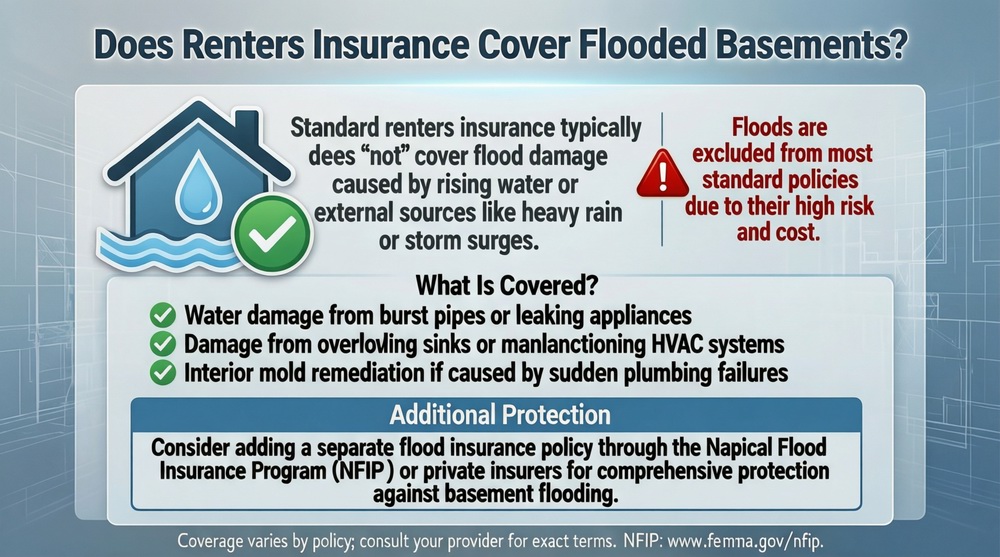

When asking “does renters insurance cover flooded basements?” the critical answer is: It depends on the source of the water. Standard renters insurance typically covers water damage from inside your rental unit (like a burst pipe or overflowing appliance) but explicitly excludes damage from external flooding (like heavy rain, overflowing rivers, or storm surge that seeps or flows into the basement). If your basement floods due to a sewer backup or sump pump failure, that is also usually excluded unless you have a specific endorsement. To be covered for true external flooding, you must purchase a separate flood insurance policy through the NFIP or a private insurer. This guide will clarify these distinctions and help you understand what renters insurance is designed to protect.

The Critical Distinction: Water Damage vs. Flood Damage

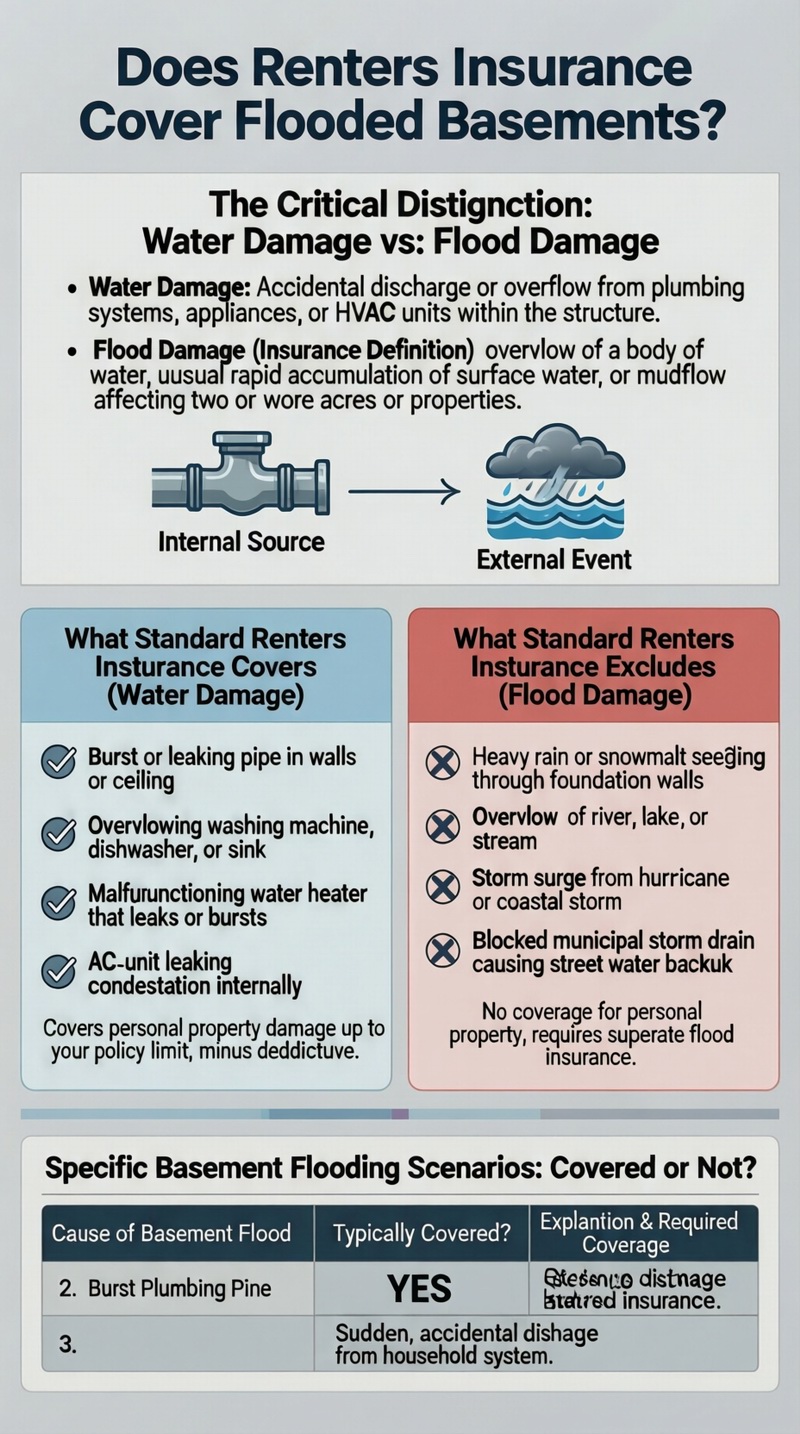

Insurance policies have very specific, legal definitions for the word “flood.” Understanding this definition is the first step in answering “does renters insurance cover flooded basements?” For insurance purposes, a flood is generally defined as an overflow of a body of water, unusual and rapid accumulation of surface water, or mudflow that affects two or more acres of normally dry land or two or more properties (one of which is yours). In contrast, water damage typically refers to accidental discharge or overflow from a plumbing system, appliance, or HVAC unit within the structure. This distinction means a basement flood caused by a torrential downpour overwhelming the ground is a “flood,” while a flood caused by a cracked water heater tank is “water damage.”

What Standard Renters Insurance Covers (Water Damage)

Your renters insurance personal property coverage will typically protect your belongings if the basement flood is caused by a covered “water damage” event. Common covered scenarios include:

– A burst or leaking pipe in the walls or ceiling.

– An overflowing washing machine, dishwasher, or sink.

– A malfunctioning water heater that leaks or bursts.

– An air conditioning unit that leaks condensation internally.

In these cases, the water originates from within the building’s systems. Your policy would cover the cost to repair or replace your damaged belongings (e.g., furniture, electronics, boxes of stored items) up to your personal property limit, minus your deductible.

What Standard Renters Insurance Excludes (Flood Damage)

The standard renters insurance policy (HO-4 form) contains a clear exclusion for “flood,” as defined above. This means if water enters your basement because of:

– Heavy rainfall or snowmelt saturating the ground and seeping through foundation walls.

– An overflowing river, lake, or stream.

– Storm surge from a hurricane or coastal storm.

– A blocked municipal storm drain causing street water to back up.

…then your renters insurance will NOT cover any damage to your personal property. The building structure is your landlord’s responsibility, but your belongings are your own financial loss without proper coverage.

Specific Basement Flooding Scenarios: Covered or Not?

Basement floods can happen in various ways. The following table breaks down common causes and whether a standard renters insurance policy is likely to provide coverage for your belongings. This is central to answering “does renters insurance cover flooded basements?” in practical terms. For more on standard protections, see our guide on renters insurance coverage.

| Cause of Basement Flood | Typically Covered by Renters Insurance? | Explanation & Required Coverage |

|---|---|---|

| Burst Plumbing Pipe | YES | Considered sudden, accidental water discharge from a household system. |

| Overflowing Washing Machine | YES | Water source is an appliance within the home, a covered peril. |

| Heavy Rain / Groundwater Seepage | NO | Defined as external flooding. Requires separate flood insurance. |

| Sewer or Drain Backup | NO (unless endorsed) | Usually excluded. Requires a water backup endorsement. |

| Sump Pump Failure | NO (unless endorsed) | Often excluded or limited. May be covered by a water backup or equipment breakdown endorsement. |

| Overflowing River or Stream | NO | The definitive example of a flood. Requires separate flood insurance. |

The Crucial Water Backup Endorsement

One of the most common and confusing basement flood causes is sewer or drain backup. This occurs when the municipal sewer system is overwhelmed (often during heavy rain) and waste water backs up into homes through floor drains or toilets. Standard renters insurance excludes this. However, for an additional premium (usually $50-$100 per year), you can add a Water Backup of Sewers and Drains endorsement. This add-on provides coverage for damage to your personal property from this specific cause. It is highly recommended for renters in homes with basements, older municipal systems, or areas prone to heavy rain.

What About Your Landlord’s Insurance?

A common misconception is that your landlord’s insurance will cover your belongings in a basement flood. This is false. Your landlord’s property insurance covers the physical structure of the building (drywall, flooring, built-in appliances). It does not extend to the personal property of tenants. Regardless of the water source, your belongings are only protected by your own renters insurance (if the cause is covered) or your separate flood insurance policy.

How to Get Coverage: Flood Insurance and Endorsements

Since the answer to “does renters insurance cover flooded basements?” is often “no” for external water, securing separate protection is essential if you are at risk. Flood insurance for renters is available and more affordable than many think. It is primarily purchased through the National Flood Insurance Program (NFIP), administered by FEMA, though private flood insurance options are growing. A renters flood insurance policy (called an “Contents Only” policy) covers your personal belongings against direct physical loss from flooding. Coverage limits up to $100,000 for contents are available through the NFIP. There is typically a 30-day waiting period from purchase before the policy goes into effect, so you cannot buy it last minute as a storm approaches.

Cost of Renters Flood Insurance

The cost depends on your flood risk, determined by your property’s location on FEMA’s Flood Insurance Rate Map (FIRM). For renters in low-to-moderate risk areas (Zone B, C, or X), a contents-only flood policy can cost as little as $100-$400 per year. In high-risk flood zones (Zone A or V), the cost will be higher but is still a fraction of the potential loss. Given the average flood claim is significant, this is a cost-effective form of protection for vulnerable belongings, especially those stored in basements or first-floor units. Consider this as part of your total renters insurance cost planning.

Steps to Protect Your Belongings in a Basement

1. Identify the Risk: Check your address on FEMA’s Flood Map Service Center to see your official flood zone.

2. Review Your Policy: Read your renters insurance policy to understand its water damage coverage and exclusions. Speak to your agent about adding a water backup endorsement.

3. Purchase Flood Insurance: If you are in any flood zone (even low risk), seriously consider an NFIP contents-only policy. Over 20% of flood claims come from outside high-risk areas.

4. Mitigate Loss: Store valuable items on shelves or in waterproof containers. Avoid keeping irreplaceable items or high-value electronics in a basement prone to moisture.

Navigating a Claim for a Flooded Basement

If your basement floods, taking the right steps immediately can protect your health and your financial claim.

Step 1: Ensure Safety. Do not enter a flooded basement if the water could be in contact with electrical outlets or appliances. Turn off the electricity at the breaker if it is safe to do so.

Step 2: Identify the Source. Try to determine where the water is coming from. This is critical for the claim. Is it clean water from a pipe? Dirty water from a floor drain? External water seeping through walls?

Step 3: Notify Your Landlord. Contact your landlord or property manager immediately. They are responsible for stopping the source (fixing a broken pipe) and mitigating damage to the structure.

Step 4: Document the Damage. Before cleaning up, take extensive photos and videos of the water level, the damaged belongings, and the apparent source. Create a list of all damaged items.

Step 5: Contact Your Insurance Company. File a claim with your renters insurance provider if you believe the cause is covered (e.g., burst pipe). If the cause is external flooding, you must file a claim with your flood insurance provider.

Step 6: Mitigate Further Damage. Once documented, move salvageable items to a dry area. Your policy requires you to take reasonable steps to prevent further loss.

Working with Adjusters for Different Claims

If you have both a water damage claim (covered) and flood damage (not covered), you may interact with two different adjusters. A renters insurance adjuster will assess damage from the covered internal source, while an NFIP-assigned adjuster will assess flood damage. Clear documentation separating what was damaged by which water source is vital. For authoritative information on flood risks, FEMA provides resources like their official flood insurance website.

Conclusion: Proactive Protection is Key

So, does renters insurance cover flooded basements? The nuanced truth is that it covers some causes but not the most common and destructive ones. Relying solely on a standard renters policy leaves you vulnerable to external flooding and sewer backups. The smart approach is to build a layered defense: 1) Maintain a robust renters insurance policy with replacement cost coverage and a water backup endorsement. 2) Evaluate your flood risk and purchase a separate NFIP flood insurance policy for your contents if there is any potential for external water intrusion. 3) Practice smart storage habits for items in basements or ground-floor units. By understanding these distinctions and taking proactive steps, you can ensure that a flooded basement is a manageable inconvenience rather than a financial catastrophe. Explore all renters insurance options and add-ons to build complete protection.

Frequently Asked Questions (FAQ)

If my landlord’s negligence causes a pipe to burst and flood my basement, am I covered?

Yes, your renters insurance should cover your damaged belongings in this scenario. The burst pipe is a covered water damage event, regardless of fault. Your insurer would pay to replace your property (minus your deductible) and would then potentially pursue subrogation against the landlord or their insurance to recover the costs if negligence can be proven. Your policy is designed to cover you for direct loss, not to depend on establishing liability first.

Does renters insurance cover the cost of a hotel if my basement apartment floods?

Yes, if the cause of the flood is a covered peril. The Loss of Use or Additional Living Expenses (ALE) coverage in your renters insurance will pay for reasonable extra costs (hotel, meals, laundry) if your rental unit is rendered uninhabitable by a covered event, like a burst pipe. However, if the flood is from an excluded cause like external groundwater, your ALE coverage would not apply unless you have a flood insurance policy that includes coverage for increased cost of living.

I live on the 3rd floor. Do I need to worry about flood insurance?

While your personal belongings are at lower direct risk from a ground-level flood, flood insurance can still be relevant. If the building’s ground floor floods, causing power outages, structural damage, or mold that forces evacuation, a contents-only flood policy could cover your belongings if they are damaged by the flood waters (e.g., water seeps up to the third floor) or cover your additional living expenses if you must relocate. The risk is lower but not zero. Evaluate based on the building’s overall flood risk.

What is the difference between “groundwater seepage” and a “pipe leak”?

This is the crux of many claim disputes. Groundwater seepage is water from the surrounding soil that slowly enters through cracks, walls, or floors due to hydrostatic pressure. It is considered flooding and is excluded. A pipe leak is water escaping from a pressurized plumbing system within the walls or under the slab. This is covered water damage. An adjuster will often look for signs of the source: seepage shows dampness along walls/floors, while a pipe leak may show a more concentrated origin point.

Can I get flood insurance if I rent an apartment in a high-risk flood zone?

Yes, and it is strongly advised. The NFIP cannot deny you a policy based on high risk. If your community participates in the NFIP, you are eligible to purchase a contents-only policy. The premium will be based on your building’s specific risk factors and the coverage amount you choose. Landlords in Special Flood Hazard Areas (SFHAs) with mortgages from federally regulated lenders are required to have flood insurance on the structure, but this does not cover your possessions.

How do I prove what was damaged in a basement flood for my claim?

Documentation is everything. If you have a pre-loss home inventory (photos/videos of your basement contents), that is ideal. After the flood, take clear, wide-angle photos and close-ups of all damaged items before discarding anything. Note make, model, age, and approximate value. For items without receipts, gather any proof of ownership (old photos, credit card statements, manuals). Keep samples of damaged materials (a piece of a ruined rug, a sodden book) until the adjuster has visited.

Does “mold remediation” for a flooded basement fall under renters insurance?

It depends on the source. If mold results from a covered water damage event (like a pipe leak that was promptly reported), your renters insurance may cover the cost to clean or replace mold-damaged belongings, as it’s a direct result of the covered peril. However, most policies limit or exclude mold damage that results from a long-term, neglected problem, poor maintenance, or from an excluded cause like external flooding. Coverage for the mold remediation itself on the building structure is the landlord’s responsibility.