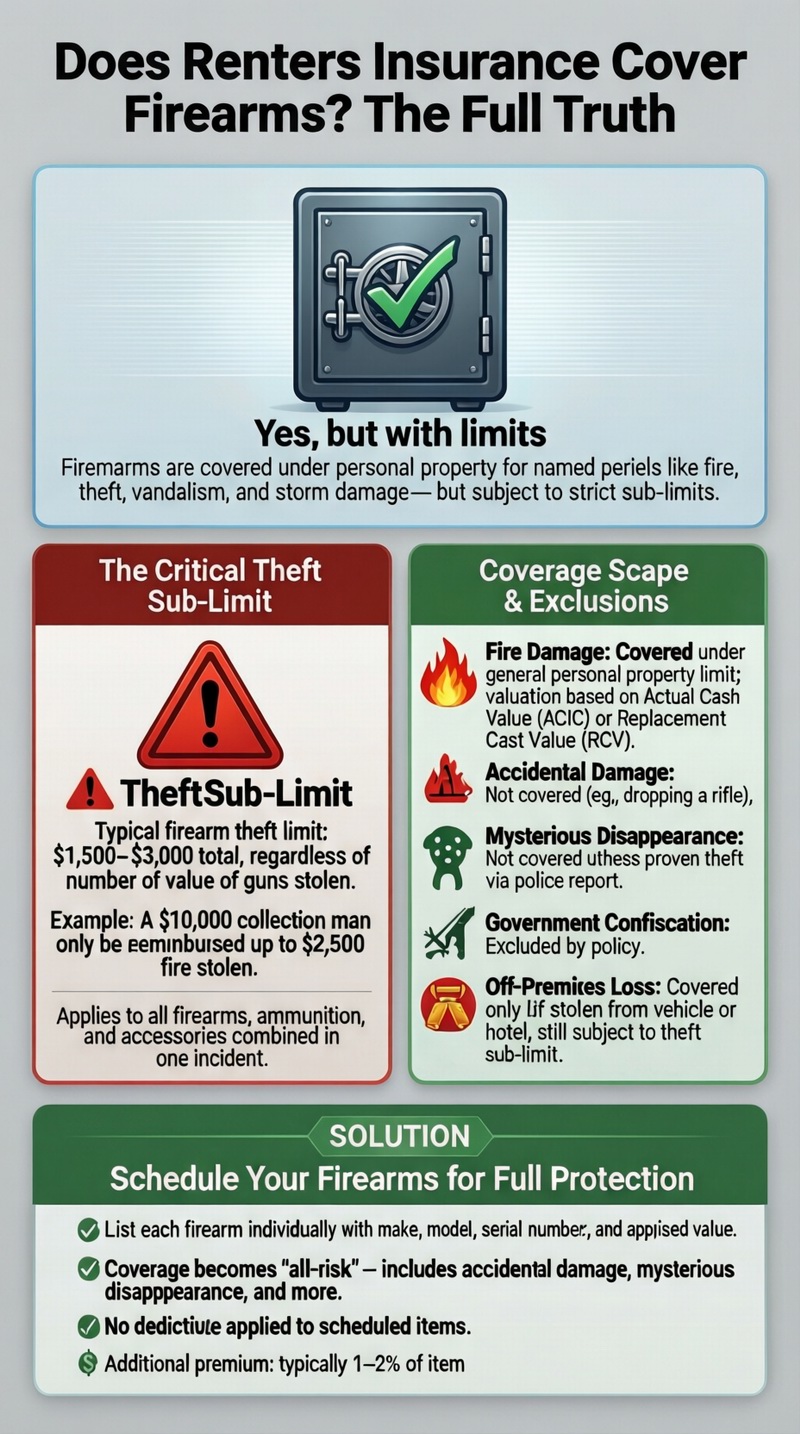

The answer is: Yes, renters insurance does cover firearms, but with very important limitations that often leave gun owners underinsured. Standard renters insurance policies include firearms under personal property coverage for named perils like theft, fire, or vandalism. However, they impose a low special sub-limit for theft of firearms, typically ranging from $1,500 to $3,000 total, regardless of how many guns you own or their actual value. This means a collection worth $10,000 might only be covered for $2,000 if stolen. To get full coverage, you must “schedule” your firearms—add them individually to your policy with a description and value, often for an additional premium. This guide explains the details, exclusions, and steps to properly insure your guns. Start with the fundamentals in our article on what renters insurance is.

Standard Renters Insurance Coverage for Firearms

When asking, “does renters insurance cover firearms?” it’s crucial to understand that guns are considered personal property. Under a standard HO-4 policy, they are covered for the same named perils as your other belongings, such as fire, lightning, windstorm, hail, explosion, riot, aircraft, vehicles, smoke, vandalism, theft, falling objects, and damage from plumbing/heating systems. So, if your apartment catches fire and your gun safe is damaged, or a tornado destroys your home, your firearms would be covered for their insured value, subject to the policy’s overall limits and conditions. This is part of your broader renters insurance coverage.

The Critical Theft Sub-Limit

The most significant restriction is the sub-limit for theft. Insurance companies view firearms as high-risk items for theft due to their portability and value. Therefore, they cap the amount they will pay for stolen guns. This limit is an aggregate limit, meaning it’s the maximum payout for all firearms, ammunition, and accessories stolen in a single incident. For example, if your policy has a $2,500 firearm theft sub-limit and thieves steal three guns worth a total of $6,000, the maximum you could recover from insurance for those items is $2,500, minus your deductible. This sub-limit applies only to theft; other perils like fire are subject to your overall personal property limit, but still may have special valuation rules.

Coverage for Ammunition and Accessories

Ammunition, scopes, cases, and gun safes are generally covered under the same rules as the firearms themselves. They are often included within the firearm sub-limit for theft. In a fire loss, they would be covered under your general personal property limit. However, high-value optics (e.g., a $2,000 night vision scope) might also be subject to separate sub-limits for electronics or jewelry. It’s important to itemize and value accessories separately when reviewing your coverage needs.

Understanding Limits, Exclusions, and Scheduling

The following table breaks down key scenarios to clarify does renters insurance cover firearms in practice, highlighting where standard coverage falls short and what solutions exist.

| Scenario / Loss Type | Covered by Standard Policy? | Coverage Details & Limitations |

|---|---|---|

| Firearms stolen in a burglary | YES, but sub-limited | Subject to the special firearm theft limit (e.g., $2,500 total). You must file a police report. Losses exceeding the sub-limit are not covered unless guns are scheduled. |

| Firearms damaged in an apartment fire | YES | Covered under the general personal property limit, not the theft sub-limit. Valuation (ACV vs. RCV) applies. A melted $1,500 rifle might only be worth $500 as ACV. |

| Loss or damage while hunting or traveling | YES (Off-Premises) | Covered, but subject to the same theft sub-limit if stolen from your vehicle or hotel. Off-premises coverage is usually 10% of your total property limit, but the firearm theft sub-limit still applies. |

| Accidental damage (e.g., dropping a rifle) | NO (typically) | Standard policies cover named perils, not “accidental breakage.” Dropping and breaking a scope is not a covered event unless it results from a covered peril like a fall caused by a windstorm. |

| Mysterious disappearance | NO | If a firearm is lost (e.g., left behind at a range) and not proven to be stolen, it is not covered. |

| Government confiscation | NO | Seizure by law enforcement or other authorities is excluded. |

Actual Cash Value vs. Replacement Cost for Firearms

This distinction is vital. Most standard policies pay Actual Cash Value (ACV), which is the replacement cost minus depreciation. Firearms can depreciate based on age, model, and condition. A 20-year-old hunting rifle may have an ACV far below what it would cost to buy a comparable new one. Replacement Cost Value (RCV) coverage, often an optional upgrade, pays the amount to buy a new firearm of like kind and quality. For gun owners, RCV is highly recommended, especially for modern firearms. However, even with RCV, the theft sub-limit still caps the total payout.

How to “Schedule” Your Firearms for Full Coverage

Scheduling is the process of listing individual high-value items on your policy with a specific description and agreed-upon value (often based on an appraisal or receipt). For scheduled firearms:

– The theft sub-limit no longer applies. Each scheduled item is covered for its stated value.

– Coverage is often “all-risk,” meaning it protects against a wider range of perils, including accidental damage (e.g., dropping) or mysterious disappearance, which are not covered under the standard policy.

– There is usually no deductible applied to scheduled items.

To schedule a firearm, you’ll typically need the make, model, serial number, and often a recent appraisal or receipt proving value. There is an additional premium, usually 1-2% of the item’s value per year.

Steps to Properly Insure Your Gun Collection

To ensure you’re not left with a devastating financial loss, follow these steps:

1. Know Your Policy. Read your policy documents to find the “special limits of liability” section. Identify the exact dollar sub-limit for “firearms, theft.”

2. Take a Detailed Inventory. Create a list of every firearm, including make, model, serial number, caliber, and any accessories. Take clear photographs of each gun and its serial number. Keep this list and photos in a secure, separate location (like a cloud drive).

3. Get Professional Appraisals. For antique, custom, or high-value firearms, get a professional appraisal from a certified gunsmith or dealer to establish current market or replacement value.

4. Calculate Total Value. Add up the replacement cost of your entire collection and compare it to your policy’s theft sub-limit and overall personal property limit.

5. Contact Your Insurance Agent. Discuss your collection. Ask about:

– The cost to increase your overall personal property limit.

– The cost and process to schedule your firearms.

– Whether they offer a “collectibles” or “valuable items” policy that might be more suitable for large collections.

6. Secure Your Firearms. Many insurers offer discounts for gun safes, and safe storage may be required for scheduled items. It also reduces theft risk. Use a quality safe bolted to the structure.

Does a Gun Safe Reduce Insurance Costs?

While it may not directly lower your premium for the firearm coverage itself, owning a certified gun safe can:

– Make you eligible for a general home security discount on your overall renters policy.

– Be a requirement from the insurer to schedule high-value firearms.

– Prevent theft, thereby avoiding a claim that would increase your future premiums.

Always inform your insurer about your safe, as it demonstrates risk mitigation. For insights into how security affects renters insurance cost, review our guide.

Special Considerations and State Laws

Insurance regulations can vary by state. Some states may have specific rules or consumer protections regarding the insuring of firearms. Furthermore, you must comply with all local, state, and federal laws regarding firearm ownership, storage, and transportation. Insurers may deny a claim if a stolen firearm was not stored in compliance with local safe-storage laws (e.g., not in a locked container). Always prioritize legal compliance as part of your risk management. For a wide view of providers and policies, explore all renters insurance options.

What About Liability Coverage for Firearm-Related Incidents?

This is separate from property coverage. The liability portion of your renters insurance (Coverage E) may provide coverage if you are found legally liable for bodily injury or property damage caused by the accidental discharge of a firearm. However, intentional acts or criminal use of a firearm are excluded. It’s crucial to have high liability limits ($300,000-$500,000 or more) if you own firearms, as related lawsuits can be extraordinarily costly. Consider an umbrella policy for additional liability protection above your renters limits.

Conclusion: Don’t Assume You’re Covered

In summary, does renters insurance cover firearms? It provides a baseline of protection but is woefully inadequate for most gun owners due to restrictive theft sub-limits. Assuming your collection is fully covered by a standard policy is a costly mistake. The responsible course of action is to conduct a thorough inventory, understand your policy’s limits, and proactively schedule your firearms to ensure they are insured to their full value against a broad range of perils. The modest additional premium for scheduling is a small price to pay for the peace of mind that comes with knowing your valuable assets are properly protected. Take action today to review and update your coverage.

Frequently Asked Questions (FAQ)

Does renters insurance cover antique or collectible firearms?

Yes, but standard sub-limits still apply, and ACV can be problematic. Antique firearms may appreciate, but ACV may not reflect collector value. For any collectible, historical, or custom firearm, scheduling is essential. You will need a professional appraisal to establish the agreed value for the schedule. This ensures you are paid the true collector’s value, not just the base material value.

If my firearm is used in a crime after being stolen, am I liable?

Your renters insurance liability coverage is not designed to protect you if your stolen firearm is used in a crime. That would be a criminal act by a third party. However, if the victim’s family sues you for negligent storage leading to the theft, your liability coverage may provide a legal defense. The outcome would depend on the specifics of the case and local laws. Secure storage is your best defense against such lawsuits.

Are airsoft, BB, or pellet guns covered?

Typically, yes, they are covered as personal property, but they may not be subject to the same strict firearm theft sub-limit. They might fall under general personal property or a different category like “sports equipment.” Check your policy or ask your agent. High-value airsoft replicas might still warrant scheduling.

Do I need to notify my insurer that I own firearms?

You are not generally required to disclose firearm ownership when applying for a standard renters policy. However, you must disclose them when scheduling or if asked directly on an application. Failure to schedule high-value items means you accept the standard sub-limits. Being transparent ensures you get the right coverage and avoids claims disputes.

Will my premium skyrocket if I schedule my guns?

Not necessarily. The additional premium for scheduling is usually a small percentage (1-2%) of the item’s value per year. For a $1,000 firearm, that’s roughly $10-$20 annually. This is often very reasonable for the dramatic increase in coverage (full value, all-risk, no deductible). It’s far more cost-effective than finding yourself underinsured after a theft.

What documentation do I need for a firearm insurance claim?

For any claim, you’ll need:

1. A police report (for theft).

2. Your pre-loss inventory with descriptions, photos, and serial numbers.

3. Proof of ownership (purchase receipts, appraisals, firearm registration documents where applicable).

4. For scheduled items, the schedule from your policy and the appraisal used to set the value.

Thorough documentation is the key to a smooth and full settlement. The Insurance Information Institute’s guide to home inventories is an excellent resource.

Does renters insurance cover a gun safe itself?

Yes. A gun safe is considered personal property. If it is damaged by a covered peril (like a fire) or stolen, it is covered under your personal property coverage, subject to your overall limit and deductible. Its contents (the firearms) are covered separately under the rules discussed above.