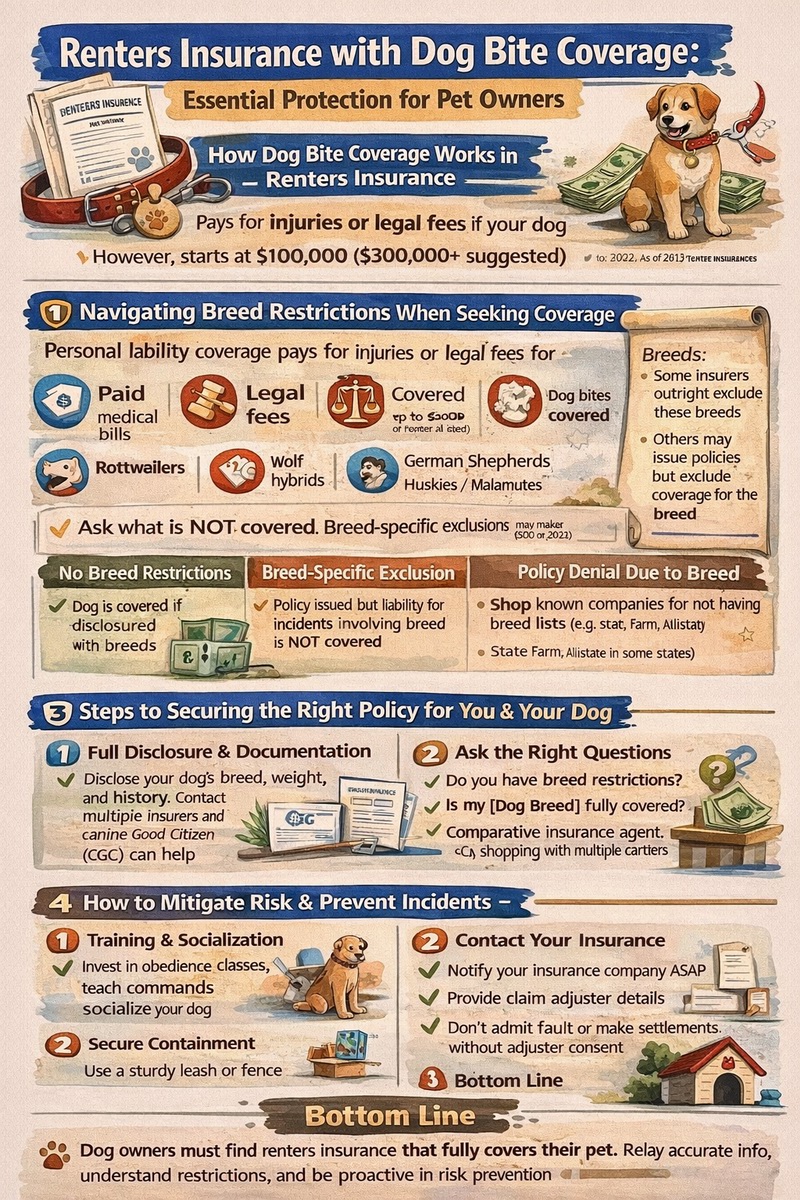

For renters with dogs, securing renters insurance with dog bite coverage is not just advisable—it’s a critical component of financial responsibility. Standard renters insurance policies typically include personal liability protection, which often extends to cover injuries or property damage caused by your dog, including bites. This coverage can pay for the injured person’s medical bills, legal fees, and settlements if you are found liable, protecting your savings and future income from a lawsuit. However, navigating this coverage requires careful attention: many insurers have breed restrictions, weight limits, or history requirements that can exclude certain dogs. Furthermore, some companies may outright deny coverage or require a separate animal liability policy. This guide will walk you through how to find and secure a policy that fully covers your canine companion, understand the limitations, and take steps to mitigate risk, ensuring you and your pet are protected in your rented home.

How Dog Bite Coverage Works in a Renters Policy

Dog bite coverage is generally not a separate policy but an integral part of the personal liability component (often called Coverage E) within a standard renters insurance policy. This section of your policy protects you financially if you are found legally responsible for causing bodily injury or property damage to others. Since dog bites fall under “bodily injury,” they are typically covered up to the liability limit you selected, which usually starts at $100,000 and can be increased to $500,000 or more. When an incident occurs, your insurance company would handle the claim, covering medical expenses, legal defense costs, and any court-awarded damages, minus your deductible if applicable to liability claims (though often liability coverage has no deductible). This system prevents a single incident from causing financial ruin.

The Role of Personal Liability Protection

Personal liability protection is the shield that renters insurance with dog bite coverage provides. It operates on the principle of negligence. If your dog bites someone and you are deemed legally liable—for example, because you failed to restrain the dog or knowingly took it into a prohibited area—your liability coverage activates. It’s important to note that coverage can vary by state due to differing “dog bite statutes.” Some states have a “strict liability” rule, where the owner is automatically liable for injuries regardless of the dog’s past behavior. Your renters insurance is designed to respond in these situations, making robust liability limits essential for dog owners.

Typical Coverage Scenarios and Limits

A renters insurance policy with adequate liability limits can cover a range of dog-related incidents:

- A bite on your property: A guest or service person is bitten in your apartment.

- A bite off your property: Your dog bites someone at a park or on a sidewalk during a walk.

- Property damage: Your dog knocks over a expensive sculpture at a friend’s house or damages a neighbor’s property.

The coverage applies worldwide, not just at your rental address. However, the financial protection is capped at your policy’s liability limit. Given that the average cost of a dog bite claim exceeds $50,000, opting for higher limits like $300,000 or $500,000 is a prudent decision for dog owners. For a full breakdown of liability and other protections, see our guide on renters insurance coverage.

Navigating Breed Restrictions and Insurance Exclusions

The most significant hurdle for renters seeking dog bite coverage is navigating insurer-specific restrictions. Many companies maintain lists of dog breeds they consider high-risk, which can lead to denied coverage, policy non-renewal, or liability exclusions. Understanding this landscape is crucial to avoid a dangerous gap in your protection.

Common Restricted Breeds and “Blacklists”

While lists vary, breeds frequently subject to restrictions or exclusions include Pit Bulls (and related breeds like Staffordshire Terriers), Rottweilers, Doberman Pinschers, German Shepherds, Huskies, Malamutes, Chow Chows, Presa Canarios, and Wolf hybrids. Some insurers may also have weight limits (e.g., no dogs over 80 lbs) regardless of breed. It’s vital to disclose your dog’s breed accurately when applying for a policy. Failure to do so can be considered material misrepresentation, giving the insurer grounds to deny a future claim or cancel your policy outright.

What “Excluded” or “Not Covered” Really Means

If your dog’s breed is on an insurer’s exclusion list, it can mean one of three things:

- Policy Denial: The company will refuse to sell you a renters policy at all.

- Liability Exclusion: They will sell you a policy, but with a specific endorsement that excludes liability for any injury or damage caused by your dog. This leaves you fully personally liable.

- Non-Renewal: They may discover you have a restricted breed after policy issuance (e.g., through a claim) and choose not to renew your policy when it expires.

Always ask point-blank: “Does this policy provide full liability coverage for my [Dog Breed]?” Get the answer in writing.

| Insurance Company Stance | What It Means for You | Your Action Steps |

|---|---|---|

| No Breed Restrictions | Dog is covered under standard liability, subject to the dog’s individual history. | Confirm in writing, still disclose breed, and consider higher liability limits. |

| Breed-Specific Exclusion | Policy is issued but liability for incidents involving that breed is NOT covered. | This is a critical gap. Seek a different insurer or a separate animal liability policy. |

| Mandatory Muzzle/Restraint Endorsement | Coverage is contingent on the dog being muzzled in public or restrained on your property. | Understand the exact terms; a violation could void coverage for a claim. |

| Policy Denial Due to Breed | You cannot purchase a standard renters policy from that company. | Shop with companies known for not having breed lists (e.g., State Farm, Allstate in some states). |

How to Find and Secure the Right Policy for Your Dog

Finding true renters insurance with dog bite coverage requires a strategic and transparent approach. Being proactive and shopping carefully can save you from the shock of a denied claim later. Follow these steps to ensure you obtain a policy that provides the protection you need.

Step 1: Full Disclosure and Documentation

Honesty is non-negotiable. When getting quotes, provide your dog’s exact breed(s), weight, age, and history. Be prepared to share records from obedience training classes or the Canine Good Citizen (CGC) certification, which can sometimes positively influence an insurer’s decision. Having this documentation ready demonstrates responsible ownership and can be a valuable asset during the application process.

Step 2: Shopping and Asking the Right Questions

Don’t just compare prices; compare coverage terms related to pets. Contact multiple insurers and ask these specific questions:

- “Do you have any breed or weight restrictions for dogs?”

- “Is my [Dog Breed] fully covered under the personal liability section?”

- “Are there any special endorsements or requirements for dog owners?”

- “Is there a limit on the number of dogs covered?”

- “Would a prior bite history affect my eligibility or coverage?”

Companies like State Farm and Allstate are often cited as being more flexible with breed restrictions, evaluating dogs on a case-by-case basis rather than using a banned list. Independent insurance agents can also be excellent resources as they can shop your case with multiple carriers.

Step 3: Considering Umbrella Insurance for Extended Protection

For dog owners, especially those with larger breeds or significant assets, a personal umbrella policy is a highly recommended supplement. This is a separate, affordable policy that provides an extra $1 million or more in liability coverage on top of your renters and auto insurance limits. If a severe dog bite claim exceeds your renters policy liability limit, the umbrella policy kicks in. It also often provides broader coverage. Securing an umbrella policy typically requires that your underlying renters insurance already provides dog bite coverage, so it builds on a solid foundation. Understanding the full renters insurance cost should include evaluating the value of adding an umbrella policy for comprehensive protection.

Mitigating Risk and Preventing Incidents

While having the right renters insurance with dog bite coverage is essential, proactive risk management is the first and best line of defense. Taking steps to prevent incidents not only keeps others safe but also helps you maintain coverage and avoid premium increases or non-renewal after a claim.

Training and Socialization

Formal obedience training and consistent socialization from puppyhood are among the most effective ways to reduce bite risk. A well-trained dog that is comfortable in various situations is less likely to react out of fear or anxiety. Earning the AKC’s Canine Good Citizen title is a recognized achievement that signals to insurers and landlords that your dog has mastered basic manners and can behave reliably in public.

Secure Containment and Responsible Supervision

Always ensure your dog is securely contained within your rental property, whether by a sturdy fence (if applicable) or kept leashed when outside. Never leave your dog unattended in a common area of an apartment building. When guests visit, assess their comfort level with dogs and consider crating or confining your dog to another room if necessary, especially during gatherings. Post clear signage if your dog is on the property, as this can affect liability in some jurisdictions.

Understanding Local Laws and Leash Ordinances

Comply with all local animal control laws, including licensing, vaccination (especially rabies), and leash requirements. Violating a leash law can be used as evidence of negligence in a liability lawsuit, potentially complicating your insurance claim. Stay informed about your rights and responsibilities as a dog owner by checking resources like your local municipality’s website or the American Veterinary Medical Association.

What to Do If Your Dog Bites Someone

Despite best efforts, incidents can happen. Knowing the correct procedure is vital to manage the situation legally, medically, and in terms of your insurance coverage.

Immediate Actions Post-Incident

1. Secure Your Dog: Immediately remove your dog from the situation and confine it.

2. Assist the Victim: Offer first aid and, if the injury is serious, call for emergency medical assistance. Be courteous and concerned but avoid making statements that could be construed as an admission of legal liability, such as “My dog has never done this before!” or “This is all my fault.”

3. Exchange Information: Provide your name and contact information to the victim. Obtain their contact information as well.

4. Document the Scene: Take photos of the location and any relevant conditions.

Notifying Your Insurance Company and Managing the Claim

Contact your insurance company or agent to report the incident as soon as possible, even if the injury seems minor. Medical complications can arise later, and early reporting is a requirement of your policy. Provide the facts objectively. The insurer will assign a claims adjuster who will investigate, communicate with the injured party (or their attorney), and manage the settlement process. Do not agree to pay any expenses or sign any agreements without consulting your adjuster. Your cooperation is essential for the claim to be handled effectively under your renters insurance with dog bite coverage.

Conclusion

For a renter with a dog, a standard insurance policy is not enough—you need confirmed renters insurance with dog bite coverage. This protection is a fundamental part of responsible pet ownership, shielding you from potentially catastrophic financial loss. The journey involves careful shopping, full transparency about your pet, understanding and navigating breed restrictions, and choosing liability limits that reflect the real-world costs of an incident. By pairing this financial safety net with proactive training and responsible pet management, you create a comprehensive strategy for safety and security. Don’t wait for an incident to discover a gap in your policy. Review your current renters insurance today, ask the critical questions, and secure the peace of mind that comes from knowing both your home and your best friend are properly protected.

Frequently Asked Questions (FAQ)

Does renters insurance automatically cover dog bites?

In most cases, yes, standard renters insurance includes personal liability coverage that typically extends to dog bites. However, it is not “automatic” in the sense that many insurers have exclusions for specific breeds or dogs with a prior bite history. You must verify with your specific company that your dog is covered under the policy’s terms.

What dog breeds are most commonly excluded from coverage?

While lists vary by insurer, breeds frequently facing restrictions or exclusions include Pit Bulls, Rottweilers, Doberman Pinschers, German Shepherds, Huskies, Alaskan Malamutes, Chow Chows, Presa Canarios, and Wolf hybrids. It is essential to ask your insurer for their specific list before purchasing a policy.

Will my insurance cover my dog if it has bitten before?

This is a complex situation. If your dog has a documented bite history, you are legally obligated to disclose it when applying for insurance. Most standard insurers will likely deny coverage or exclude the dog from liability protection. In this case, you may need to seek a separate animal liability policy or inquire about surplus lines insurance, which is more expensive but designed for high-risk cases.

Can my landlord require me to have dog bite insurance?

Yes, absolutely. Many landlords and property management companies include clauses in the lease requiring tenants with dogs to carry renters insurance with a minimum liability limit (e.g., $300,000) and to provide proof that the dog is covered. They may also require you to name them as an “additional interested party” on the policy so they are notified of any changes or cancellations.

Is there a difference between “one-bite” states and strict liability states?

Yes, and it affects your liability. In a “strict liability” state, a dog owner is generally liable for injuries caused by their dog, even if the dog had never bitten before and the owner had no reason to believe it was dangerous. In a “one-bite” state (a simplification of negligence-based rules), the owner might not be liable for the first bite unless they knew the dog was dangerous. Your renters insurance is designed to respond in both scenarios, but the legal path to proving liability differs.

What if my dog damages my own property or my landlord’s property?

Damage your dog causes to your own personal property (like chewing your sofa) is typically not covered by renters insurance, as policies exclude damage caused by pets. Damage to the landlord’s property (like chewing the door frame or flooring) is also generally not covered under your policy; that is the landlord’s responsibility to repair, though they may deduct the cost from your security deposit or seek reimbursement from you personally.

How can I lower my premium as a dog owner?

While having a dog may affect your eligibility more than your premium, you can lower costs by: 1) Shopping with companies that don’t penalize your specific breed, 2) Choosing a higher deductible for personal property claims, 3) Bundling with auto insurance, and 4) Maintaining a claims-free history. Providing certificates for obedience training may also help in some cases.