire if there are any other discounts you qualify for, such as safe driver, defensive driving course, good student, automatic payment, paperless billing, or protective device discounts for your rental home. Third, ask if the policies can be set to renew on the same date for easier management. Fourth, clarify the claims process: will you have a single point of contact? Finally, verify the financial strength of the insurer by checking ratings from independent agencies like AM Best. For comprehensive, unbiased information on insurance principles, the Insurance Information Institute is an excellent resource.

When It Might Make Sense Not to Bundle

While bundling is advantageous for most, there are scenarios where separating your auto renters insurance might be wiser. If you have a specialty auto insurance need (like coverage for a classic car or a high-risk driving record) that is best served by a niche provider, you may get a better auto rate separately. Similarly, if you find an exceptional renters insurance rate through a digital-only insurer that doesn’t offer auto insurance, the combined cost of two separate, best-in-class policies could be lower than a mediocre bundle. The decision always comes down to the math: total the cost of the best separate quotes you can find and compare it to the best bundled quote. Only if the bundled price is lower for equivalent or better coverage should you proceed. Never sacrifice necessary coverage quality just to secure a bundle discount.

Maximizing Your Protection and Savings Long-Term

After securing your auto renters insurance bundle, your work is not done. To maximize value, conduct an annual insurance review. Before each renewal, reassess your coverage needs—have you bought a new car, acquired expensive jewelry, or moved to a new rental? Contact your insurer to update your policies and ensure you’re not over- or under-insured. Also, re-shop your bundle every 2-3 years. The insurance market is dynamic, and loyalty discounts are sometimes less valuable than new customer promotions offered by competitors. By periodically comparing prices, you ensure you continue to receive the best combination of price and service for your auto renters insurance needs. This proactive approach guarantees that the convenience of bundling continues to be matched by ongoing financial savings and optimal protection.

Frequently Asked Questions (FAQ)

Is auto renters insurance a single policy?

No, it is not a single policy. “Auto renters insurance” refers to the practice of purchasing two separate policies—one for your car and one for your rental home—from the same insurance company to qualify for a multi-policy discount.

How much is the typical discount for bundling?

The typical discount for bundling auto and renters insurance ranges from 10% to 25% off the total combined premium. The exact amount varies by insurance company, your location, driving history, and other personal factors.

Can I bundle if I have a poor driving record?

Yes, you can still bundle, but your auto insurance premium will likely be high due to your record. The multi-policy discount will still apply to that higher premium, but it may be worthwhile to shop separately to see if a specialty auto insurer offers a better rate alone.

Do all insurance companies offer bundling discounts?

Virtually all major insurers that sell both auto and renters insurance offer a bundling discount. However, some digital-only renters insurance companies may not sell auto insurance, so bundling with them is not an option.

What happens to my bundle if I sell my car or buy a home?

If you sell your car and no longer need auto insurance, you would cancel that policy and your renters insurance would revert to its standard, un-bundled rate. If you buy a home, you would typically replace your renters policy with a homeowners policy and can often bundle that with your auto insurance for a similar discount.

Is it easier to file a claim with a bundled policy?

It can be more convenient, as you have one company to deal with. However, you will still file separate claims under each policy’s terms. The main ease comes from having a familiar point of contact and a single online portal to manage both claims processes.

Should I always bundle my auto and renters insurance?

Not always. You should compare the total cost of a bundled quote with the total cost of purchasing the best auto and renters policies from two different companies. Only bundle if the combined bundled price is lower for equivalent or better coverage.