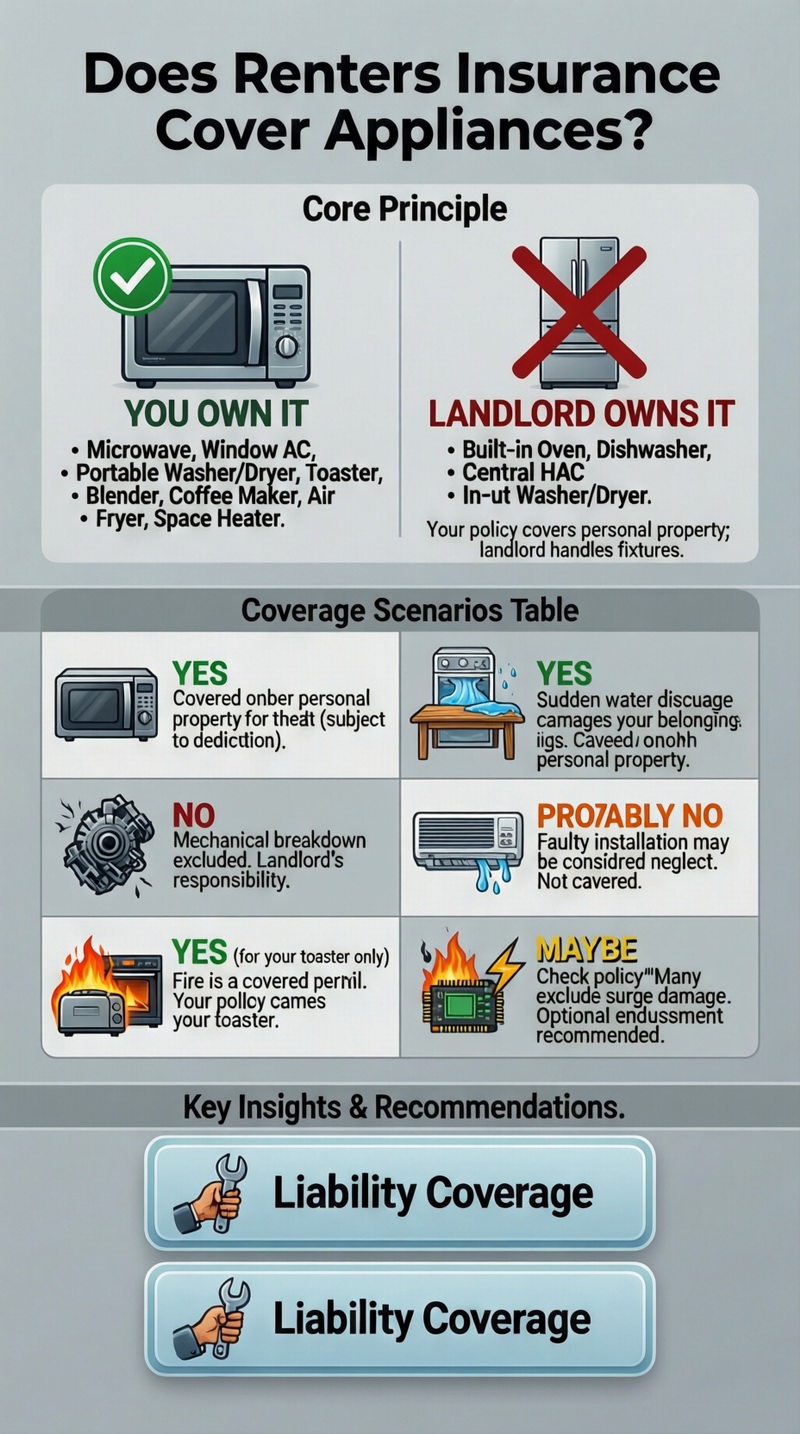

The answer to “does renters insurance cover appliances?” depends entirely on who owns the appliance and what caused the damage. Your renters insurance does cover damage to your personal, portable appliances (like a microwave or window AC unit you own) if they are damaged by a covered peril such as fire, theft, or a sudden plumbing leak. It does not cover mechanical breakdown, wear and tear, or repairs to landlord-provided, built-in appliances (like the refrigerator or oven that came with the unit). Those are the landlord’s responsibility to maintain and repair. However, damage those landlord appliances cause to your belongings (e.g., a leaking dishwasher ruining your flooring) is covered. For specialized breakdown coverage, you may need an optional endorsement. Start with the basics in our guide on what renters insurance is.

The Core Principle: Tenant-Owned vs. Landlord-Owned Appliances

This is the most important distinction when determining does renters insurance cover appliances. Your policy’s personal property coverage (Coverage C) protects belongings that you own and would take with you when you move. Landlord-provided appliances are considered part of the building’s fixtures and are covered by their property insurance, not yours.

Appliances YOU Own (Typically Covered)

If you purchased it and can unplug it and take it, it’s likely your personal property. Examples include:

– Microwave oven

– Window air conditioning unit

– Portable dishwasher or clothes washer/dryer

– Toaster, blender, coffee maker, air fryer

– Space heater, dehumidifier

These items are covered if they are damaged or destroyed by a covered peril listed in your policy, such as fire, lightning, windstorm, theft, vandalism, or sudden water discharge (like a burst pipe that soaks your microwave). This coverage is part of your standard renters insurance coverage.

Appliances Your LANDLORD Owns (Not Covered for Repair)

Appliances that are permanently installed or provided as part of the rental are the landlord’s property. You are not responsible for insuring them against breakdown. Examples:

– Built-in refrigerator, oven, range, cooktop

– Built-in dishwasher

– Central air conditioning and heating system

– In-unit washer/dryer that is included with the lease

If these break down due to mechanical failure or age, your renters insurance does not pay to repair or replace them. Your landlord is responsible for fixing or replacing them per the lease and local habitability laws.

Coverage Scenarios: What’s Protected and Under What Circumstances

The following table breaks down common appliance-related incidents to clarify exactly does renters insurance cover appliances in various situations.

| Scenario | Covered by Renters Insurance? | Who is Responsible / Coverage Details |

|---|---|---|

| Your personal microwave is stolen. | YES | Covered under personal property for theft, subject to your deductible and policy limits. |

| The landlord’s refrigerator motor burns out. | NO | Mechanical breakdown is excluded. Landlord must repair or replace the appliance. |

| A kitchen fire damages both your toaster and the landlord’s oven. | YES (for your toaster only) | Fire is a covered peril. Your policy covers your toaster. The landlord’s insurance covers their oven. |

| The landlord’s dishwasher leaks, ruining your wooden kitchen table. | YES (for your table) | Sudden water discharge is a covered peril. Your policy covers your damaged table. Landlord fixes the dishwasher. |

| Your window AC unit falls and breaks due to faulty installation. | PROBABLY NO | Breakage from your own faulty installation is not a covered peril. It may be considered neglect. |

| A power surge fries your personal refrigerator’s circuit board. | MAYBE (check policy) | Many policies exclude damage from power surges to the appliance itself. Some offer limited coverage or require an endorsement. |

| You accidentally break the glass turntable in the landlord’s microwave. | YES (under Liability) | If you are liable for damaging the landlord’s property, your liability coverage may pay for the repair. |

The Role of Liability Coverage for Appliance Damage

If you cause damage to a landlord-owned appliance through negligence (e.g., you overload and break the washing machine, or cause a grease fire that ruins the stove), your personal liability coverage (Coverage E) may cover the cost to repair or replace it. This protects you from having to pay out of pocket for damaging the landlord’s property. However, simple mechanical failure from age is not your negligence.

Gaps in Coverage: Mechanical Breakdown and Power Surges

Standard renters insurance covers sudden, external events (perils), not internal mechanical failure. Two common gaps are:

1. Mechanical/Electrical Breakdown: When an appliance simply stops working.

2. Power Surge Damage: Many policies exclude or limit coverage for appliances damaged by electrical surges.

Optional Endorsements to Fill the Gaps

– Equipment Breakdown Coverage: This add-on (also known as “boiler and machinery” coverage) can be added to your renters policy. It covers the repair or replacement of personal appliances and systems (even some you might be responsible for, like a portable AC) that break down due to mechanical or electrical failure. It often includes coverage for spoilage if your refrigerator breaks.

– Enhanced Electronics or Surge Protection: Some insurers offer endorsements that lower or remove the sub-limits for electronics and appliances damaged by power surges. A standard policy might only offer $500 for surge damage; an endorsement can increase this significantly.

Steps to Take When an Appliance Issue Occurs

1. Identify the Appliance Owner: Check your lease to see what appliances are provided. Determine if it’s yours or the landlord’s.

2. Determine the Cause: Is it a breakdown (motor died) or damage from a covered event (fire, water leak)?

3. For Landlord Appliances (Breakdown): Notify your landlord or property manager in writing immediately. They are responsible for repairs.

4. For Your Appliances (Covered Damage): If damaged by a covered peril, document the damage and the cause with photos. File a claim with your renters insurance.

5. For Damage Caused by an Appliance: If a landlord’s appliance leaks and damages your belongings, document everything, notify the landlord, and file a claim with your insurer for your damaged items.

6. Mitigate Further Damage: Take reasonable steps to prevent more loss (e.g., turn off water to a leaking appliance, unplug it).

Preventing Appliance Disputes with Your Landlord

Your lease should clearly state which appliances are provided and who is responsible for maintenance and repair. Conduct a move-in inspection, noting the make, model, and condition of all landlord-provided appliances. This creates a record to prevent disputes over pre-existing damage or wear and tear when you move out.

Cost Considerations and Is Extra Coverage Worth It?

The decision to add equipment breakdown coverage depends on the value of your personal appliances. If you own several high-end personal appliances (an expensive espresso machine, high-end window AC units, a portable washer/dryer), the endorsement might be worthwhile for a modest addition to your renters insurance cost (often $20-$50 per year). For renters with few personal appliances, it may be less critical. Always weigh the cost of the endorsement against the potential repair or replacement cost of your items.

Conclusion: Know Your Stuff, Know Your Policy

In summary, does renters insurance cover appliances? It provides important but specific protection. It safeguards your personal appliances from external disasters and covers damage that landlord appliances cause to your belongings. It does not function as a home warranty for mechanical failures. By understanding the ownership divide, knowing your policy’s covered perils, and considering optional endorsements for breakdowns, you can avoid unexpected costs and ensure a quick resolution when appliance issues arise. Review your lease and your policy today to know exactly where you stand. For a comprehensive look at your protections, explore all renters insurance options.

Frequently Asked Questions (FAQ)

Does renters insurance cover food spoilage if the refrigerator breaks?

Only under specific conditions. Standard renters insurance does not cover spoilage from a mechanical breakdown. However, if the breakdown is caused by a covered peril (like a power outage from a windstorm), some policies include a small limit (e.g., $500) for food spoilage. Equipment breakdown coverage would also typically include spoilage coverage.

What if my personal appliance causes a fire or flood?

Your renters insurance provides crucial coverage in two ways: 1) Personal Property: Covers damage to your other belongings from the fire/water. 2) Liability: If your appliance (e.g., a space heater) causes a fire that damages the building or other units, your liability coverage pays for those damages and your legal defense.

Are smart home appliances (like a smart fridge) covered differently?

They are covered as personal property if you own them. The same perils apply. However, their higher value may mean they exceed general category limits. Additionally, if they are damaged by a cyber event (hacking), that is typically not covered. You may need to schedule very high-value smart appliances.

My landlord’s appliance is old and inefficient. Will insurance pay to upgrade it?

No. Insurance, whether yours or the landlord’s, only pays to repair or replace with “like kind and quality.” It does not pay for upgrades. If the landlord’s 15-year-old refrigerator dies, their insurance or they themselves would pay for a comparable basic model, not a top-of-the-line upgrade.

Does renters insurance cover the cost of using a laundromat if my washer breaks?

No. Renters insurance does not cover incidental costs or inconvenience due to an appliance breakdown. Additional Living Expenses (ALE) only applies if your entire rental is uninhabitable due to a covered loss, not just if one appliance is broken.

What if I’m not sure who is responsible for an appliance?

Always refer to your written lease agreement first. If it’s unclear, ask your landlord in writing for clarification. For common areas (like a shared laundry room), the landlord is almost always responsible. Never assume—get it in writing to avoid liability disputes.

Where can I learn more about landlord-tenant responsibilities?

For general information on property insurance principles, the Insurance Information Institute’s article on renters insurance coverage provides a good overview, though for specific landlord-tenant laws, your state’s housing authority or a local tenants’ rights organization is the best resource.