The answer to “does renters insurance cover power surges?” is nuanced. Standard renters insurance typically provides limited or no coverage for power surge damage to the actual appliances and electronics that were fried. Most policies exclude damage to the “electrical apparatus” itself (like your TV, computer, or refrigerator) if the surge originates off your premises (e.g., from the utility grid). However, if the power surge is caused by a covered peril like a lightning strike directly to your home, the resulting damage to your belongings is usually covered. To get meaningful protection for surge damage, you often need to add an optional “equipment breakdown” endorsement or a specific “surge protector” endorsement, or rely on separate manufacturer/extended warranties. For foundational knowledge, start with our guide on what renters insurance is.

How Standard Renters Insurance Addresses Power Surges

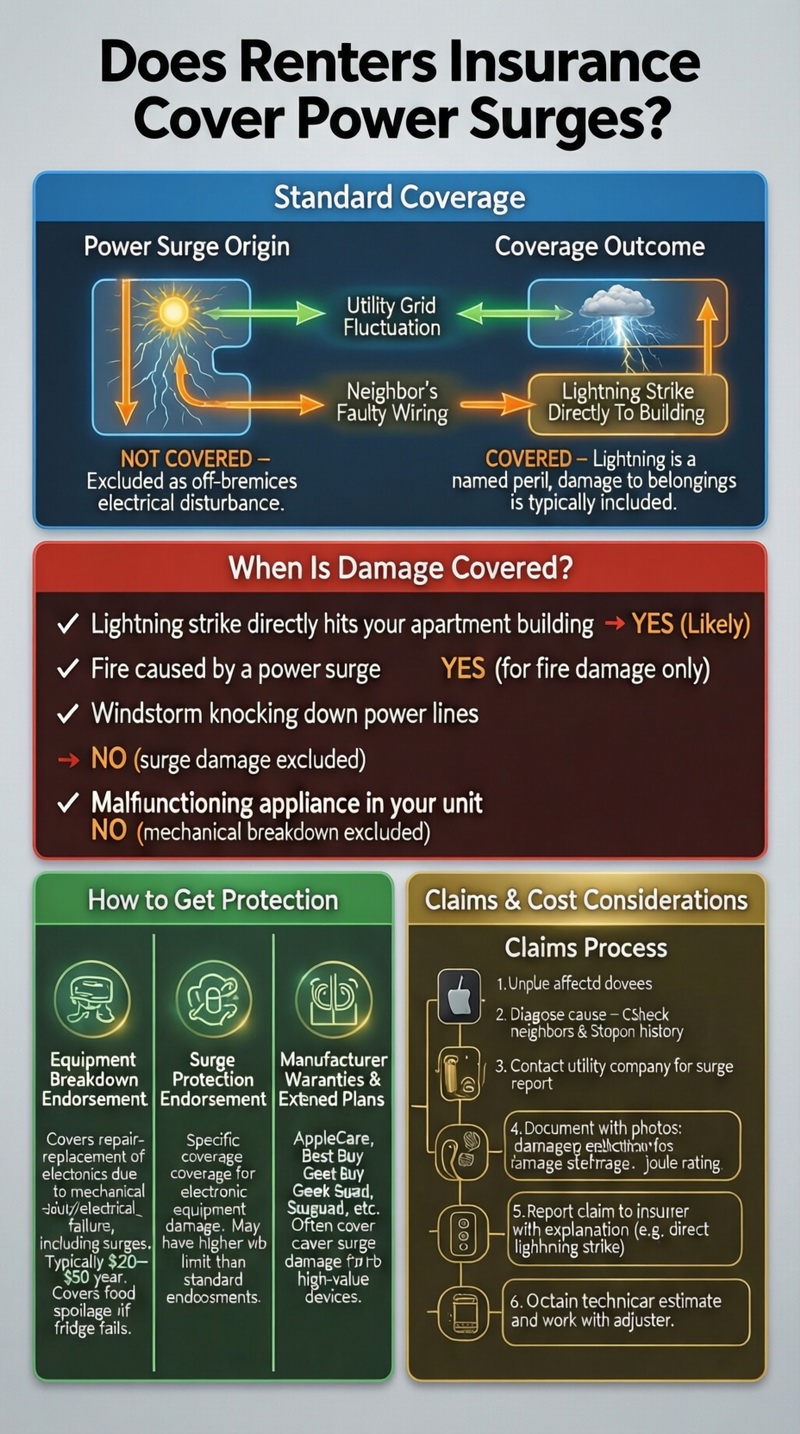

Standard renters insurance (HO-4) is a “named perils” policy. When evaluating “does renters insurance cover power surges?”, you must look for the specific perils listed. The relevant peril is often worded as: “Sudden and accidental damage from artificially generated electrical current.” This sounds promising, but the devil is in the exclusions and interpretations that follow in the policy fine print.

The Typical Exclusion for “Electrical Apparatus”

Most policies include an exclusion that states coverage does not apply to loss caused by artificially generated electrical current to “electrical appliances, devices, wiring, or components.” This means if a surge from the street fries your smart TV’s motherboard, the TV itself is not covered. The intent is to exclude wear and tear, mechanical breakdown, and grid-related surges, which are considered utility or maintenance issues. This is a key detail in understanding your renters insurance coverage limits.

When Power Surges ARE Covered: The Lightning Exception

Coverage often applies if the power surge is the direct result of a covered peril. Lightning is a named peril. Therefore:

– If lightning strikes a power line near your home and causes a surge that destroys your gaming console, the damage is likely excluded (surge from off-premises).

– If lightning directly strikes your building and the massive electrical surge fries everything plugged in, that damage is more likely to be covered because the lightning (the covered cause) happened on your premises.

Proving the origin can be difficult for claims adjusters.

Coverage Scenarios: What’s Protected and What’s Not

The following table clarifies how different types of power surge incidents are typically handled, answering “does renters insurance cover power surges?” in practical situations.

| Cause of Power Surge / Damage | Typically Covered by Standard Policy? | Explanation & Required Coverage |

|---|---|---|

| Lightning strike directly hits your apartment building. | YES (Likely) | Lightning is a covered peril. The resultant surge is considered part of the lightning damage. |

| Utility company grid fluctuation (brownout/surge). | NO | Excluded as off-premises electrical disturbance. Consider a warranty or equipment breakdown coverage. |

| Surge from a neighbor’s faulty wiring. | NO | Considered an off-premises electrical issue, even if originating next door. |

| Fire caused by a power surge. | YES (for fire damage) | Fire is a covered peril. Your policy would cover items burned in the fire, but not items only damaged by the surge that didn’t catch fire. |

| Power surge after a windstorm knocks down lines. | NO (for surge damage) | While wind is covered, the subsequent surge is often excluded. The wind damage to the building is covered; your fried electronics are not. |

| Surge from a malfunctioning appliance in your unit. | NO | Mechanical/electrical breakdown of an appliance is excluded. Equipment breakdown endorsement may help. |

Additional Living Expenses (ALE) for Surge-Related Issues

If a covered peril (like a lightning-caused fire) makes your home uninhabitable, your ALE coverage would pay for a hotel. However, if a simple power surge knocks out your electricity but causes no other covered damage, ALE does not apply because the home itself is not damaged, just inconvenienced.

How to Get Coverage: Endorsements and External Solutions

Since standard coverage is lacking, proactive steps are necessary to protect your electronics.

1. Equipment Breakdown Coverage Endorsement

This is the most effective add-on. Often called “boiler and machinery” coverage, it can be added to your renters policy for an additional premium (usually $20-$50/year). It covers the repair or replacement of home systems and appliances (including personal electronics) that break down due to mechanical or electrical failure, including power surges. It often includes coverage for food spoilage if your refrigerator fails. This endorsement essentially fills the “mechanical/electrical breakdown” exclusion gap.

2. Specific “Surge Protection” Endorsements

Some insurers offer a specific endorsement for power surge damage to electronic equipment. This may have a separate, higher sub-limit than what’s available under standard or equipment breakdown coverage. Ask your agent if this is available.

3. Manufacturer Warranties and Extended Protection Plans

For high-value electronics, the manufacturer’s warranty or a retailer’s extended service plan (like AppleCare or Best Buy’s Geek Squad Protection) often covers power surge damage. These can be more comprehensive for individual items than an insurance endorsement.

4. High-Quality Surge Protectors (Prevention)

Invest in UL-listed surge protectors with a high joule rating (over 2,000) for valuable electronics. For whole-home protection, consider asking your landlord about installing a surge protection device at the electrical panel. Prevention is the most cost-effective strategy.

The Claims Process for Suspected Surge Damage

If you believe you have a covered claim (e.g., from lightning), follow these steps:

1. Unplug Affected Devices: Prevent further damage.

2. Diagnose the Cause: Check if neighbors experienced the same issue. Was there a storm with visible lightning?

3. Contact Your Utility Company: Report the surge. They may provide a report or confirmation, which can help your claim.

4. Document Everything: Take photos of damaged electronics, any visible damage to outlets, and the surge protectors (note their joule rating). Keep the damaged items.

5. Contact Your Insurance Company: Report the claim. Be prepared to explain why you believe the cause is covered (e.g., direct lightning strike).

6. Get Repair Estimates: For repairable items, get a diagnosis and estimate from a qualified technician.

7. Work with the Adjuster: They will investigate to determine if the cause falls under a covered peril or is excluded.

Cost Considerations and Is Extra Coverage Worth It?

The cost of adding equipment breakdown coverage is minimal compared to the value of modern electronics. Given that the average household has thousands of dollars in susceptible devices (TVs, computers, gaming systems, smart home hubs, kitchen appliances), the endorsement is generally a wise investment. It transforms your policy from one that largely excludes surge damage to one that actively covers it. Consider this as part of your overall renters insurance cost and protection strategy. For a full review, explore all renters insurance options.

Conclusion: Assume You’re Not Covered, Then Get Covered

In summary, does renters insurance cover power surges? Not reliably under the standard policy. You should operate under the assumption that damage from a typical grid surge is excluded. To secure true protection, you have two main paths: 1) Add an equipment breakdown endorsement to your renters policy, or 2) Rely on manufacturer warranties and high-quality surge protectors for your most valuable items. The combination of physical surge protection and the right insurance endorsement is the best defense against the silent killer of electronics. Review your policy today, call your insurer to ask about adding equipment breakdown coverage, and safeguard your digital life.

Frequently Asked Questions (FAQ)

Does renters insurance cover a fried circuit board in my refrigerator?

Not under a standard policy. A surge that damages the refrigerator’s internal electronics is considered an electrical apparatus failure and is excluded. If you have an equipment breakdown endorsement, it would likely cover the repair or replacement of the fridge.

What about power strips/surge protectors? Does insurance cover if they fail?

The surge protector itself is not covered if it burns out. However, a high-quality surge protector is your first line of defense. Some premium surge protectors come with a connected equipment warranty that will reimburse you for devices damaged while properly plugged into them, even if your renters insurance doesn’t.

If a surge damages my home’s wiring, am I covered?

No. Damage to the building’s electrical wiring, outlets, or circuit breakers is considered part of the structure and is the landlord’s responsibility to repair under their property insurance. Your renters insurance only covers your personal property, not the dwelling.

Does “off-premises” coverage protect my laptop if a surge damages it at a coffee shop?

No. The off-premises coverage extends theft and other perils, but the same exclusions for electrical apparatus damage apply. If a surge at a coffee shop fries your laptop, your renters insurance is unlikely to cover it unless you have very specific and rare endorsements.

Will filing a claim for lightning surge damage raise my premium?

It might, as filing any claim can affect your risk profile. However, a claim stemming from a catastrophic event like a direct lightning strike may be viewed differently than a smaller, more frequent type of claim. Always weigh the claim amount against your deductible and potential future premium increases.

How can I prove the surge was caused by lightning?

It’s challenging. Evidence can include: a weather service report of lightning in your area at the exact time, visible damage to the building (a scorch mark, damaged roof), simultaneous failure of multiple unrelated appliances, and a report from an electrician diagnosing the cause as a high-voltage surge consistent with lightning.

Where can I find more information on protecting electronics?

For expert advice on surge protection and electrical safety, the Electrical Safety Foundation International (ESFI) guide to surge protectors provides excellent, non-commercial information on choosing and using surge protection effectively.