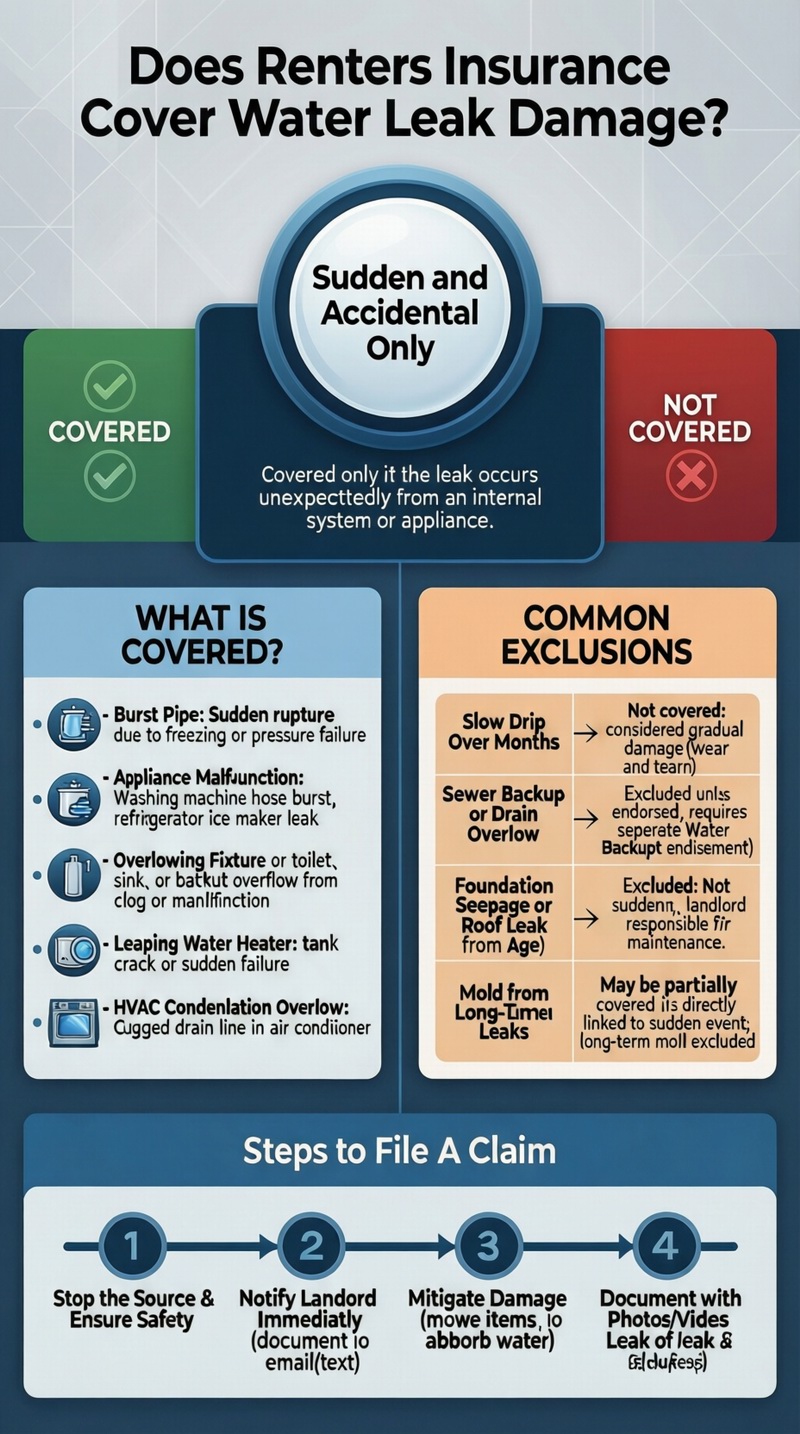

Renters insurance does cover water leak damage, but with a critical condition: the leak must be sudden and accidental. This means a pipe that suddenly bursts, a washing machine hose that ruptures without warning, or an overflowing toilet due to a clog are typically covered events. Your policy will pay to repair or replace your damaged personal belongings (furniture, electronics, clothing) up to your personal property limit. However, gradual damage from a slow, ongoing leak (like a dripping pipe under a sink that goes unnoticed for months) is considered a maintenance issue and is not covered. The key is the speed and unexpected nature of the event. For foundational knowledge, start with our guide on what renters insurance is.

Understanding the “Sudden and Accidental” Standard

When determining does renters insurance cover water leak damage, insurance companies look at the cause. Standard renters insurance policies (HO-4 form) cover water damage caused by the “accidental discharge or overflow of water or steam from within a plumbing, heating, air conditioning, or automatic fire protection sprinkler system, or from within a household appliance.” The keywords are accidental and from within. This language is designed to cover unforeseen internal failures, not external flooding or wear and tear.

Examples of COVERED Water Leak Damage

Your personal property coverage (Coverage C) will respond if your belongings are damaged by:

– A Burst Pipe: A frozen pipe that ruptures, or a pipe that suddenly fails due to a manufacturing defect or excessive pressure.

– Appliance Malfunction: The water supply line to your refrigerator ice maker breaks, flooding the kitchen. A washing machine hose bursts.

– Overflowing Fixture: An overflowing toilet, sink, or bathtub due to an accidental clog or malfunction (not a sewer backup).

– Leaking Water Heater: The tank suddenly cracks and leaks.

– HVAC Issues: An air conditioner’s condensation line clogs and overflows inside the unit.

In all these cases, the water originates suddenly from a built-in system or appliance within your rental. This is a core part of your renters insurance coverage.

The Landlord’s Responsibility vs. Yours

It’s crucial to separate responsibilities. Your landlord’s insurance covers the structure—repairing the broken pipe, damaged drywall, flooring, and cabinetry. Your renters insurance covers your personal property—the sofa, TV, books, and clothing damaged by the water. You are responsible for mitigating further damage (e.g., moving items out of the water).

What Water Leak Damage is NOT Covered? Key Exclusions

The most common and costly misunderstandings arise from leaks that are excluded. The following table clarifies scenarios to answer “does renters insurance cover water leak damage” in complex situations.

| Type of Leak / Cause | Typically Covered? | Explanation & Who is Responsible |

|---|---|---|

| Sudden burst of a supply line under the sink | YES | Sudden, accidental discharge from a plumbing system. Your insurance covers your damaged items; landlord fixes the pipe. |

| Slow drip from a worn-out pipe joint over several months | NO | Considered “gradual damage,” wear and tear, or lack of maintenance. Excluded. Landlord may be liable for not repairing. |

| Water seepage through foundation walls or floors | NO | Considered “groundwater” or flood-related. Excluded. May require separate flood insurance. |

| Backup or overflow from a sewer or drain | NO (unless endorsed) | Typically excluded. Can be added via a “Water Backup of Sewers and Drains” endorsement. |

| Leak from a roof due to wind/hail damage | YES (for your belongings) | If wind (a covered peril) damages the roof, allowing rain in, the resulting water damage to your items is covered. |

| Leak from a roof due to old age/worn shingles | NO | Gradual deterioration. Excluded. Landlord is responsible for roof maintenance and any damage to your belongings may be their liability. |

| Mold resulting from a covered leak | MAYBE (Limited) | If mold is a direct result of the covered water leak, some policies may cover remediation of affected belongings. Mold from a long-term leak is excluded. |

The Critical “Gradual Damage” Exclusion

Insurance is designed for sudden, unforeseen losses—not problems that develop over time due to neglect or poor maintenance. If you notice a small leak and ignore it, and it later causes major damage, your claim will likely be denied. You have a “duty to protect your property.” Report any signs of moisture or leaks to your landlord immediately, in writing, to protect yourself.

Navigating a Water Leak Damage Claim: Step-by-Step

If you experience a sudden leak, taking the right steps protects your belongings and your claim.

1. Stop the Source & Ensure Safety: If safe, turn off the water supply to the leaking fixture or the main water shut-off. Avoid electrical hazards.

2. Notify Your Landlord Immediately: They are responsible for stopping the leak and repairing the source. Document your notification (email/text is best).

3. Mitigate Further Damage: Move undamaged items to a dry area. Use towels to soak up standing water. This is required by your policy.

4. Document Everything Extensively: Take clear photos and videos of the leak source, the damaged areas, and all affected belongings before you start cleaning up.

5. Create a Detailed Inventory: List every damaged item with description, age, and estimated replacement cost. A pre-existing home inventory is invaluable.

6. Contact Your Renters Insurance Company: File the claim promptly. Provide your policy number, documentation, and a clear description of the cause.

7. Work with the Adjuster: They will investigate to determine if the cause is a covered peril (sudden vs. gradual) and assess the damage.

8. Secure Temporary Housing if Needed: If the leak makes your unit uninhabitable, your Additional Living Expenses (ALE) coverage pays for a hotel and extra costs. Keep receipts.

Actual Cash Value vs. Replacement Cost

Water can destroy items. With Actual Cash Value (ACV), you get the depreciated value of your waterlogged 4-year-old laptop—maybe $200. With Replacement Cost Value (RCV), you get enough to buy a new, comparable laptop—$800+. Always choose RCV coverage.

Prevention, Endorsements, and Proactive Protection

The best claim is the one you never file. Prevent leaks by:

– Knowing the location of your unit’s water shut-off valve.

– Inspecting appliance hoses regularly and replacing them every 5-7 years.

– Reporting any signs of moisture (stains, warping, musty smells) to your landlord immediately in writing.

Consider these policy enhancements:

– Water Backup Endorsement: Adds coverage for sewer/drain backups, a common source of water damage.

– Equipment Breakdown Coverage: May cover the sudden mechanical failure of an appliance that causes a leak.

Review your policy’s details and understand your renters insurance cost relative to the protections you have. For a comprehensive review, explore all renters insurance options.

Conclusion: Speed and Source Determine Coverage

In summary, does renters insurance cover water leak damage? Yes, for the sudden, internal accidents that are common in homes. But no, for the slow, creeping damage that results from deferred maintenance. Your financial protection hinges on the cause being sudden and accidental. By understanding this distinction, taking swift action when a leak occurs, maintaining good communication with your landlord, and choosing Replacement Cost coverage, you can navigate water leak incidents with confidence. Remember, prompt reporting and documentation are your best tools for a successful outcome.

Frequently Asked Questions (FAQ)

What if the leak comes from the apartment above or next door?

You are still covered under your own renters insurance policy for damage to your belongings, regardless of where the water originated. If the leak from a neighbor’s unit is due to a covered peril (like a burst pipe), your insurer will pay you. They may then seek reimbursement from the neighbor’s insurance (subrogation). Your claim process remains the same.

Does renters insurance cover the cost to tear out walls to find the leak?

No. Renters insurance covers your personal property, not the structure. The cost of investigating and repairing the building itself (including opening walls) is the landlord’s responsibility. Your coverage is for your belongings damaged by the water that escaped.

How can I prove a leak was “sudden” and not “gradual”?

Documentation is key. If you have prior photos of the area showing no damage, that helps. The adjuster will look for signs: A sudden burst often has a single point of origin and may show spraying. Gradual leaks often show widespread water staining, mold, or rot. Your prompt reporting (date-stamped communication to your landlord) also supports a “sudden” discovery.

Are my belongings covered if they’re damaged by the plumber fixing the leak?

If a plumber hired by your landlord accidentally causes additional damage (e.g., breaks your shelf while working), that damage may be covered under your policy’s personal property coverage, as it’s a sudden, accidental event. However, the plumber or their insurance should be primarily liable. Notify your insurer, and they will coordinate.

Does renters insurance cover water leaks if I’m away on vacation?

Yes, if the leak is from a covered peril. However, if you turned off the heat in winter, causing pipes to freeze and burst, the claim could be denied due to negligence. You have a duty to maintain heat or properly winterize. Always take precautions before an extended absence.

What if the landlord’s negligence caused the leak?

Your renters insurance still covers your belongings first. If you can prove the landlord was negligent (e.g., ignored repeated requests to fix a known issue), your insurer may pay you and then pursue the landlord or their insurance to recover the money. You may also be able to seek reimbursement directly from the landlord for your deductible.

Where can I find more information on property damage claims?

For a clear, authoritative overview of how property insurance handles water damage, the Insurance Information Institute’s guide on water damage provides excellent general advice that applies to renters situations as well.