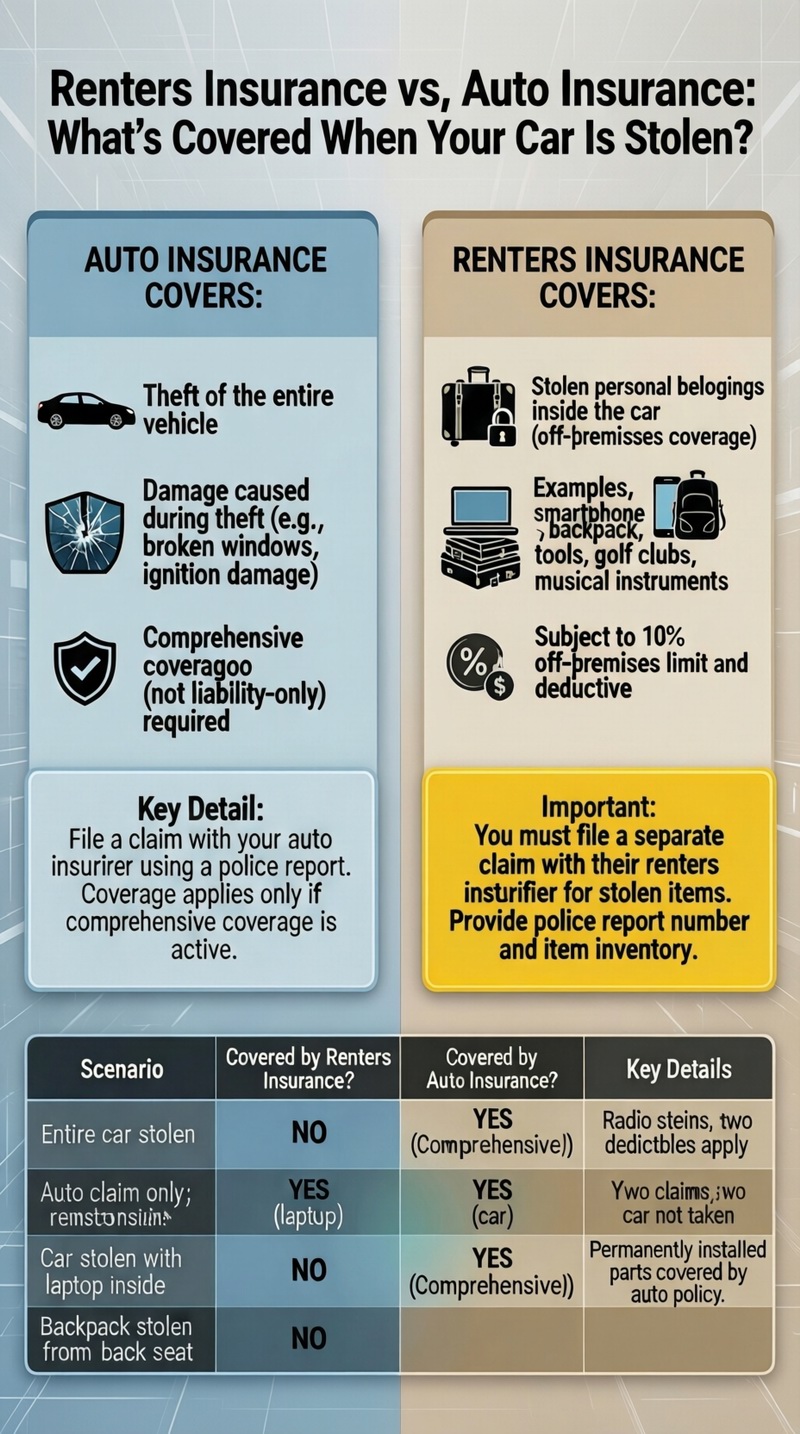

Renters insurance does NOT cover the theft of your car itself. However, it does cover your personal belongings that were inside the car when it was stolen, such as a laptop, gym bag, or tools. The vehicle is covered exclusively by your auto insurance policy’s comprehensive coverage. If your car is stolen, you file a claim with your auto insurer. If items inside the car were also stolen, you file a separate claim with your renters insurer, subject to its “off-premises” coverage limit and your deductible. You will need a police report for both claims. For the basics, see our guide on what renters insurance is.

The Clear Division: Car vs. Contents

When asking “does renters insurance cover car theft?” you must separate two distinct properties: 1) The automobile, which is a motor vehicle designed for road use, and 2) Your personal property, which is the movable items you own and transport. Insurance policies are designed around this division. Auto insurance covers vehicles and their permanent parts; renters insurance covers your personal belongings anywhere in the world. This is a fundamental principle of renters insurance coverage.

What Renters Insurance Covers: Your Stolen Belongings

Your renters policy’s “off-premises” coverage protects your personal property against theft, even when it’s away from your home. If your car is stolen with your belongings inside, those items are covered. Common examples include:

– Electronics: Laptops, tablets, smartphones, GPS units.

– Personal Items: Purses, backpacks, luggage, clothing, sports equipment.

– Tools: Non-permanent tools (a toolbox, not tools built into a work van).

– Other: Musical instruments, textbooks, camping gear.

Coverage is subject to your policy’s off-premises limit (typically 10% of your total personal property limit) and your deductible.

What Auto Insurance Covers: The Stolen Vehicle

Your auto insurance policy’s comprehensive coverage (sometimes called “other than collision”) is specifically for this loss. It covers theft of the entire vehicle, as well as damage caused during the theft (e.g., broken windows, damaged ignition). If you only have liability auto insurance, you have no coverage for the stolen car itself. Comprehensive coverage is optional but essential.

Coverage Scenarios: A Detailed Breakdown

The following table clarifies exactly what is covered by which policy in various car theft situations, answering “does renters insurance cover car theft?” in practical terms.

| Scenario | Covered by Renters Insurance? | Covered by Auto Insurance? | Key Details |

|---|---|---|---|

| Your entire car is stolen. | NO | YES (Comprehensive) | Auto insurance handles the vehicle loss. Renters insurance does not apply to the car itself. |

| Car is stolen with your laptop inside. | YES (for laptop) | YES (for car) | Two separate claims: Auto for the car, Renters for the laptop. Two deductibles apply. |

| Thieves break in, steal your radio, but don’t take the car. | NO | YES (Comprehensive) | A permanently installed car stereo is part of the vehicle, covered by auto insurance. |

| Thieves steal your backpack from the back seat. | YES | NO | This is a theft of personal property, covered by renters insurance (subject to off-premises limit). |

| Car is recovered, but your golf clubs inside are gone. | YES (for clubs) | YES (for car damage) | File a renters claim for the stolen clubs. File an auto claim for any damage to the car from the theft. |

The 10% Off-Premises Limit

Renters insurance limits coverage for belongings away from your home. Usually, this is 10% of your total personal property limit. If you have $30,000 in coverage, you have $3,000 for items stolen from your car. Ensure this limit is adequate for the value of items you regularly transport.

The Claims Process for a Stolen Car and Belongings

Act quickly and methodically to handle both potential claims.

1. Contact the Police Immediately: File a stolen vehicle report. Get the police report number. This is required for both auto and renters insurance claims.

2. Notify Your Auto Insurance Company: Report the stolen vehicle to your auto insurer to start the comprehensive claim process. They will likely start an investigation and have a waiting period (often 30 days) before declaring the car a total loss.

3. Document Your Losses: Create a list of all personal items that were in the car. Include descriptions, brands, models, serial numbers if available, and estimated replacement costs. Use old photos or receipts if possible.

4. Contact Your Renters Insurance Company: If you had valuable items in the car, file a separate claim for those belongings. Provide the police report number and your inventory list.

5. Work with Both Adjusters: You may have two different adjusters. Be clear: the auto claim is for the vehicle, the renters claim is for the contents.

6. Pay Your Deductibles: You will likely pay two deductibles: your auto comprehensive deductible and your renters insurance deductible. Consider this before filing a renters claim for low-value items.

Actual Cash Value vs. Replacement Cost for Stolen Items

If your renters policy has Actual Cash Value (ACV), you’ll get the depreciated value of your stolen 3-year-old camera. With Replacement Cost Value (RCV), you’ll get enough to buy a new, comparable camera. RCV coverage is highly recommended.

Preventing Theft and Ensuring Adequate Coverage

Prevention is key. Never leave valuables in plain sight. Use a steering wheel lock or car alarm. Park in well-lit, secure areas.

To ensure proper insurance coverage:

– Carry Comprehensive Auto Coverage: Don’t opt for liability-only insurance. The cost is relatively low for the protection it provides.

– Review Your Renters Off-Premises Limit: Ensure 10% of your personal property limit covers the value of items you often carry. Increase your overall limit if needed.

– Schedule High-Value Items: For expensive cameras, musical instruments, or professional equipment you transport, “schedule” them on your renters policy for full, stated-value coverage.

– Maintain an Inventory: Keep a photo/video log of high-value items and their serial numbers stored in the cloud.

Understanding these elements helps manage your total renters insurance cost and protection. For a full review, explore all renters insurance options.

Conclusion: Two Policies, Two Protections

In summary, does renters insurance cover car theft? It covers the aftermath—the loss of your personal possessions inside the vehicle—while your auto insurance covers the vehicle itself. This division of responsibility is clear in the insurance world. Being a victim of auto theft is stressful enough; don’t compound it by being underinsured. Ensure you have both robust auto comprehensive coverage and sufficient renters insurance limits with Replacement Cost to recover what’s lost. Always file a police report immediately, as it is the foundation for both claims.

Frequently Asked Questions (FAQ)

What if I only have liability auto insurance and my car is stolen?

If you only carry liability insurance, you have no coverage for the stolen vehicle. Liability insurance only covers damage or injuries you cause to others. You would be responsible for the entire financial loss of the car. This is why comprehensive coverage is crucial.

Are items stolen from a rental car covered by my renters insurance?

Yes. Your renters insurance off-premises coverage extends to your personal property anywhere in the world, including inside a rental car. The same limits and rules apply. The rental car company’s insurance covers the vehicle.

Does renters insurance cover a stolen car key or key fob?

Maybe, but it’s complicated. The key fob itself is personal property, so its theft might be covered. However, the much larger cost is often re-keying the car to prevent theft. This is typically considered part of the auto loss and should be covered by your auto comprehensive claim, not your renters policy.

What if my car is stolen from my apartment’s parking lot?

The location doesn’t change the coverage. Whether stolen from your driveway, a parking lot, or a shopping mall, the same rules apply: Auto insurance covers the car, renters insurance covers the belongings inside (if applicable).

Will filing a renters claim for stolen items raise my premium?

It might. Filing any claim can lead to a premium increase at renewal. For a small loss close to your deductible, it may be more cost-effective to pay out-of-pocket than to risk a rate hike over several years.

How long does the auto insurance company take to pay for a stolen car?

Most policies have a waiting period (often 30 days) to see if the car is recovered. If not recovered after that period, the insurer will typically declare it a total loss and pay you the vehicle’s Actual Cash Value (ACV), minus your deductible, based on its pre-theft market value.

Where can I learn more about auto theft and insurance?

The Insurance Information Institute’s guide to auto insurance coverage provides a clear breakdown of comprehensive coverage and other auto policy parts, which is essential context when dealing with car theft.