A common concern for tenants is understanding what happens if someone gets hurt in their rental home. So, does renters insurance cover injuries? The answer is yes, in two distinct and important ways. Renters insurance provides crucial financial protection through two separate coverages: personal liability insurance and medical payments to others. These components work together to address injuries that occur to guests or other third parties on your rented property or, in some cases, due to your actions elsewhere. This guide will clarify the difference between these two coverages, explain what types of injuries are included, detail the claims process, and highlight critical exclusions. Understanding this protection is key to safeguarding your finances from the high costs associated with accidental injuries.

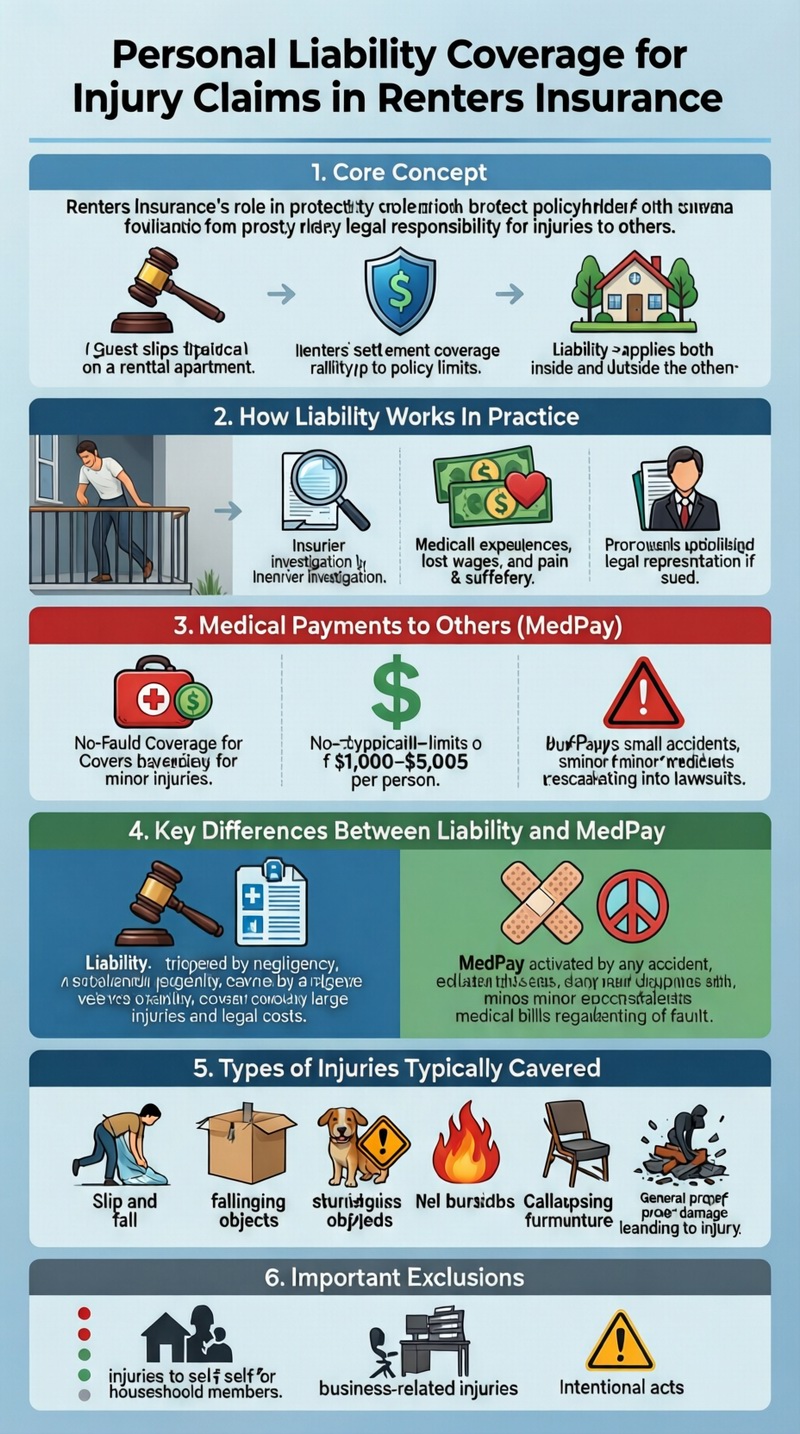

Personal Liability Coverage for Injury Claims

The primary way renters insurance covers injuries is through personal liability protection. This coverage applies if you are found legally responsible (negligent) for causing bodily injury to someone else. For example, if a guest slips on a wet floor you just mopped and breaks their wrist, they could sue you for medical bills and other damages. Your renters insurance liability coverage would provide a legal defense and pay for settlements or court judgments up to your policy limit. This coverage is not limited to injuries inside your home; it often extends to injuries you accidentally cause away from home, such as accidentally hitting someone with a golf ball. The question “does renters insurance cover injuries” is largely answered by this liability shield, which protects your savings, wages, and other assets from being seized to pay a judgment. For a foundational understanding, explore what renters insurance is.

How Liability Coverage Works in Practice

Imagine a scenario where a loose railing on your apartment balcony gives way while a friend is leaning on it, causing a fall. If you were aware the railing was loose and failed to report it to your landlord, you could be found negligent. The injured friend’s medical expenses could easily reach tens of thousands of dollars. Your renters insurance liability coverage would investigate the claim. If they determine you are liable, they would pay for the friend’s medical bills, lost wages, and “pain and suffering” up to your liability limit (e.g., $100,000 or $300,000). They would also hire and pay for an attorney to defend you if a lawsuit is filed. This coverage is activated by your legal responsibility, not just the occurrence of an injury. It is a critical part of your renters insurance coverage that addresses the most severe financial risks from accidents.

Medical Payments to Others Coverage

Separate from liability coverage, renters insurance typically includes “medical payments to others” (often called MedPay). This is a smaller, no-fault coverage designed to handle minor injuries without determining legal blame. If a guest trips and suffers a minor cut or sprain in your home, MedPay can cover their reasonable medical expenses, such as ambulance fees, X-rays, stitches, or doctor visits, regardless of who was at fault. The coverage limits are much lower, usually between $1,000 and $5,000 per person. The purpose of MedPay is to promote goodwill and prevent small incidents from escalating into larger liability lawsuits. By quickly paying for minor medical bills, it helps avoid legal disputes over negligence. It is important to note that MedPay does not cover injuries to you or members of your household; it is strictly for guests or others injured on your property.

Key Differences Between Liability and Medical Payments

Understanding the distinction is crucial. Liability coverage requires a finding of fault or negligence on your part and covers larger, more serious injuries and associated legal costs. Medical payments coverage is triggered simply by an accident occurring on your premises, with no need to prove fault, but it only covers smaller, immediate medical expenses. For example, if a guest cuts their finger on a broken glass you left on a counter, MedPay could cover the cost of the bandages and a tetanus shot. If the same guest falls down poorly lit stairs you were supposed to maintain and breaks their back, that would be a liability claim covering extensive medical treatment, rehabilitation, and potential legal damages. Both coverages work together to provide a comprehensive answer to “does renters insurance cover injuries?”

What Types of Injuries Are Typically Covered?

Renters insurance covers a wide range of accidental bodily injuries. Common examples include slip and fall accidents, injuries from falling objects, dog bites (subject to breed exclusions), burns from a kitchen accident, or injuries caused by a piece of your furniture collapsing. The coverage generally applies to injuries sustained by guests, service workers (like a delivery person), or even neighbors if you cause an incident that affects them (e.g., a fire that spreads). The key factor is that the injury must be accidental. The coverage is designed for unforeseen events, not intentional harm. As long as the injury is the result of an accident and you are either legally liable (for liability coverage) or it occurred on your premises (for MedPay), your renters insurance should respond.

Important Exclusions to Understand

While renters insurance covers many injury scenarios, there are important exclusions. First, it does not cover injuries to you or members of your household. Your own health insurance is for that. Second, injuries arising from business or professional activities conducted from your home are excluded. Third, injuries caused intentionally by you or a resident are not covered. Fourth, injuries related to the use of motor vehicles (car accidents) are covered by auto insurance, not renters insurance. Fifth, injuries to employees (like a regular house cleaner) may be excluded, as they might require workers’ compensation insurance. Finally, some policies exclude specific high-risk activities or have special conditions for certain dog breeds. Knowing these exclusions prevents false expectations. For insights on how injury risk factors affect your premium, see our guide on renters insurance cost.

The Claims Process for an Injury Incident

If someone is injured in connection with your rental, follow these steps. First, ensure the injured person receives necessary medical attention. Second, document the incident. Take photos of the hazard that caused the injury (e.g., a wet floor, broken step) and get contact information for any witnesses. Third, be courteous but do not admit fault or make promises to pay for expenses. Simply express concern for their well-being. Fourth, contact your renters insurance company as soon as possible to report the incident. Provide them with all the facts. They will determine whether to handle it under Medical Payments (if bills are minor and fault is unclear) or under Liability coverage (if a serious injury where you may be at fault). An adjuster will be assigned to manage communications with the injured party and their insurer, working to resolve the claim within your policy limits.

How Insurers Handle Injury Claims

When you report an injury, the insurance adjuster’s role is to investigate and manage risk. For a MedPay claim, they will typically ask for copies of medical bills and reimburse the injured party directly, up to the MedPay limit, with minimal fuss. For a liability claim, the process is more involved. The adjuster will gather evidence, review medical records, and assess your legal liability. They will then negotiate with the injured person (or their attorney) to reach a settlement that avoids a lawsuit. If a lawsuit is filed, your insurer will provide and pay for your legal defense. The goal is to resolve the claim fairly while protecting your financial interests. Your cooperation is essential, but you should let the professionals handle negotiations. To find a policy with strong liability protection, use a comparison service like Tejribati. For expert advice, the Insurance Information Institute is a trusted resource.

Maximizing Your Protection Against Injury Claims

To ensure you have robust protection, take these steps. First, carry adequate liability limits. Given the high cost of healthcare, a limit of $300,000 to $500,000 is a wise minimum. Consider an umbrella policy for an extra $1 million or more in coverage. Second, maintain a safe home. Fix hazards promptly, ensure good lighting, clean up spills, and secure rugs. Third, understand your responsibilities under your lease for maintenance and repairs to avoid liability for negligence. Fourth, if you have a dog, disclose it to your insurer and ensure it is covered. Fifth, review your policy to understand the exact limits of your Medical Payments coverage. By being proactive, you reduce the risk of injuries and ensure your insurance is ready to respond effectively if an accident does occur.

Conclusion: A Critical Safety Net

So, does renters insurance cover injuries? Absolutely. It provides a dual-layer safety net through Medical Payments for minor, no-fault accidents and through substantial Liability coverage for serious injuries where you are at fault. This protection is fundamental, as the financial consequences of an injury lawsuit can be devastating. By understanding how these coverages work, maintaining a safe living environment, and carrying sufficient policy limits, you can rent with confidence. Your renters insurance does more than protect your stuff; it protects your financial future from the unpredictable costs of accidental injuries. Review your policy today to ensure your protection is adequate for your lifestyle.

Frequently Asked Questions (FAQ)

Does renters insurance cover my own injuries if I get hurt at home?

No. Renters insurance does not cover medical expenses for you or members of your household. For your own injuries, you must rely on your personal health insurance, disability insurance, or workers’ compensation if applicable.

If my dog bites someone, is that covered under the injury coverage?

Yes, dog bite injuries to others are typically covered under the liability portion of your renters insurance, subject to your policy’s terms and any breed-specific exclusions. Medical Payments may also cover initial minor bills.

What if a delivery person slips on my icy walkway and gets hurt?

This could be covered under both Medical Payments (for immediate bills) and Liability coverage (if you were negligent in failing to clear ice, as often required by local ordinance). Your insurer would investigate to determine liability.

Are injuries from a party at my house covered?

Yes, injuries to guests at a social gathering are generally covered. However, if you serve alcohol and a guest causes an accident after leaving, you could face “social host liability,” which may or may not be covered depending on state law and your policy. Check with your insurer.

How much medical payments coverage should I have?

A typical amount is $1,000 to $5,000. This is usually sufficient for minor injuries like sprains or stitches. The cost to increase this limit is minimal, so consider raising it to $5,000 for added peace of mind.

Does my landlord’s insurance cover injuries in my apartment?

The landlord’s insurance covers injuries caused by their negligence in maintaining common areas or the building’s structure. It does not cover injuries caused by your negligence or conditions within your rented unit. That is your responsibility, covered by your renters insurance.

Can I be sued even if I have renters insurance?

Yes, you can still be sued. However, if you have renters insurance, your insurer will provide a legal defense. If the lawsuit is covered, they will also pay any settlement or judgment up to your policy limits, protecting your personal assets.