Pet liability insurance for renters is a crucial form of protection, typically included within the personal liability coverage of a standard renters insurance policy. It provides financial coverage if your dog, cat, or other pet injures someone (e.g., bites a guest or neighbor) or damages their property. This coverage pays for the injured party’s medical bills, legal fees if you’re sued, and settlement costs up to your policy’s liability limit. However, significant caveats exist: many insurers have breed restrictions (often excluding pit bulls, Rottweilers, etc.) and may deny coverage for animals with a history of aggression. If your pet is excluded, you may need a separate animal liability policy. Understanding this coverage is a key part of responsible pet ownership and comprehensive renters insurance planning.

How Pet Liability Coverage Works in a Renters Policy

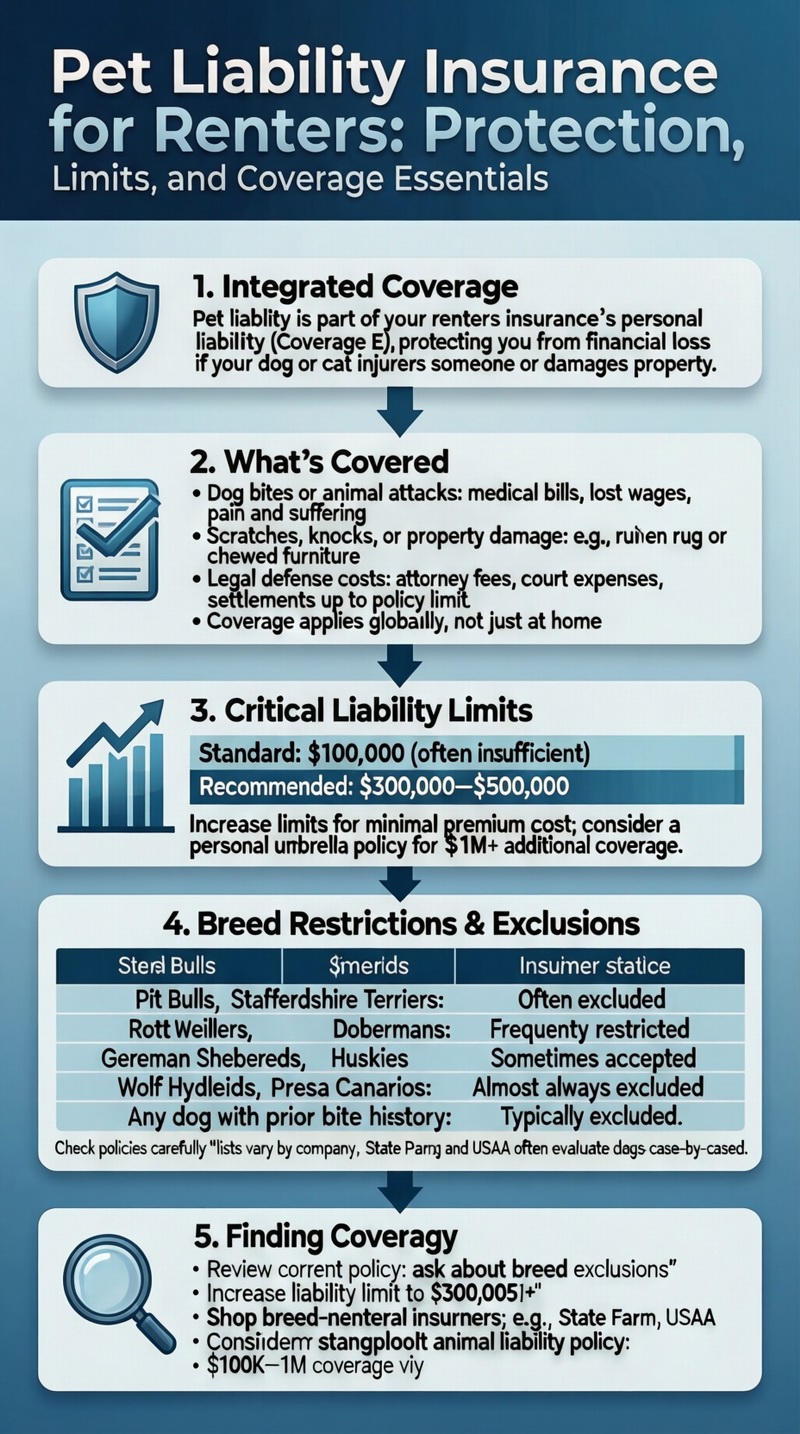

When exploring pet liability insurance for renters, it’s essential to know it’s not usually a standalone product. Instead, it’s integrated into the personal liability section (Coverage E) of your standard renters insurance policy. This coverage is designed to protect your personal assets (savings, future income) if you are found legally responsible for bodily injury or property damage to others. Since pet-related incidents are a common cause of such liability, they are included, subject to the policy’s general terms and exclusions. If your dog bites a delivery person, your liability coverage would pay for their medical expenses, lost wages, and pain and suffering, up to your chosen limit (e.g., $100,000 or $300,000). It would also provide a legal defense if you are sued. This is a core component of your renters insurance coverage.

What’s Typically Covered Under Pet Liability

Coverage applies to a wide range of incidents involving pets you own or keep:

– Dog Bites & Animal Attacks: The most common claim. Covers medical bills for the victim.

– Scratching or Knocking Someone Over: If your cat scratches a guest or your large dog jumps and injures someone.

– Property Damage: If your pet damages someone else’s property (e.g., your dog ruins a neighbor’s expensive rug or chews their patio furniture).

– Legal Defense Costs: Attorney fees, court costs, and settlements or judgments awarded against you, up to your policy limit.

Coverage usually applies anywhere in the world, not just at your rental home.

The Critical Role of Liability Limits

The average cost of a dog bite claim nationally exceeds $60,000, and serious injuries can lead to lawsuits in the hundreds of thousands. Standard liability limits of $100,000 may be insufficient. For pet owners, it’s strongly advised to carry at least $300,000 to $500,000 in personal liability coverage. You can increase this limit on your renters policy for a modest premium increase. For even greater protection, consider a personal umbrella policy, which provides an extra $1 million or more in liability coverage above the limits of your renters and auto policies.

Breed Restrictions, Exclusions, and How to Navigate Them

The most significant hurdle for renters with pets is insurer-imposed breed restrictions. Due to actuarial data on bite frequency and severity, many companies maintain lists of “restricted” or “excluded” dog breeds. If you own a dog on this list, your renters policy may deny liability coverage for any incident involving that animal, or the company may refuse to insure you altogether.

| Commonly Restricted Breeds* | Typical Insurance Policy Stance | Actions for Owners of These Breeds |

|---|---|---|

| Pit Bull Terriers, Staffordshire Terriers | Often Excluded | Shop for companies with no breed restrictions (e.g., State Farm, USAA). Disclose breed upfront. Consider a separate animal liability policy. |

| Rottweilers, Doberman Pinschers | Frequently Restricted | Same as above. Provide documentation of training, Canine Good Citizen certification, which may help. |

| German Shepherds, Huskies, Malamutes | Sometimes Restricted | May be accepted by some insurers but subject to underwriting. Full disclosure is required. |

| Wolf Hybrids, Presa Canarios | Almost Always Excluded | Extremely difficult to find coverage under standard renters insurance. A specialty animal liability policy is necessary. |

| Any dog with a prior bite history | Typically Excluded | Must be disclosed. Will likely preclude coverage under a standard policy, requiring a specialty policy. |

*Lists vary significantly by insurance company.

Other Common Exclusions and Limitations

Beyond breed restrictions, standard policies may exclude:

– Business Activities: Liability from pets used for business (breeding, guarding, therapy).

– Intentional Injury: If you intentionally sic your dog on someone.

– Owned vs. Kept Animals: Coverage typically applies to pets you own. If you’re dog-sitting a friend’s restricted breed, an incident may not be covered.

– Exotic Pets: Reptiles, large birds, or unusual mammals may not be covered. Check your policy.

Finding Insurers Without Breed Restrictions

Some major insurers, like State Farm and USAA (for eligible members), are known for evaluating dogs on a case-by-case basis rather than automatically excluding breeds. They focus on the individual dog’s history and temperament. When shopping for pet liability insurance for renters, be upfront about your dog’s breed and ask explicitly about the company’s underwriting policy. Getting a policy from a breed-neutral insurer is the most straightforward solution.

Securing Coverage: Steps for Renters with Pets

To ensure you and your pet are protected, follow this action plan:

1. Review Your Current Policy. Read the liability section and exclusions. Look for any mention of “animals,” “pets,” or “dogs.” Call your agent to confirm if your specific pet is covered and ask about breed restrictions.

2. Increase Your Liability Limits. If your pet is covered, boost your liability limit to at least $300,000. The renters insurance cost increase for higher limits is minimal compared to the risk.

3. Shop for a New Policy If Needed. If your current insurer excludes your pet, get quotes from breed-neutral companies. Be honest about your pet’s breed and history during the application.

4. Consider a Separate Animal Liability Policy. If you cannot find a standard renters policy that covers your pet, companies like Einhorn Insurance (through the Federation of Insured Dog Owners) or DogsBite.org-listed insurers offer standalone animal liability policies. These can provide $100,000-$1,000,000 in coverage specifically for pet-related incidents.

5. Document Your Pet’s Good Behavior. Keep records of obedience training certificates (like AKC Canine Good Citizen), vaccination records, and letters from veterinarians attesting to temperament. This can help with underwriting.

6. Comply with Local Laws and Lease Terms. Ensure your pet is licensed, vaccinated (especially rabies), and that you comply with any lease requirements regarding pets, breed, or weight limits.

The Importance of a “Canine Liability” Umbrella Policy

For owners of large dogs or breeds that might be seen as higher risk, a personal umbrella policy is a powerful, cost-effective tool. It sits on top of your renters (and auto) liability coverage. If a pet incident exhausts your $300,000 renters liability limit, the umbrella policy kicks in to cover the next $1 million (or more). It provides an essential extra layer of security for your financial future.

What to Do If Your Pet Injures Someone

Despite precautions, incidents happen. Knowing the procedure is part of responsible pet liability insurance for renters ownership.

1. Secure Your Pet and Ensure Safety. Immediately restrain your pet and separate them from the victim.

2. Provide Assistance and Information. Offer first aid if appropriate. Exchange names and contact information with the victim. Be polite but do not admit fault or make statements like “My dog has never done this before,” which could be used against you.

3. Seek Medical Attention. Encourage the victim to seek professional medical evaluation, even for minor injuries, to prevent infection.

4. Document the Incident. Take photos of the injury and the location. Note the names and contact info of any witnesses.

5. Notify Your Insurance Company. Contact your renters insurance provider as soon as possible to report the incident and start the claims process. Provide all collected information.

6. Cooperate Fully. Work with the claims adjuster, provide any requested documentation, and inform them of any communication from the victim or their attorney.

7. Report as Required by Law. In many jurisdictions, dog bites must be reported to local animal control. Your insurer can guide you on this.

Will My Premium Increase After a Pet Liability Claim?

Almost certainly. Filing any liability claim, especially a significant one like a dog bite, marks you as a higher risk. Your insurer may significantly increase your premium at renewal or even choose not to renew your policy. In some cases, they may add an exclusion for that specific pet. This underscores the importance of prevention and adequate initial limits.

Conclusion: Non-Negotiable Protection for Pet Owners

In summary, pet liability insurance for renters is not an optional extra—it’s a fundamental component of financial responsibility for any tenant with a dog, cat, or other animal. Standard renters policies provide a base level of protection, but breed restrictions and low limits can leave you dangerously exposed. By proactively reviewing your policy, shopping with breed-neutral carriers if necessary, and securing high liability limits (or an umbrella policy), you protect not just your pet, but your entire financial well-being from the potentially ruinous cost of a single incident. Don’t wait for an accident to discover your coverage is inadequate. Explore all renters insurance options and secure the right protection today.

Frequently Asked Questions (FAQ)

Does pet liability insurance cover damage my pet does to my own apartment?

No. Pet liability insurance covers injury or damage to other people and their property. Damage your dog or cat causes to your own rental unit (chewed baseboards, scratched floors, stained carpets) is not covered by the liability or personal property sections of your renters insurance. This is considered a maintenance issue, and you are responsible for repair costs, which may be deducted from your security deposit.

Are cats covered under renters liability insurance?

Yes, typically. Cats are generally covered under the personal liability portion of a renters policy. While cat bites are less common, they can cause serious infection. More commonly, liability could arise if your cat trips a guest, causing a fall, or scratches someone. Breed restrictions are overwhelmingly focused on dogs, but it’s always wise to confirm with your insurer.

What if my lease requires pet liability insurance?

An increasing number of landlords require tenants with pets to carry renters insurance with a specific minimum liability limit (e.g., $100,000) and to name the landlord as an “additional interest” or “certificate holder.” You must provide proof of insurance (a certificate of insurance) before move-in. Failure to maintain the required insurance can be a lease violation, potentially leading to fines or eviction.

Can I get pet liability insurance if I don’t have a renters policy?

Yes, but it’s less common and may be more expensive. Standalone animal liability policies exist for dog owners, particularly those with restricted breeds. These policies provide liability-only coverage for your pet. However, for most renters, bundling pet liability with a full renters insurance policy that also protects your belongings is the most practical and economical approach.

Does my policy cover veterinary bills if my pet is injured?

No. Standard renters insurance does not cover veterinary bills or the medical costs for your own pet. That is the function of a separate pet health insurance policy. Renters insurance liability coverage is exclusively for third-party injuries or damages caused by your pet.

What happens if I don’t disclose my dog’s breed to the insurer?

This is known as material misrepresentation and is very serious. If you fail to disclose a restricted breed and later file a claim for a dog bite, the insurance company will likely investigate, discover the omission, and deny the claim. They could also cancel your policy retroactively. Always be fully transparent to ensure your coverage is valid.

Where can I find more information on responsible pet ownership and liability?

For authoritative resources on dog bite liability and prevention, the Insurance Information Institute’s dog bite liability page provides excellent statistics, legal context, and tips for reducing risk, which complements the insurance information provided here.