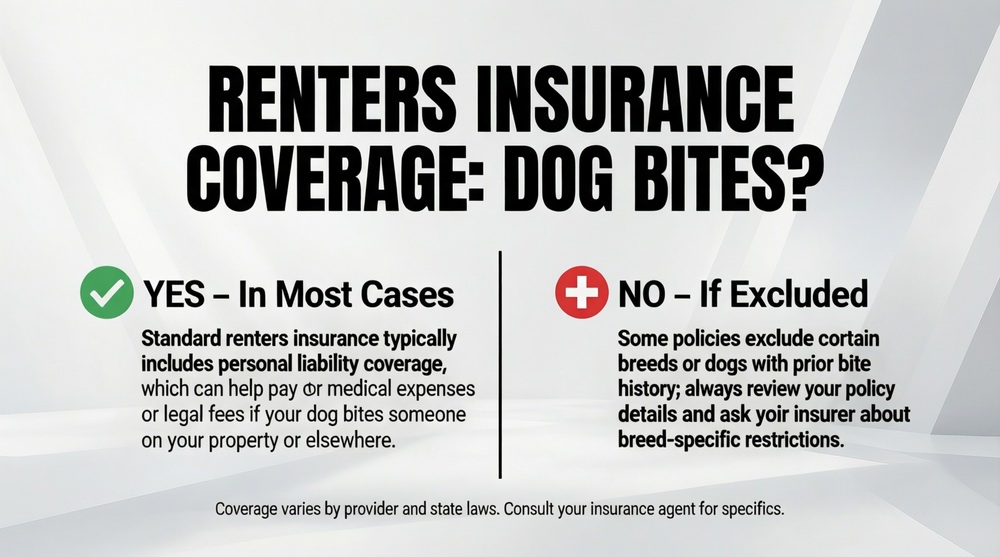

For millions of renters who are also pet owners, a critical question arises: does renters insurance cover dog bites? The good news is that, in most cases, the personal liability coverage within a standard renters insurance policy does provide protection if your dog bites someone or causes an injury. This coverage is essential, as a single dog bite incident can lead to tens of thousands of dollars in medical bills, legal fees, and potential lawsuits. However, coverage is not universal, and insurers have specific rules and exclusions, particularly regarding certain dog breeds or animals with a history of aggression. This guide will explain how dog bite liability coverage works under renters insurance, outline common restrictions, and provide steps you can take to ensure you and your pet are properly protected, giving you peace of mind as a responsible pet owner.

Understanding Dog Bite Liability Coverage

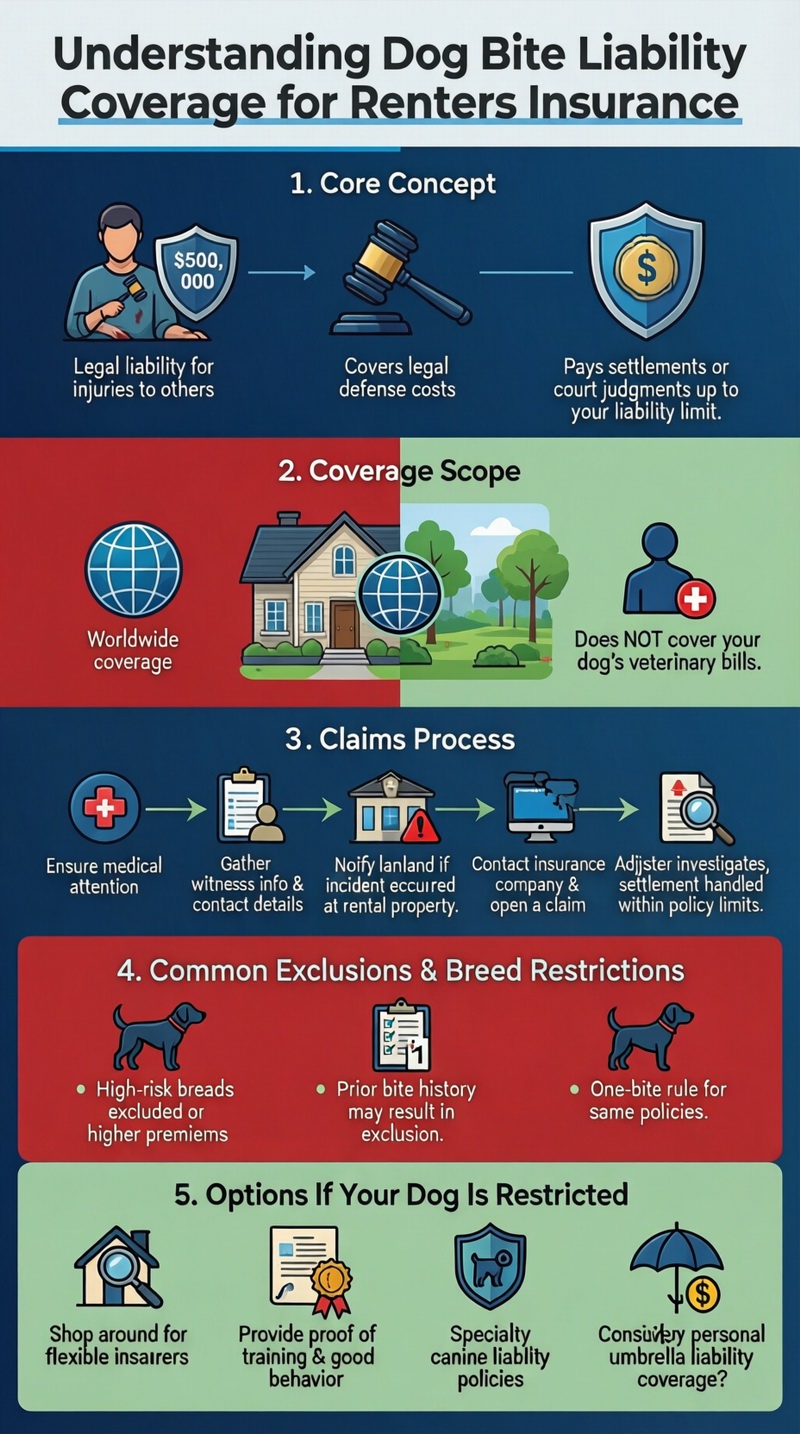

The core component that answers the question “does renters insurance cover dog bites?” is the personal liability coverage in your policy. This coverage is designed to protect you financially if you are found legally responsible for injuring another person or damaging their property. A dog bite is a common example of such an incident. If your dog bites a guest, a neighbor, or even someone outside your home, the injured party may seek compensation for medical expenses, lost wages, and pain and suffering. Your renters insurance liability coverage typically provides two key benefits: it pays for your legal defense costs, including attorney fees, and it pays for settlements or court-ordered judgments, up to the liability limit on your policy. This protection can prevent a single accident from devastating your personal finances. For a broader understanding of this protection, learn more about what renters insurance is.

How Coverage Applies Inside and Outside the Home

Dog bite liability coverage under renters insurance is not limited to incidents within your rented apartment or house. It generally provides “worldwide” coverage, meaning it can protect you if your dog bites someone at a park, on a walk, or while visiting another location. This is a crucial aspect, as dogs can act unpredictably in unfamiliar environments. The coverage responds regardless of where the incident occurs, as long as you are found legally liable. It is important to note that the coverage is for third-party liability; it does not cover veterinary bills if your own dog is injured—that would require a separate pet insurance policy. Understanding the extent of this coverage is a key part of evaluating your overall renters insurance coverage as a pet owner.

The Claims Process for a Dog Bite Incident

If your dog bites someone, taking the right steps is important for the well-being of the injured person and for your insurance claim. First, ensure the injured person receives appropriate medical attention. Be polite and cooperative but avoid making statements that could be construed as an admission of legal fault. Second, exchange contact information and gather details from any witnesses. Third, report the incident to your landlord if it occurred on the rental property. Fourth, contact your renters insurance company as soon as possible to report the incident. They will open a claim file and guide you through the process. An adjuster will investigate, which may involve speaking with the injured party, reviewing medical records, and assessing the circumstances. Your insurer’s goal is to settle the claim within your policy limits to avoid a lawsuit.

Common Exclusions and Breed Restrictions

While the answer to “does renters insurance cover dog bites?” is often yes, there are significant exclusions that can leave you without coverage. The most common is the “canine liability exclusion” or “dangerous dog exclusion.” Many insurance companies maintain a list of dog breeds they consider high-risk, and they may either refuse to issue a policy, exclude coverage for that specific dog, or charge a higher premium. Breeds commonly on restricted lists include Pit Bulls, Rottweilers, Doberman Pinschers, German Shepherds, Huskies, and Wolf hybrids. Furthermore, if your dog has a prior bite history, most insurers will exclude coverage for that animal. Some policies may have a “one-bite” rule, meaning they will cover the first incident but then exclude the dog or cancel the policy afterward. It is absolutely essential to disclose your pet’s breed and history when applying for insurance.

What to Do If Your Dog Breed is Restricted

If you own a dog breed that is commonly restricted, do not assume you have no options. First, shop around. Not all insurance companies use the same breed lists or underwriting guidelines. Some smaller or regional insurers may be more flexible. Second, you can provide documentation to demonstrate your dog’s good behavior, such as a Canine Good Citizen (CGC) certification from the American Kennel Club, completion of obedience training, or a letter from a veterinarian. This may help in some cases. Third, inquire about purchasing a separate canine liability policy or a personal umbrella liability policy, which might provide coverage where your base renters policy does not. Fourth, be prepared to sign a waiver or accept a higher premium. Being proactive and honest is the only way to secure legitimate coverage. For context on how pets can affect your policy’s pricing, see our guide on renters insurance cost.

Landlord Requirements and Lease Agreements

Your renters insurance is not the only policy to consider. Your lease agreement likely has clauses regarding pets. Many landlords require proof of renters insurance and may specifically require that the policy include liability coverage for dog bites. They may also have their own breed restrictions that are stricter than those of insurance companies. Violating your lease by having a prohibited breed or failing to maintain the required insurance could result in fines or even eviction. Always review your lease carefully and ensure your renters insurance meets both your needs and your landlord’s requirements. Open communication with your landlord about your pet and your coverage can prevent conflicts later.

Maximizing Your Protection as a Pet Owner

To ensure you are fully covered, take these proactive steps. First, always disclose that you have a dog when applying for or renewing renters insurance. Provide accurate information about the breed, age, and any past incidents. Second, choose a liability limit that provides adequate protection. Given the high cost of medical care and lawsuits, a limit of $300,000 to $500,000 is often recommended. Consider adding an umbrella policy for an extra $1 million in coverage. Third, take steps to minimize risk: properly train and socialize your dog, use a leash in public, securely fence your yard if applicable, and never leave children unattended with a dog. Fourth, keep records of your dog’s training and vaccinations. These steps not only reduce the chance of an incident but also demonstrate responsible ownership, which can be helpful if you ever need to file a claim or find a new insurer.

What If You Are Not Covered?

If you discover your renters insurance does not cover dog bites because of an exclusion, you are personally financially responsible for any incidents. This means you would have to pay out of pocket for medical bills, legal fees, and any settlements. This risk makes it imperative to find alternative coverage. Options include seeking a specialty insurer that covers your breed, purchasing a standalone canine liability policy, or exploring membership organizations that offer pet liability coverage. Do not take the risk of going without coverage. To compare renters insurance policies that are pet-friendly, use a service like Tejribati. For expert advice on this topic, the Insurance Information Institute provides valuable information that applies to renters as well.

Conclusion: Essential Protection for Responsible Owners

So, does renters insurance cover dog bites? For most responsible pet owners with dogs not on a restricted list and without a violent history, the answer is a clear yes, providing vital liability protection through a standard policy. This coverage is a financial lifeline that safeguards your assets and future. The key is full transparency with your insurer, understanding your policy’s specific terms and exclusions, and carrying sufficient liability limits. By taking responsibility for your pet’s behavior and securing the right insurance, you can enjoy the companionship of your dog with the confidence that you are protected against the unexpected. Review your policy today, talk to your agent about your pet, and ensure you have the peace of mind every pet-owning renter deserves.

Frequently Asked Questions (FAQ)

Are all dog breeds covered by renters insurance?

No. Many insurance companies exclude specific breeds they deem high-risk, such as Pit Bulls, Rottweilers, and others. You must disclose your dog’s breed when applying, and the insurer will confirm if coverage is provided or excluded.

What happens if I do not tell my insurance company I have a dog?

Failing to disclose a dog, especially a restricted breed, is a serious omission. If your dog later bites someone, the insurer can deny the claim for misrepresentation, leaving you personally liable for all costs. Always be honest about pet ownership.

Does renters insurance cover damage my dog does to my own property?

No. The personal property coverage in renters insurance does not cover damage your pet causes to your own belongings (e.g., chewing furniture). That is considered preventable damage and is excluded.

Will my premium go up if I file a dog bite claim?

It is very likely. Filing any liability claim can lead to a significant premium increase at renewal. In some cases, the insurer may choose not to renew your policy after a dog bite incident.

What if my dog bites another dog?

Your renters insurance liability coverage may apply if your dog injures another person’s pet, as this is considered damage to their property. Coverage would be subject to your policy limits and the same breed exclusions.

Can my landlord require me to have dog bite liability coverage?

Yes, many landlords include a clause in the lease requiring tenants with pets to carry renters insurance with a minimum amount of liability coverage, often $100,000 or more, specifically noting dog bite protection.

How can I prove my dog is not dangerous to an insurer?

You can provide documentation such as official obedience training certificates, the AKC Canine Good Citizen certificate, a letter from your veterinarian regarding temperament, or a history of no prior incidents.