Business renters insurance is not a standard policy but rather a crucial adaptation or extension of coverage needed when you operate a business from your rented residence. A typical personal renters insurance policy contains significant exclusions for business-related property and liability, leaving you dangerously exposed. To properly protect a home-based business, you generally have three paths: 1) Adding endorsements to your existing renters policy for limited business property and liability, 2) Purchasing an In-Home Business Policy (a more robust hybrid), or 3) Securing a standalone Business Owner’s Policy (BOP) for comprehensive commercial coverage. The right choice depends on the scale of your business, the value of your business property, whether clients visit your home, and your level of liability exposure. Understanding these options is critical to avoid claim denials and protect both your personal and business assets.

The Critical Gap: Why Personal Renters Insurance Isn’t Enough

Standard renters insurance is designed for personal, non-commercial activities. Its policies include specific exclusions that create immediate gaps when you start a business from home. Relying on it for business protection is a high-risk mistake that can lead to denied claims and financial ruin.

Common Business Exclusions in Personal Policies

Most personal renters insurance policies contain clauses such as:

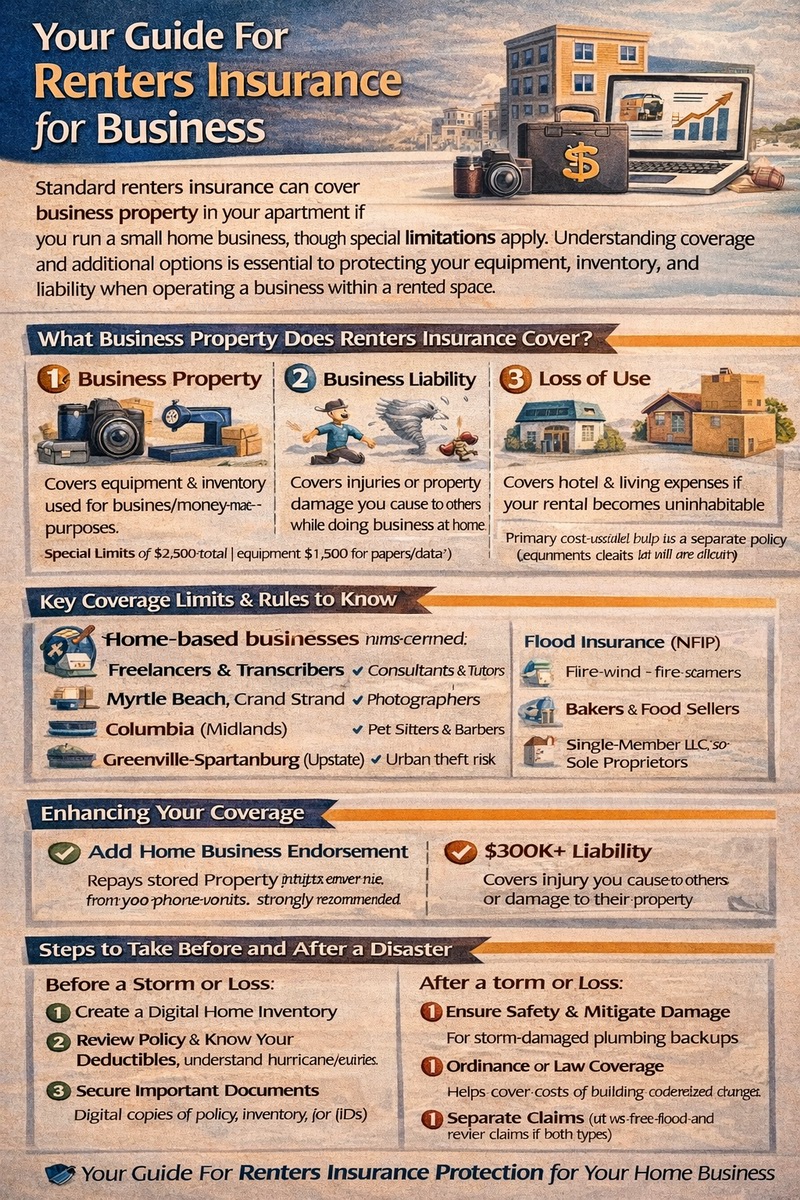

- Business Property Exclusion: Limits coverage for “business property” to a very low amount, often $2,500, and only for on-premises items. This is woefully inadequate if you have specialized equipment, inventory, or computers used primarily for work.

- Business Liability Exclusion: Excludes liability for injuries or damages “arising out of business pursuits.” If a client slips and falls during a consultation or a product you sell causes harm, you have no coverage.

- No Business Interruption Coverage: Does not cover lost income if a covered peril (like a fire) forces you to suspend business operations.

- No Professional Liability Coverage: Excludes errors, omissions, or negligence in the services or advice you provide (E&O or malpractice).

Simply using a personal laptop for freelance work might be overlooked, but once you have dedicated equipment, inventory, or client visits, you’ve likely exceeded the policy’s intent.

Consequences of Inadequate Coverage

If you file a claim for a business-related loss under a personal policy, the insurer can investigate. They may:

- Deny the claim entirely based on business exclusions.

- Pay only up to the minimal business property sub-limit (e.g., $2,500) for a loss worth $10,000.

- Cancel or non-renew your personal policy for material misrepresentation if you failed to disclose business activities.

This leaves you personally liable for replacing business assets and for any legal judgments against you.

Three Paths to Proper Business Renters Insurance

To bridge the gap, you must formally address your business exposure. The solution scales with the size and risk of your enterprise.

Option 1: Renters Insurance Endorsements (Riders)

For very small, low-risk, low-revenue businesses (e.g., a freelance writer with one computer, no clients on-site, no inventory), you might add endorsements to your existing policy.

- Business Property Endorsement: Increases the sub-limit for business property on-premises, perhaps to $10,000.

- Business Liability Endorsement: Adds a small amount of liability coverage for business activities, often with a separate limit.

Pros: Low cost, simple. Cons: Coverage is still limited, may not cover business interruption or professional liability. It’s a band-aid, not a cure. For details on standard policy structures, see our guide on renters insurance coverage.

Option 2: In-Home Business Policy

This is a specialized policy, often offered by the same company that provides your renters insurance, designed specifically for home-based businesses. It’s a middle-ground solution.

- Coverage: Typically combines broader business property coverage, business liability, loss of business income (interruption), and sometimes limited professional liability or coverage for data loss.

- Ideal For: Consultants, tutors, graphic designers, small online retailers with limited inventory, and others with moderate-value equipment and occasional client visits.

Pros: More comprehensive than endorsements, covers key business risks, often affordable. Cons: May have revenue or employee number limits. Not for businesses with significant inventory or high-risk operations.

Option 3: Standalone Business Owner’s Policy (BOP)

This is a commercial insurance package for small to medium-sized businesses, regardless of location. It’s the most comprehensive solution.

- Coverage: Bundles commercial property insurance (for your business assets, even at home), general liability insurance (for client injuries, product liability), and business interruption insurance. You can add professional liability, commercial auto, etc.

- Ideal For: Businesses with significant inventory, several employees, frequent client traffic, higher revenue, or those selling physical products. It separates your business insurance from your personal renters policy entirely.

Pros: Full, professional-grade coverage. Clearly defines and protects the business. Cons: Higher cost, more complex to purchase, requires maintaining two separate policies (renters and BOP).

| Solution | Best For | Typical Coverages Included | Cost Estimate (Annual) |

|---|---|---|---|

| Renters Policy + Endorsements | Micro-businesses, solo freelancers with minimal equipment & no client visits. | Increased business property limit, small business liability extension. | $50 – $200 added to renters premium |

| In-Home Business Policy | Established home-based businesses with equipment, some inventory, occasional clients. | Business property, liability, loss of income, sometimes professional liability. | $250 – $750+ |

| Business Owner’s Policy (BOP) | Businesses with significant operations, inventory, employees, or high liability risk. | Commercial property, general liability, business interruption. Add-ons available. | $500 – $2,500+ |

Key Coverages to Secure for Your Home-Based Business

Regardless of the path you choose, ensure your business renters insurance solution addresses these core commercial risks.

Business Personal Property

This covers your business assets: computers, printers, specialized tools, machinery, raw materials, and finished inventory. Ensure your limit reflects the full replacement cost of all items, both at your home and in transit. A standard renters policy’s $2,500 limit is almost always insufficient.

General Liability Insurance

This is non-negotiable if anyone interacts with your business. It covers:

- Bodily Injury: A client trips over a cord during a meeting in your home office.

- Property Damage: You accidentally damage a client’s property while on a service call.

- Advertising Injury: Libel, slander, or copyright infringement in your marketing.

Limits should start at $1 million per occurrence.

Business Income (Interruption) Insurance

If a fire damages your home office and you cannot work for two months, this coverage replaces your lost business income and helps pay ongoing expenses (like software subscriptions). It’s a lifeline that personal renters insurance completely lacks.

Professional Liability (Errors & Omissions)

If you provide services, advice, or designs, this covers financial losses your client suffers due to your mistakes, negligence, or failure to deliver. A graphic designer whose error causes a client’s website to crash, or a consultant whose bad advice leads to a financial loss, would need this coverage. It is excluded from general liability and most in-home policies unless added.

How to Assess Your Needs and Get Covered

Taking a structured approach will ensure you get the right level of business renters insurance without overpaying.

Step 1: Conduct a Business Risk Inventory

Ask yourself:

- What is the total value of my business equipment and inventory?

- Do clients, customers, or delivery personnel ever come to my home?

- Do I provide a service or advice that could lead to a professional liability claim?

- What would my monthly business expenses and lost income be if I had to shut down temporarily?

- Do I have business data that would be costly to recover?

The answers will point you toward the necessary coverages and policy type.

Step 2: Consult with an Insurance Professional

This is highly recommended. Speak with your current renters insurance agent first. Disclose the full nature of your business. They can explain what endorsements are available or if they offer an in-home business policy. For a BOP, you may need to work with a commercial insurance agent or broker who can shop the market. Be transparent about your operations to get accurate quotes.

Step 3: Compare Quotes and Policy Terms

When comparing, look beyond price:

- Coverage Limits & Sublimits: Are they adequate?

- Exclusions: What specific business activities are NOT covered?

- Deductibles: Per-claim deductibles for property and liability.

- Claims Process: How are business claims handled?

Remember, the cost of proper insurance is a necessary business expense, much like renters insurance cost is for your personal life. For authoritative guidance, the U.S. Small Business Administration (SBA) is an excellent resource.

Conclusion

Business renters insurance is not an optional upgrade; it’s a fundamental requirement for operating legally and safely from a rented home. Assuming your personal policy provides adequate coverage is a dangerous gamble. By assessing your risks—property, liability, income interruption, and professional exposure—you can choose the right solution, whether it’s a simple endorsement, a dedicated in-home policy, or a full Business Owner’s Policy. This proactive step separates savvy entrepreneurs from those vulnerable to a single disaster that could wipe out both their business and personal finances. Protect the venture you’ve built. Review your current renters insurance today, disclose your business activities to your agent, and secure the specialized protection your home-based enterprise truly needs.

Frequently Asked Questions (FAQ)

I just freelance occasionally. Do I really need business insurance?

If your freelance work is infrequent, uses minimal personal equipment, and generates very low income, you might be within the de minimis (trivial) allowance of your personal policy. However, the moment you invest in specialized equipment, dedicate a portion of your home as an office, or have even one client interaction at your home, you should at least inquire about an endorsement to formally cover your exposure. It’s better to have a small, defined coverage than a potential claim denial.

Does business renters insurance cover my car if I use it for deliveries?

No. Business use of your personal vehicle (like deliveries, ride-sharing, or client meetings) requires a commercial auto insurance endorsement on your personal auto policy or a separate commercial auto policy. Using your car for business without notifying your auto insurer can void your coverage in an accident.

What if I have employees who work from my rented home?

Having employees significantly increases your liability and likely requires a standalone Business Owner’s Policy (BOP). You will need to add Workers’ Compensation insurance (mandated by state law if you have employees) to cover work-related injuries. Your personal renters or in-home policy will not cover employee-related liabilities.

Is my business inventory covered if it’s stored in a separate storage unit?

Maybe, but you must specify this. An In-Home Business Policy or BOP can often be written to cover business property “on and off-premises,” including in a storage unit. A standard renters policy endorsement likely only covers property at your residence. Always clarify the location coverage with your agent.

How do I prove the value of my business property for insurance?

Maintain a detailed business inventory just as you would a home inventory. Keep receipts for all equipment and major purchases. For specialized equipment or inventory, consider an appraisal. For loss of income calculations, have 2-3 years of business tax returns and profit/loss statements ready to demonstrate your average earnings.

Can I write off business insurance premiums on my taxes?

Yes, typically. Premiums for insurance that protects your business (general liability, professional liability, business property, business interruption) are generally considered ordinary and necessary business expenses and are tax-deductible. Consult with a tax professional for guidance specific to your situation.

What happens if I don’t tell my renters insurer about my business?

You are committing material misrepresentation or concealment, which is grounds for your insurer to deny a claim (even a personal one), cancel your policy, or refuse to renew it. Honesty is the only safe policy when it comes to insurance.