Yes, absolutely. Renters insurance does cover fire damage comprehensively. It is one of the fundamental perils listed in every standard renters insurance policy (HO-4 form). This coverage extends to three critical areas: 1) Personal Property: It pays to repair or replace your belongings (furniture, clothes, electronics) damaged or destroyed by fire or smoke. 2) Additional Living Expenses (ALE): It covers the cost of temporary housing, meals, and other essentials if your rental unit is uninhabitable. 3) Personal Liability: It protects you if you are found legally responsible for starting a fire that damages the building or injures others. Understanding this three-part protection is essential for any tenant. Learn more about the basics in our guide on what renters insurance is.

Understanding Fire Damage Coverage in a Renters Policy

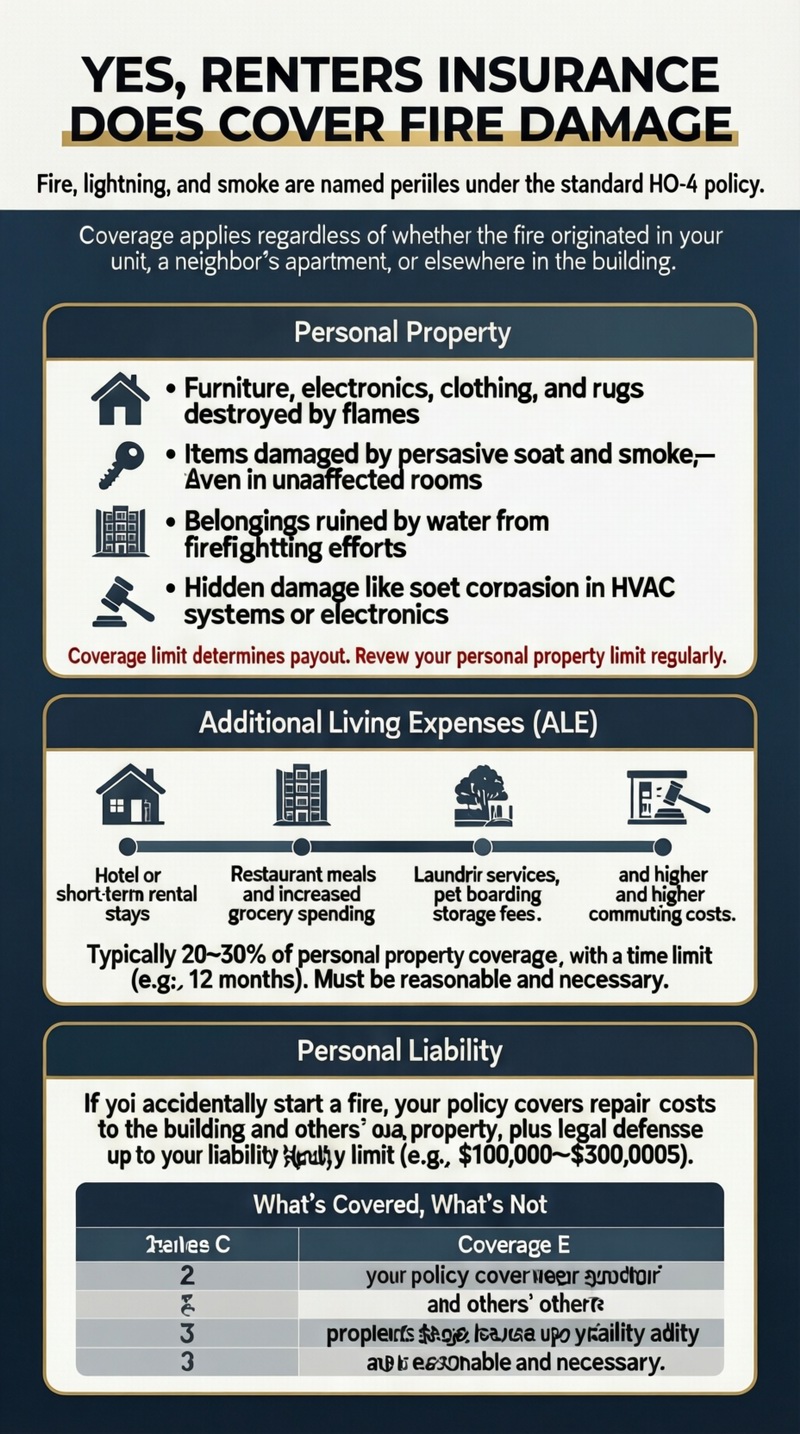

When asking, “does renters insurance cover fire damage?” you’re addressing a core reason the product exists. Fire, along with lightning and smoke, is a named peril in the standard policy. This means coverage is explicitly granted. It doesn’t matter if the fire starts in your unit (e.g., a kitchen accident), spreads from a neighbor’s apartment, or originates elsewhere in the building; the damage to your personal property is covered. The policy covers the direct flames, intense heat, and the pervasive soot and smoke that can ruin belongings even in rooms untouched by the fire itself. This comprehensive approach is vital, as smoke damage is often more widespread than burn damage.

What Exactly Is Covered Under Personal Property?

Your policy’s Coverage C (Personal Property) applies to all your insurable belongings. After a fire, this includes:

– Destroyed Items: Furniture, mattresses, clothing, rugs that are burned.

– Smoke-Damaged Items: Items that smell of smoke and require professional cleaning or replacement.

– Water-Damaged Items: Belongings damaged by water used by firefighters to extinguish the blaze.

– Hidden Damage: Soot corrosion on electronics or within HVAC ducts serving your unit.

The coverage limit is the maximum your insurer will pay, so it’s crucial to have a limit that reflects the total value of everything you own. Review your renters insurance coverage limits regularly.

The Critical Role of Additional Living Expenses (ALE)

Perhaps the most immediate relief after a fire comes from Loss of Use or ALE coverage. If a fire renders your rental unit unsafe or uninhabitable (due to structural damage, lack of utilities, or pervasive smoke odor), your insurance will pay for you to maintain your normal standard of living elsewhere. This includes:

– Hotel or short-term rental apartment costs.

– Restaurant meals and food costs beyond what you normally spend on groceries.

– Laundry service, pet boarding, storage unit fees, and increased commuting costs.

ALE coverage typically has a limit (often 20-30% of your personal property coverage) and a time limit (e.g., 12 months). It is a lifeline while your rental is being repaired.

What’s Covered, What’s Not, and Key Limitations

While fire is a covered cause of loss, it’s important to understand the boundaries, sub-limits, and conditions of your policy. The following table outlines common scenarios and how they are typically handled, providing a clear answer to “does renters insurance cover fire damage?” in various situations.

| Scenario / Item Type | Typically Covered? | Important Details & Limitations |

|---|---|---|

| Belongings damaged by fire/smoke | YES | Covered up to your personal property limit. Valuation (Actual Cash Value vs. Replacement Cost) drastically affects payout. |

| Temporary housing & living expenses | YES | Covered under ALE. Must be “reasonable” and necessary. Keep all receipts. |

| Damage to the rental building itself | NO | This is the landlord’s responsibility, covered by their property insurance. |

| Liability if you accidentally start the fire | YES | Your liability coverage pays for damage to the building and others’ property, plus legal defense. |

| Fire caused by arson (by you or a household member) | NO | Intentional, criminal acts are excluded. Could lead to denial and prosecution. |

| High-value items (jewelry, art, collectibles) | YES, but sub-limited | Special sub-limits apply (e.g., $1,500 for jewelry). May need a “scheduled” endorsement for full value. |

| Business property in the home | YES, but limited | Often capped at $2,500 for business equipment. A separate policy may be needed. |

Actual Cash Value vs. Replacement Cost: The Payout Difference

This is the single most important factor in how much money you receive for damaged belongings. A policy with Actual Cash Value (ACV) pays the depreciated value of your items. A 5-year-old TV lost in a fire might only net you $100. A policy with Replacement Cost Value (RCV) pays the amount needed to buy a brand-new, comparable TV at today’s prices, which could be $500 or more. RCV coverage typically costs 10-20% more but is worth it, especially for a total loss like a fire. Always opt for RCV if available.

What If the Fire Is Your Fault?

Your liability coverage (Coverage E) is designed for this. If your cooking, unattended candle, or faulty wiring causes a fire that damages the building or other tenants’ property, your insurer will cover the repair costs up to your liability limit (e.g., $100,000 or $300,000). It also provides a legal defense if you are sued. This protects your personal assets (savings, future wages) from being seized to pay for damages. This is a critical component of the answer to “does renters insurance cover fire damage?” that you cause.

The Fire Damage Claims Process: A Step-by-Step Guide

After a fire, safety and swift action are paramount. Follow these steps to navigate the insurance process effectively.

Step 1: Ensure Safety and Report. Do not re-enter the property until firefighters declare it safe. Contact the fire department immediately if the fire is still active.

Step 2: Notify Your Landlord. Inform your landlord or property manager of the fire immediately. They need to secure the property and file a claim under their own insurance for the building.

Step 3: Contact Your Insurance Company. Notify your renters insurance provider as soon as possible to start the claims process. Have your policy number ready.

Step 4: Document Everything. Once authorized to enter, take extensive photos and videos of all damaged areas and items. Do not throw anything away until the adjuster has seen it.

Step 5: Create a Detailed Inventory. List every damaged item, including description, brand, model, age, and estimated value. A pre-existing home inventory is invaluable here.

Step 6: Secure Temporary Housing. If you need to relocate, keep all receipts for hotels, meals, and other expenses for your ALE claim.

Step 7: Cooperate with the Adjuster. The insurance adjuster will investigate the cause and assess the damage. Provide your documentation and inventory list.

Step 8: Review the Settlement. Carefully review the adjuster’s settlement offer. For RCV policies, you may receive an initial ACV payment, then a second payment after you replace items and submit receipts.

Working with Multiple Insurance Companies

In a multi-unit fire, there will be multiple claims: your renters claim for your belongings, your landlord’s claim for the building, and possibly other tenants’ claims. Your adjuster handles only your claim. Do not give recorded statements to other insurers (like the landlord’s insurer) without consulting your own adjuster first. For complex situations, resources like the Insurance Information Institute’s fire recovery guide can be helpful.

Preventing Fires and Maximizing Your Coverage

While knowing renters insurance does cover fire damage is crucial, prevention is the best policy. Many insurers offer discounts for having smoke alarms, fire extinguishers, and monitored fire alarm systems. Proactively managing risk can lower your premium and, more importantly, save lives. To maximize your financial recovery after a fire, ensure you have: 1) Sufficient personal property limits (conduct a home inventory). 2) Replacement Cost Value coverage. 3) Adequate ALE limits to cover local hotel costs for an extended period. 4) High enough liability limits to protect your net worth. Understand how these choices affect your overall renters insurance cost.

Common Exclusions Related to Fire

While fire is covered, certain related events may have limitations:

– Earthquake or Flood Fire: If an earthquake ruptures a gas line causing a fire, the fire damage is covered, but the earthquake damage is not. Same for a flood causing an electrical fire.

– Vacancy: If you move out and leave the unit vacant for a period defined in the policy (often 30-60 consecutive days), coverage for certain perils like vandalism or fire may be suspended.

– Neglect: If you knowingly ignore a severe electrical problem that leads to a fire, the claim could be denied due to negligence.

Conclusion: Essential Protection for a Devastating Event

In conclusion, the answer to “does renters insurance cover fire damage?” is a resounding yes, and it does so with multi-layered protection that is indispensable. It replaces your worldly possessions, provides a roof over your head during recovery, and legally and financially shields you if you are at fault. A fire is a traumatic event; having a robust renters insurance policy means one less devastating problem to face. By choosing adequate limits, opting for Replacement Cost coverage, and maintaining a home inventory, you ensure that this safety net will function as intended when you need it most. Don’t wait—review your policy today to ensure you have the fire protection you need. Explore all renters insurance options to find the right fit.

Frequently Asked Questions (FAQ)

Does renters insurance cover smoke damage from a neighboring unit’s fire?

Yes. Smoke damage is a direct result of fire and is covered under the fire peril. If a fire in another apartment or building causes smoke to permeate your unit, damaging walls, furniture, clothing, and electronics, your renters insurance will cover the cost to clean or replace those items. This is true even if the flames never touched your apartment.

What if I can’t remember everything I owned for the inventory?

This is a common challenge. Start by listing what you can remember by room. Look at old photos or videos of your home for clues. Ask friends and family if they have pictures from gatherings at your place. Check online purchase histories (Amazon, credit card statements). For a total loss, a detailed inventory is crucial for a fair settlement. This underscores the importance of creating a home inventory before a disaster strikes.

Will my rates go up if I file a fire damage claim?

It is possible. Filing any claim, especially a large one like a fire, may cause your premium to increase at renewal because you are now considered a higher risk. The increase will depend on your insurer’s policies, your claims history, and whether you were at fault. However, the financial protection provided by filing a legitimate claim for a significant loss almost always outweighs the potential for a future premium increase.

How long does it take to get paid after a fire claim?

The timeline varies. For straightforward claims with clear documentation, you may receive an initial advance or settlement within a few weeks. Complex fires involving large losses, liability questions, or multiple parties can take several months. Your ALE payments for immediate living expenses should begin quickly once you submit receipts. Communication with your adjuster is key to managing expectations.

Does renters insurance cover food that spoils after a fire cuts power?

Typically, yes. If a fire causes a power outage that leads to food spoilage in your refrigerator or freezer, this is generally covered as a direct result of the covered peril (the fire). You will need to document the loss (photos of the spoiled food) and may be subject to a special sub-limit for food (e.g., $500). Check your specific policy language.

Am I covered if a wildfire forces me to evacuate?

Yes. If a wildfire is approaching and a mandatory evacuation order is issued, your Additional Living Expenses (ALE) coverage is triggered even if your home hasn’t burned yet. It covers your evacuation costs (hotel, meals). If your home is later damaged or destroyed by the wildfire, your personal property coverage applies for your belongings.

What if the fire was caused by my landlord’s faulty wiring?

Your renters insurance still covers your personal property damage. Your insurer would pay you directly. They may then pursue a process called “subrogation” against your landlord or their insurance company to recover the money they paid you, if the landlord’s negligence is proven. This does not delay your payment or involve you directly after your claim is settled.