Yes, renters insurance typically does cover car break-ins—but only for your personal belongings stolen from the vehicle, not for damage to the car itself. If thieves smash your window and steal your laptop, backpack, or sports equipment, those items are covered under your renters insurance policy’s “off-premises” personal property coverage. However, there are important limits: coverage is usually capped at 10% of your total personal property limit (e.g., $3,000 if you have $30,000 total coverage). The theft must also be a confirmed crime (a police report is required). Damage to the car (broken window, slashed seats) is covered by your auto insurance comprehensive coverage, not renters insurance. For the basics, see our guide on what renters insurance is.

How Renters Insurance Covers Belongings in Your Car

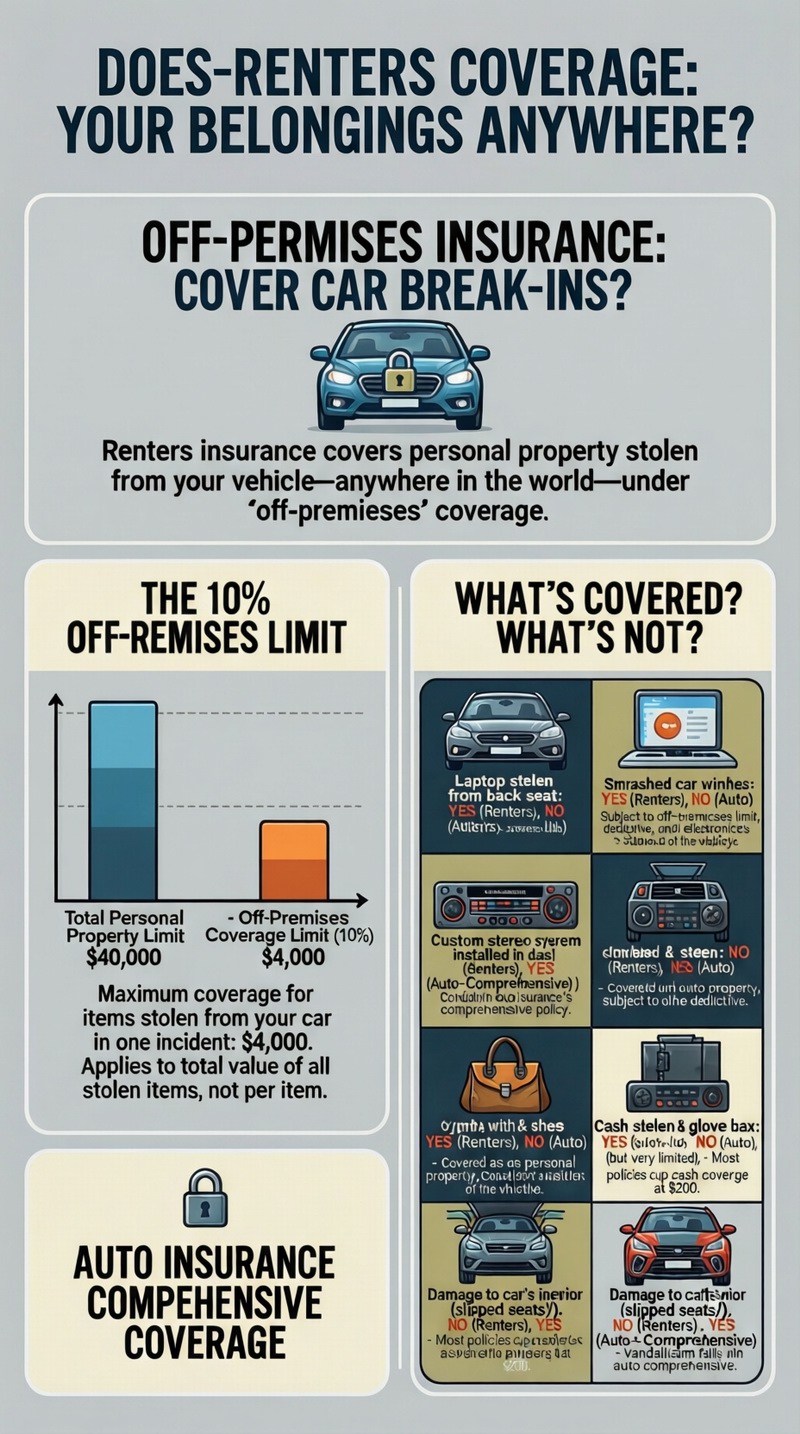

When asking “does renters insurance cover car break-ins?”, you’re tapping into a key feature: off-premises coverage. Your renters insurance protects your personal property anywhere in the world, not just inside your apartment. This includes items stolen from your car, a hotel room, a locker at the gym, or while you’re traveling. Theft is a standard named peril in the policy, so if your items are stolen from a locked or unlocked vehicle, the loss is generally covered, subject to your policy’s terms.

The 10% Off-Premises Limit

This is the most crucial detail. Insurers apply a sub-limit for property away from your primary residence. Typically, this limit is 10% of your total personal property coverage (Coverage C). For example:

– Your Total Personal Property Limit: $40,000

– Off-Premises Coverage Limit (10%): $4,000

– Maximum coverage for items stolen from your car in one incident: $4,000

This limit applies to the total of all items stolen, not per item. If you have $6,000 worth of photography equipment in your car, you would be underinsured by $2,000. This is a key part of your overall renters insurance coverage.

What Items Are Typically Covered?

Common items stolen in car break-ins that are covered by renters insurance include:

– Electronics: Laptops, tablets, smartphones, GPS units, cameras.

– Personal Items: Briefcases, backpacks, purses, clothing, gym bags.

– Sports Equipment: Golf clubs, skis, bicycles (if not attached to the car).

– Miscellaneous: Tools (for personal use), musical instruments, textbooks.

Remember, these are your personal belongings, not parts of the car.

What’s Covered, What’s Not: A Clear Breakdown

The following table clarifies the division of coverage between renters and auto insurance after a car break-in, answering “does renters insurance cover car break-ins?” in specific scenarios.

| What Was Lost/Damaged | Covered by Renters Insurance? | Covered by Auto Insurance? | Key Details |

|---|---|---|---|

| Laptop stolen from back seat | YES | NO | Subject to off-premises limit, deductible, and theft sub-limits for electronics. |

| Smashed car window | NO | YES (Comprehensive) | Damage to the vehicle itself is always an auto insurance claim under comprehensive coverage. |

| Custom stereo system installed in dash | NO | YES (Comprehensive) | Permanently installed electronic equipment is generally considered part of the car. |

| Gym bag with clothes & shoes stolen | YES | NO | Covered as personal property, subject to your deductible. |

| Cash stolen from glove box | YES (but very limited) | NO | Most policies have a very low sub-limit for cash (e.g., $200). |

| Damage to car’s interior (slashed seats) | NO | YES (Comprehensive) | Vandalism damage to the vehicle falls under auto comprehensive. |

The Role of Your Auto Insurance

Your auto insurance policy’s comprehensive coverage (sometimes called “other than collision”) is specifically designed for this. It covers damage to your vehicle from theft, vandalism, fire, and falling objects. When you file a claim for a broken window, you’ll pay your auto comprehensive deductible. It’s essential to have this coverage; liability-only auto insurance will not cover break-in damage.

The Claims Process for a Car Break-In

After discovering a break-in, follow these steps to ensure both your renters and auto insurance claims are handled smoothly.

1. Call the Police Immediately: File an official police report. This is a non-negotiable requirement for both renters (theft) and auto (vandalism) insurance claims. Get the report number.

2. Document the Scene: Take photos of the damaged car (broken windows, forced locks) and the interior, showing where items were taken from. Do not touch evidence.

3. Create a Theft Inventory: List every stolen item, including description, brand, model, serial number (if available), and estimated replacement cost. Having a pre-existing home inventory makes this much easier.

4. Contact Your Auto Insurer: File a claim for the vehicle damage (broken window, etc.). Provide the police report number.

5. Contact Your Renters Insurer: File a separate claim for your stolen personal belongings. Provide the police report, your theft inventory, and any proof of ownership (receipts, photos).

6. Work with Both Adjusters: You may have two different adjusters. Be clear about what each claim is for: auto for car damage, renters for stolen items.

7. Pay Your Deductibles: You will likely pay two separate deductibles: one for auto comprehensive and one for renters insurance. The renters deductible applies to the total value of stolen items.

Actual Cash Value vs. Replacement Cost for Stolen Items

If your renters policy has Actual Cash Value (ACV), you’ll be reimbursed for the depreciated value of your stolen 3-year-old laptop—maybe $300. With Replacement Cost Value (RCV), you’ll get enough to buy a new, comparable laptop—$1,000+. RCV coverage is highly recommended and significantly impacts your financial recovery.

Preventing Break-Ins and Maximizing Your Coverage

Prevention is the best policy. Never leave valuables in plain sight. Store items in the trunk before arriving at your destination. Use a car alarm or steering wheel lock.

To ensure adequate coverage:

– Review Your Off-Premises Limit: Is 10% of your personal property limit enough to cover the items you typically transport? If not, consider increasing your overall limit.

– Schedule High-Value Items: For expensive cameras, musical instruments, or professional tools you carry regularly, consider “scheduling” them on your renters policy. This provides stated-value coverage, often with no deductible, and may not be subject to the off-premises limit.

– Ensure You Have Auto Comprehensive Coverage: Don’t carry liability-only insurance if your car is at risk for break-ins.

Understanding these elements helps manage your overall renters insurance cost and protection. For a full review, explore all renters insurance options.

Conclusion: A Dual-Insurance Solution

So, does renters insurance cover car break-ins? Yes, for the stuff inside the car. It works in tandem with your auto insurance, which covers the car itself. By understanding the 10% off-premises limit, maintaining an inventory, and having both comprehensive auto and renters insurance with RCV, you can recover from this violating event with minimal financial stress. Remember, the police report is your first and most important step. Stay protected by not making your car a target and by ensuring your insurance limits reflect the value of what you carry with you.

Frequently Asked Questions (FAQ)

What if my car was unlocked? Does that affect coverage?

Generally, no. Renters insurance typically covers theft regardless of whether the car was locked. However, if you were grossly negligent (e.g., left the car running with the door open), the insurer might dispute the claim. Always lock your doors, but an unlocked car doesn’t automatically void theft coverage for your belongings.

<3>Are items stolen from a rental car covered?

Yes. Your renters insurance off-premises coverage applies to your belongings anywhere in the world, including in a rental car. The same limits and rules apply. Damage to the rental car would be covered by the rental company’s insurance or the coverage you purchased at the counter.

Does renters insurance cover a stolen car battery or tires?

No. Parts permanently attached to the vehicle are considered part of the car. Theft of a car battery, tires, rims, or catalytic converter is covered by your auto insurance comprehensive coverage, not your renters insurance.

What if I don’t have a police report?

Your claim will likely be denied. A police report is mandatory to prove the theft occurred and to provide an official record for the insurance company. Without it, they have no way to verify the loss wasn’t fraudulent. Always file a report, even for minor thefts.

Will filing a renters insurance claim for a car break-in raise my rate?

It might. Filing any claim, including theft, can lead to a premium increase at renewal because you are now considered a higher risk. For a small loss close to your deductible, it may be more cost-effective to pay out-of-pocket than to risk a rate hike.

What if the stolen items were for my business?

Coverage is limited. Renters insurance has a low sub-limit for “business property” (often $2,500). If you had expensive work tools or inventory stolen, you may be underinsured. A separate business insurance policy or an in-home business endorsement is needed for adequate coverage.

Where can I learn more about auto and property insurance coordination?

For a clear explanation of how different insurance policies interact, the Insurance Information Institute’s article on renters insurance coverage provides a good foundation, and your auto insurer can detail your comprehensive coverage.