The short answer is: Yes, your renters insurance often does cover a storage unit, but with significant limitations and conditions. Most standard renters insurance policies provide “off-premises” coverage, which typically extends a portion of your personal property protection to belongings stored elsewhere, including in a storage facility. However, this coverage is usually limited to 10% of your total personal property limit. So, if you have $30,000 of coverage for your apartment, you may only have $3,000 for items in storage. Furthermore, certain high-risk perils like mold, mildew, vermin, and flood damage are often excluded for storage units. It’s crucial to review your policy, understand the sub-limits, and potentially purchase additional coverage from the storage facility for full protection. For foundational knowledge, start with our article on what renters insurance is.

How Off-Premises Coverage Works for Storage Units

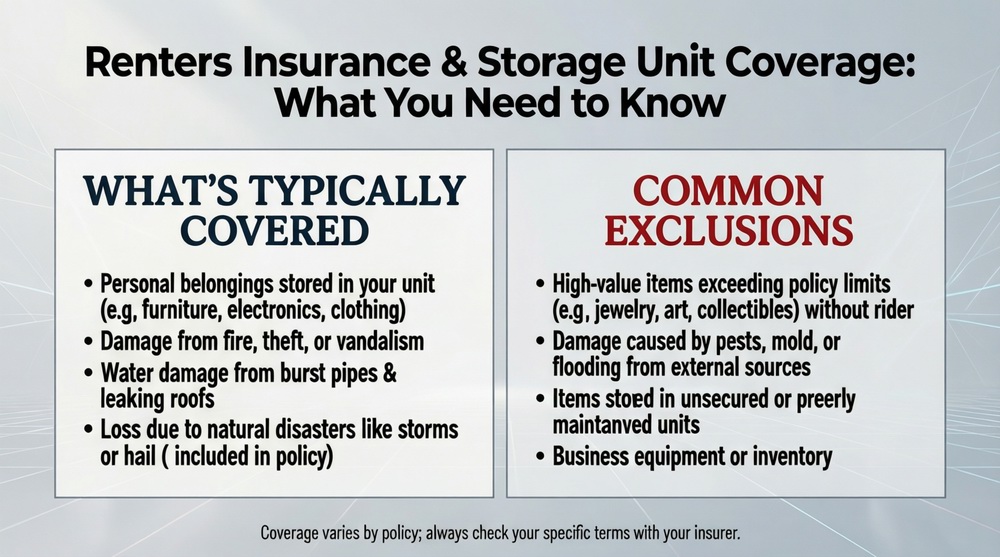

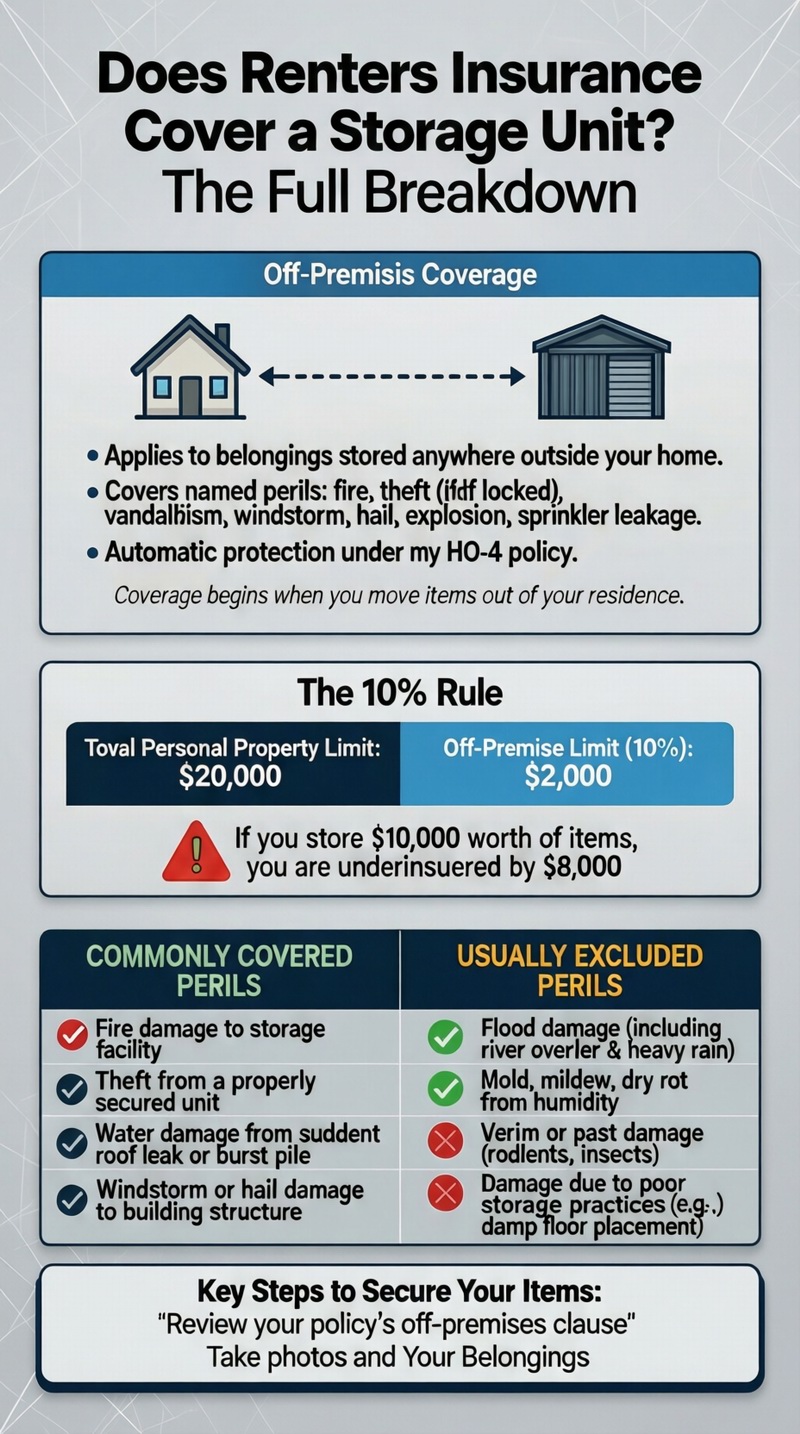

When asking, “does my renters insurance cover a storage unit?” you’re tapping into the “off-premises” clause found in most standard renters insurance policies (the HO-4 form). This provision is designed to protect your belongings anywhere in the world, not just inside your primary residence. It applies to items stolen from your car, lost while traveling, or damaged while in a self-storage facility. The coverage is automatic for the same “named perils” listed in your policy, such as fire, lightning, windstorm, hail, explosion, theft, vandalism, and sprinkler leakage. So, if a fire breaks out in the storage facility and damages your items, your renters insurance should respond, subject to your deductible and the off-premises limit. Understanding this is part of knowing your full renters insurance coverage.

The 10% Rule: Understanding Your Coverage Limit

The most critical limitation is the off-premises coverage cap. Insurers apply this to manage risk, as belongings in an unattended, commercial storage facility are statistically at a different risk level than those in your home. For example:

– Your Total Personal Property Limit: $20,000

– Standard Off-Premises Cap (10%): $2,000

– Maximum coverage for items in your storage unit: $2,000

This means if you have $10,000 worth of furniture and seasonal items in storage, you are underinsured by $8,000. You must calculate the total value of your stored belongings to see if the automatic coverage is sufficient.

Covered vs. Commonly Excluded Perils for Storage

While your policy covers many perils, the storage environment introduces specific risks that are often excluded:

Typically COVERED: Fire, theft (if unit is properly locked), vandalism, wind damage to the building, water damage from a burst pipe within the facility.

Often EXCLUDED or LIMITED:

– Flood damage: Standard policies exclude flood. If the storage facility is in a flood zone, you need separate flood insurance.

– Earthquake damage: Excluded unless you have an endorsement.

– Mold, Mildew, Dry Rot: Damage from gradual humidity or temperature changes is usually excluded as “gradual deterioration.”

– Vermin/Pest Damage: Rats, insects, or other pests damaging your items are typically not covered.

– Poor Maintenance/Neglect: If your items are damaged because you stored them improperly (e.g., placing a mattress directly on a damp floor), the claim may be denied.

Key Factors and Scenarios: What You Must Know

Navigating the question “does my renters insurance cover a storage unit?” requires looking at specific situations. The following table outlines common scenarios and how coverage typically applies, helping you gauge your level of risk and protection.

| Scenario | Is it Usually Covered? | Critical Details & Tips |

|---|---|---|

| Theft from a properly locked unit | YES | You MUST have a police report. Coverage is subject to the off-premises limit and your deductible. The facility’s security measures may affect the claim. |

| Fire damages the entire facility | YES | A covered peril. File a claim with your insurer. The storage facility’s insurance covers the building; yours covers your contents. |

| Water damage from a roof leak | YES (usually) | If water enters due to a sudden event like a storm-damaged roof, it’s likely covered. Gradual seepage over time may be excluded. |

| Flooding from heavy rain or river overflow | NO | Standard renters insurance excludes flood. You need a separate flood insurance policy, even for contents in storage. |

| Mold on furniture due to humidity | NO | Considered gradual deterioration and maintenance-related. Use climate-controlled units for sensitive items and desiccants. |

| Rodents chewing through boxes | NO | Vermin damage is almost always excluded. Choose a clean, well-maintained facility and use plastic, sealed totes. |

The Importance of the Storage Facility’s Contract (Lease Agreement)

When you rent a storage unit, you sign a contract. This document almost certainly includes a limitation of liability clause, stating that the facility is not responsible for damage to your belongings from fire, flood, theft, or pests, even if caused by their negligence. They are only required to carry insurance on the building itself. This contract underscores why your own insurance is vital—you cannot rely on the storage company to reimburse you for losses.

How to Increase Your Coverage for Stored Items

If your stored items exceed the 10% off-premises limit, you have options:

1. Increase Your Overall Personal Property Limit: If you increase your total limit from $20,000 to $40,000, your storage coverage automatically increases from $2,000 to $4,000 (10%). This may be the simplest solution if you also need more coverage at home.

2. Purchase a “Scheduled Property” Endorsement: For specific high-value items (e.g., an antique collection, expensive sports equipment), you can schedule them. This provides stated-value coverage regardless of location, often with no deductible.

3. Buy Insurance Through the Storage Facility: Most facilities offer tenant insurance policies or partner with an insurer. This can be convenient and designed specifically for storage risks, but compare the cost and coverage carefully against enhancing your own renters policy.

Steps to Take Before Storing Your Belongings

Proactive steps can prevent losses and ensure a smooth claims process if you need to answer “does my renters insurance cover a storage unit?” with a claim.

1. Review Your Policy. Read your policy’s “off-premises” coverage section. Call your agent or insurer to confirm the exact percentage limit and any storage-specific exclusions.

2. Take a Detailed Inventory. Create a list and take photos/videos of all items going into storage. Note their approximate value and age. This is your proof of ownership and value for a claim.

3. Calculate Total Value. Add up the value of everything you’re storing. If it exceeds your off-premises limit, take action to increase coverage.

4. Choose the Right Facility. Opt for a well-lit, secured facility with gated access, surveillance cameras, and good maintenance. For sensitive items, pay extra for a climate-controlled unit.

5. Pack and Store Smartly. Use sturdy, plastic sealed totes instead of cardboard boxes. Place pallets or shelves to keep items off the concrete floor. Do not store prohibited items (flammables, perishables, cash).

6. Keep Your Lease and Receipts. Save your storage rental agreement and any receipts for items purchased. This helps establish timelines and values.

What to Do If You Need to File a Claim for Stored Items

The process is similar to a home claim but with extra steps:

1. Discover the Loss: Document the scene with photos/videos immediately. Do not disturb evidence if it’s a theft.

2. Notify the Storage Facility Manager: File an incident report with them. Get a copy.

3. File a Police Report (for theft/vandalism): This is mandatory for theft claims.

4. Contact Your Renters Insurance Company: Start the claim, providing your policy number, the facility’s incident report, and police report number.

5. Provide Your Inventory and Documentation: Submit your pre-loss inventory, photos, and any receipts to the adjuster.

6. Cooperate with the Investigation: The adjuster will assess the damage and may inspect the storage unit.

Comparing Costs: Enhancing Your Policy vs. Facility Insurance

When your stored items need more protection, you’ll face a choice. Increasing your renters insurance limit is often cost-effective. For example, raising your total coverage by $10,000 might only increase your annual premium by $20-$40, subsequently raising your storage limit by $1,000. In contrast, insurance purchased through the storage facility might cost $10-$30 per month for $5,000-$10,000 of coverage. However, the facility’s policy might cover some perils yours excludes (like earthquake in certain areas). Get quotes for both and compare the renters insurance cost increase versus the standalone storage policy cost and terms. For a full market view, explore all renters insurance options.

When to Consider a Separate Storage Insurance Policy

A separate policy from the storage facility or a specialty insurer may be best if:

– You are storing very high-value items that exceed what you can reasonably add to your renters policy.

– Your renters insurance has very restrictive exclusions for storage (e.g., no theft coverage).

– You are storing items long-term and your renters policy might lapse if you move.

– You need “all-risk” coverage for perils like earthquake or flood that your renters policy doesn’t cover.

Conclusion: Proactive Protection is Essential

So, does my renters insurance cover a storage unit? The answer is a qualified yes, but it’s not a blank check. The standard 10% off-premises limit and common exclusions for mold, pests, and floods mean you cannot assume everything is protected. The key is to audit your stored belongings’ value, review your policy’s fine print, and proactively bridge any coverage gaps—either by increasing your renters limits or purchasing a separate storage policy. By taking inventory, choosing a secure facility, and understanding your contract, you can store your items with confidence, knowing you’ve built a financial safety net that matches the risk. Don’t let a disaster in your storage unit become a personal financial disaster.

Frequently Asked Questions (FAQ)

Does renters insurance cover a storage unit if I’m moving?

Yes, during the move. Your renters insurance typically covers belongings in transit and in temporary storage for a short period (often up to 30 days) as part of a move to a new primary residence. This is distinct from long-term storage. The standard off-premises limit and covered perils still apply. If you’re using a moving company, also check their liability coverage.

Are there items I should NEVER put in a storage unit?

Yes, and storing them may void insurance. Prohibited items typically include: perishable food, living plants/animals, flammable/combustible materials (gas, paint, chemicals), firearms, ammunition, explosives, illegal substances, irreplaceable items (cash, stock certificates), and unregistered vehicles. Storing these can invalidate both the facility’s rules and your insurance coverage.

Does the storage unit’s climate control affect my coverage?

Climate control itself doesn’t change your policy’s terms, but it helps prevent losses from excluded perils. Using a climate-controlled unit can prevent mold, mildew, and warping from humidity/temperature swings—damage that your renters insurance would likely deny. It’s a risk-mitigation step, not a coverage enhancement, but it’s highly recommended for sensitive items like electronics, wood furniture, artwork, and documents.

What if I cancel my renters insurance but still have items in storage?

Your coverage ends immediately upon cancellation. Your belongings in the storage unit would have NO insurance protection. If you no longer have a primary renters policy (e.g., you’ve moved in with family), you must secure a separate storage insurance policy or a non-owner (tenant’s) policy to maintain coverage for your stored items.

How does the deductible work for a storage unit claim?

It works the same as any claim. If you have a $500 deductible and suffer a $2,000 loss in your storage unit, you would receive $1,500 from your insurer. The deductible applies per claim, not per item. If the loss is below your deductible, it’s not worth filing a claim as you’d receive no payment and it could raise your rates.

Will filing a claim for my storage unit raise my renters insurance premium?

It likely will. Filing any claim, regardless of location, can lead to a premium increase at renewal because it indicates higher risk. For a small loss close to your deductible, paying out-of-pocket may be more cost-effective in the long run than facing higher premiums for 3-5 years.

Where can I find official information on property insurance?

For general, authoritative information on how property insurance functions, including concepts like off-premises coverage, a reliable resource is the Insurance Information Institute’s guide to renters insurance. They provide clear, unbiased explanations of policy terms and coverages.