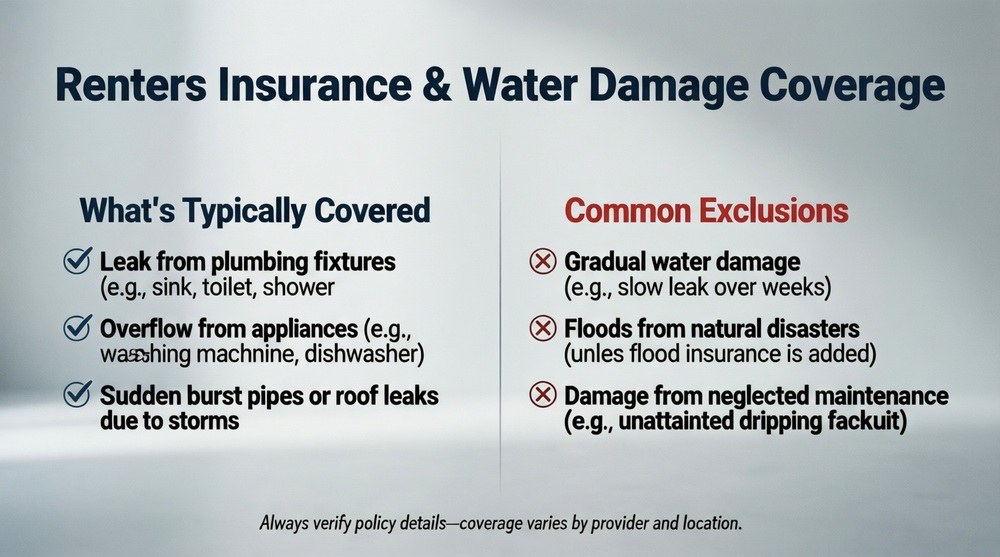

The answer to “does renters insurance cover water damage?” is a definitive “it depends on the source.” Standard renters insurance does cover sudden and accidental water damage that originates inside your rental unit, such as from a burst pipe, overflowing washing machine, or a leaking water heater. However, it does not cover water that comes from outside or below ground, including floods, sewer backups (unless you add an endorsement), and groundwater seepage. The key is the peril: internal plumbing issues are usually covered; external flooding is not. Understanding this distinction is essential for every renter. For a broader understanding, start with our guide on what renters insurance is.

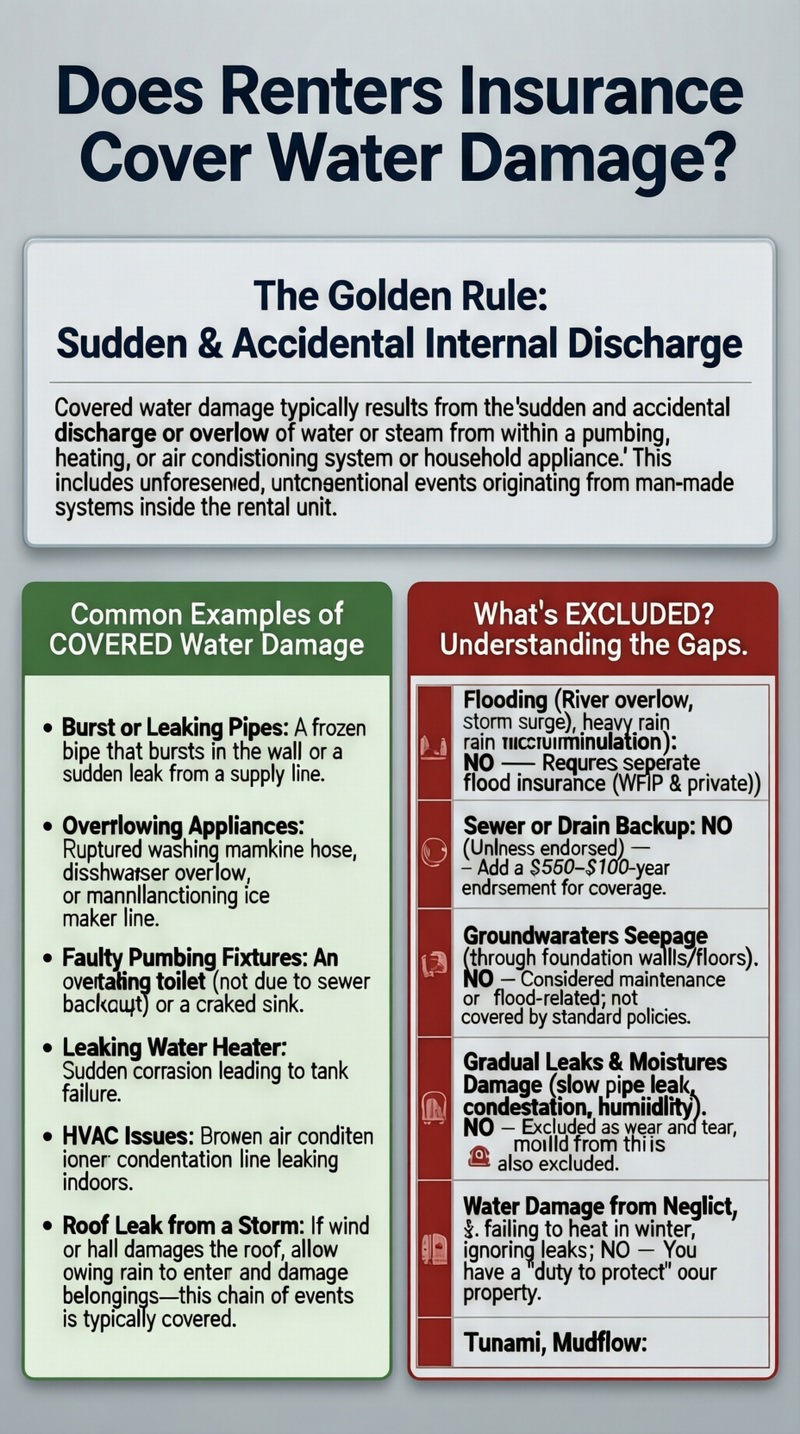

The Golden Rule: Sudden & Accidental Internal Discharge

When evaluating “does renters insurance cover water damage,” insurers apply a specific standard. Covered water damage typically results from the “sudden and accidental discharge or overflow of water or steam from within a plumbing, heating, or air conditioning system or household appliance.” This language in your policy (the HO-4 form) is your guide. The event must be unforeseen, unintentional, and originate from a man-made system within the building’s interior. Damage from a slow, hidden leak that festered for months is often denied, as it’s considered a maintenance issue.

Common Examples of COVERED Water Damage

Your personal property coverage (Coverage C) will typically protect your belongings if damaged by:

– Burst or Leaking Pipes: A frozen pipe that bursts in the wall, or a pipe that suddenly springs a leak.

– Overflowing Appliances: A washing machine hose that ruptures, a dishwasher that overflows, or a malfunctioning ice maker line.

– Faulty Plumbing Fixtures: An overflowing toilet (if not due to a sewer backup) or a cracked sink.

– Leaking Water Heater: A tank that corrodes and leaks suddenly.

– HVAC Issues: A broken air conditioner condensation line that leaks inside.

– Roof Leak from a Storm: If wind or hail (covered perils) damages the roof, allowing rain to enter and damage your belongings, that chain of events is typically covered.

This is a core part of your renters insurance coverage.

What’s the Landlord’s Responsibility vs. Yours?

It’s critical to separate property responsibilities. Your landlord’s insurance covers the structure (repairing the broken pipe, damaged drywall, and flooring). Your renters insurance covers your personal property (your ruined sofa, books, electronics) and may provide Additional Living Expenses (ALE) if you need to temporarily relocate. You are responsible for mitigating damage (e.g., moving belongings out of water).

What Water Damage is EXCLUDED? Understanding the Gaps

Renters insurance is not all-risk. Major exclusions exist to answer the other side of “does renters insurance cover water damage?” The most significant exclusions involve water entering the home from outside or below ground level.

| Type of Water Damage / Source | Typically Covered? | Detailed Explanation & Solutions |

|---|---|---|

| Flooding (River overflow, storm surge, heavy rain accumulation) | NO | Definition is key: Flood is an excess of water on normally dry land affecting two or more properties. Requires a separate flood insurance policy from the NFIP or a private insurer. |

| Sewer or Drain Backup | NO (unless endorsed) | Often excluded. Can be added for an extra $50-$100/year with a “Water Backup of Sewers and Drains” endorsement. Highly recommended for basement/ground-floor units. |

| Groundwater Seepage (Water seeping through foundation walls/floors) | NO | Considered a flood-related or maintenance issue. Not covered by renters or standard flood policies in many cases. Proper grading and drainage are preventive measures. |

| Gradual Leaks & Moisture Damage (Slow pipe leak, condensation, humidity) | NO | Excluded as “wear and tear, deterioration, or maintenance.” Mold resulting from this is also excluded. Promptly report any signs of moisture to your landlord. |

| Water Damage from Neglect (Failing to heat in winter, ignoring a known leak) | NO | You have a “duty to protect” your property. Neglect can lead to claim denial. |

| Tsunami, Mudflow | NO | Generally covered only under specific flood policies or separate riders. |

The Crucial Water Backup Endorsement

This add-on is one of the most valuable for renters. Sewer backups often occur during heavy rains when municipal systems are overwhelmed. The resulting water is unsanitary and can cause extensive damage. A standard policy won’t cover it, but for a relatively small annual fee, the endorsement provides specific coverage for this peril. If you have a unit below grade (like a basement apartment), this is practically essential.

Navigating a Water Damage Claim: Step-by-Step

If you experience water damage, swift and correct action is vital to protect your belongings and your claim.

1. Stop the Source & Ensure Safety: If safe to do so, turn off the water main or stop the appliance. Avoid electrical hazards from standing water.

2. Notify Your Landlord Immediately: They are responsible for repairing the source (the broken pipe, appliance, etc.). Document your communication.

3. Mitigate Further Damage: Move undamaged items to a dry area. Remove standing water if possible. This is a requirement in your policy.

4. Document Everything Thoroughly: Take extensive photos and videos of the water source, the damaged areas, and all affected belongings before you start cleaning up.

5. Create a Detailed Inventory: List every damaged item, including description, age, and estimated value. A pre-existing home inventory is invaluable here.

6. Contact Your Renters Insurance Company: File the claim promptly, providing your documentation. Be clear about the source of the water.

7. Work with the Adjuster: They will determine if the cause is a covered peril and assess the damage. Keep damaged items until they are inspected.

8. Secure Temporary Housing if Needed: If the unit is uninhabitable, your ALE coverage will pay for a hotel and extra living expenses. Keep all receipts.

Actual Cash Value vs. Replacement Cost in Water Claims

Water can ruin items completely. If you have Actual Cash Value (ACV), you’ll be paid the depreciated value of your waterlogged 5-year-old laptop—maybe $100. With Replacement Cost Value (RCV), you’d be paid enough to buy a new, comparable laptop—$800 or more. RCV coverage is highly recommended and significantly impacts your financial recovery.

Prevention and Proactive Protection

The best claim is the one you never file. To reduce risk:

– Know the location of your unit’s water shut-off valve.

– Inspect appliance hoses regularly and replace them every 5-7 years.

– Don’t pour grease down drains and use drain catchers to prevent clogs.

– Keep valuables and electronics off basement floors.

– Consider water leak sensors or a smart water shut-off system for early detection.

Also, review your policy’s specifics. Understand your renters insurance cost and what endorsements you have. Ensure you have the water backup endorsement if you’re at risk, and seriously consider flood insurance if you’re in a flood zone (or even a moderate-risk area—over 20% of flood claims are outside high-risk zones). For a comprehensive look at policies, explore all renters insurance options.

Conclusion: Knowledge is Your Best Defense

So, does renters insurance cover water damage? Yes, for the sudden, internal accidents that are common in rental homes. But no, for the external forces of nature like floods. The difference is not just semantic—it’s financial. By understanding your policy’s covered perils, adding the vital water backup endorsement, and considering separate flood insurance where appropriate, you build a layered defense against water-related financial losses. Remember, when in doubt, document the source and contact your insurer. With the right knowledge and coverage, you can navigate water damage without drowning in unexpected costs.

Frequently Asked Questions (FAQ)

Does renters insurance cover water damage from a leaky roof?

It depends on what caused the roof to leak. If a covered peril like wind or hail damages the roof, allowing rain to enter, the resulting water damage to your belongings is typically covered. If the leak is due to worn-out shingles or general deterioration (a maintenance issue), the water damage to your property is likely excluded. The landlord is responsible for roof maintenance.

What if the water damage comes from the apartment above me?

You are still covered under your own renters insurance policy. It doesn’t matter where in the building the water originated; if the water damage to your belongings results from a covered peril (like a burst pipe in your neighbor’s unit), your policy should respond. Your insurer may later seek reimbursement from the at-fault party’s insurance (subrogation).

Does renters insurance cover mold caused by water damage?

Only in very specific circumstances. Mold remediation is typically excluded if the mold results from long-term humidity, condensation, or gradual leaks. However, if mold is a direct result of a covered water loss (like water from a sudden burst pipe that wasn’t properly dried), some policies may cover a limited amount for mold removal (e.g., $5,000). Check your policy limits.

Are my belongings covered if they’re damaged by fire sprinklers?

Yes. Accidental discharge from a fire sprinkler system is a covered peril under standard renters insurance policies. If a sprinkler goes off due to a fire, high heat, or even a malfunction, the water damage to your belongings is covered.

What’s the difference between “flood” and “water backup”?

Flood is water coming from the outside, over the ground, and into your home (e.g., river overflow). Water backup is when water or sewage backs up through sewers or drains from inside the municipal system or your building’s plumbing. They are different perils, often both excluded, and require different add-ons (flood insurance vs. water backup endorsement).

Does renters insurance cover the cost to repair the actual pipe or appliance that leaked?

No. Renters insurance covers your personal property, not the structure or fixtures of the building. Repairing the burst pipe, faulty washing machine, or leaky water heater is the responsibility of your landlord (if it’s their appliance) or possibly you if it’s an appliance you own.

Where can I find official information on flood risks and insurance?

For authoritative information on flood insurance and understanding your risk, the official FEMA National Flood Insurance Program (NFIP) website is the primary source. It provides flood maps, policy details, and guidance on obtaining coverage, which is essential for understanding the part of water damage that renters insurance does not cover.