The direct answer is yes, renters insurance will cover stolen items in the vast majority of cases, whether the theft occurs inside your apartment, from your car, or while you’re traveling. Theft is a standard “named peril” in virtually all renters insurance policies. However, there are critical conditions, limits, and exclusions you must understand. Coverage depends on the circumstances being a legitimate theft, you filing a police report, and your belongings falling within your policy’s personal property limit and any applicable sub-limits for high-value items like jewelry. This guide will detail exactly how theft coverage works, the claims process, and how to ensure you’re fully protected. Understanding this is a core part of knowing what renters insurance is designed to do.

Understanding Theft Coverage in Your Renters Policy

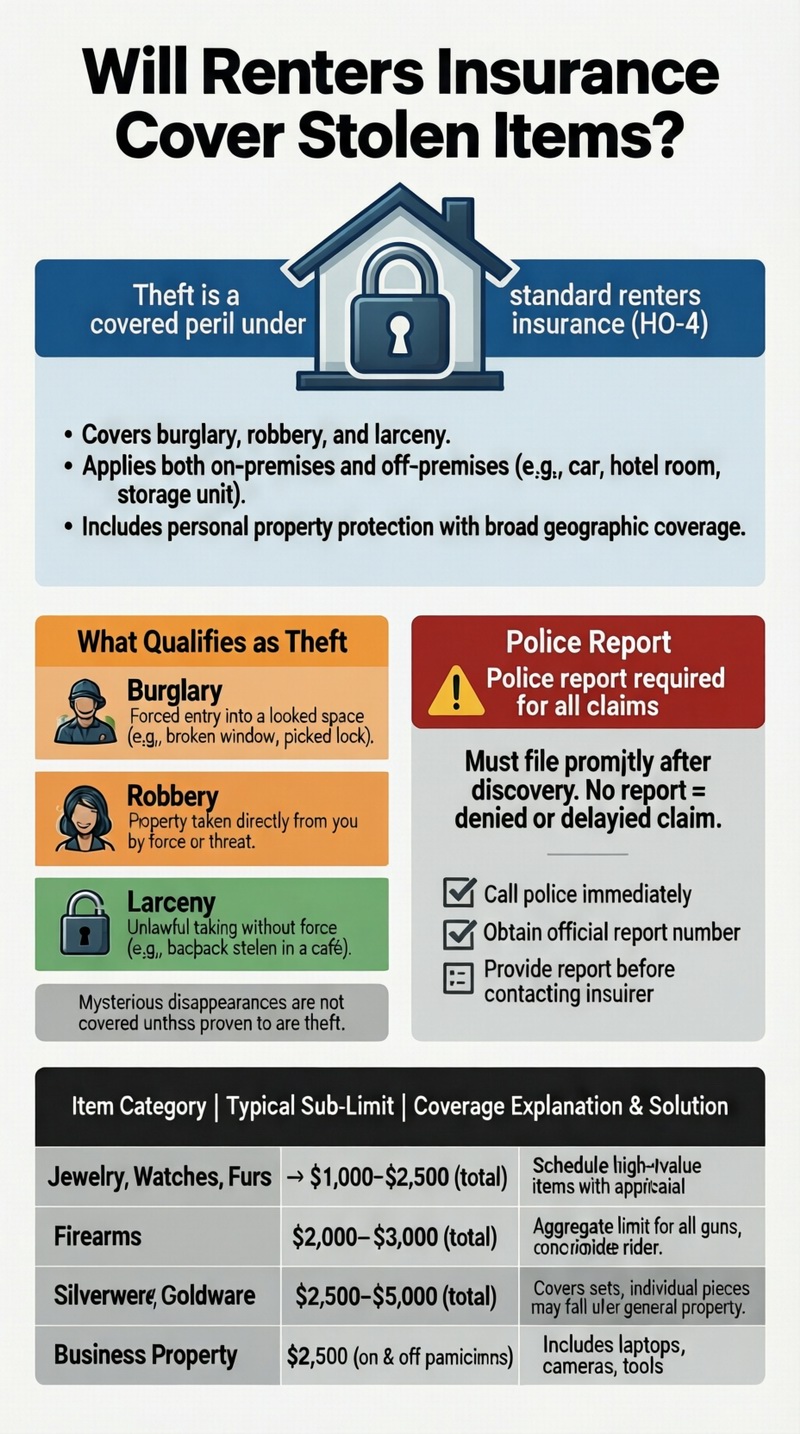

When you ask, “will renters insurance cover stolen items?” you’re addressing one of the most common and valuable protections the policy provides. Theft is explicitly listed as a covered peril in the standard renters insurance policy form (HO-4). This means if your belongings are stolen due to an act of burglary, robbery, or larceny, your policy’s personal property coverage should respond. Coverage applies not just within your rented dwelling but also “off-premises,” meaning items stolen from your car, a hotel room, or even a storage unit are typically covered. This broad protection is a key reason renters insurance is considered essential. For a full overview, explore our guide on renters insurance coverage details.

What Qualifies as a “Covered Theft”?

Insurance defines theft as the unlawful taking of property. This encompasses:

Burglary: Forced entry into a locked premises (e.g., a broken window or picked lock).

Robbery: Property taken directly from you through force or threat of force.

Larceny: The simple act of stealing without force (e.g., someone takes your backpack from a coffee shop while you’re in the restroom).

The key is that the act must be illegal and done with intent to deprive you of your property. Mysterious disappearances (e.g., “I think I lost my ring somewhere”) are usually not covered unless you can prove it was likely stolen.

The Critical Role of the Police Report

One non-negotiable step in answering “will renters insurance cover stolen items?” is the police report. Insurers almost universally require you to file a report with the local police department promptly after discovering the theft. This report serves as official documentation of the crime, helps establish the timeline and value of lost items, and protects the insurer from fraudulent claims. Without a police report number, your claim is likely to be denied or severely delayed. Always file the report before calling your insurance company to start the claim.

What’s Covered, What’s Not, and Important Limits

While theft is a covered peril, your policy is not a blank check. Specific limits and exclusions apply. The maximum payout for all stolen items combined cannot exceed your chosen personal property coverage limit (e.g., $30,000). More importantly, most policies have special sub-limits for certain categories of valuable items. This means even if you have $30,000 in total coverage, you may only be able to recover a small fraction of that for specific stolen goods. The following table outlines common categories and their typical sub-limits, which are crucial to understanding the real scope of theft coverage.

| Item Category | Typical Sub-Limit | Coverage Explanation & Solution |

|---|---|---|

| Jewelry, Watches, Furs | $1,000 – $2,500 (total) | This is a total limit for all items in this category. A single stolen $5,000 engagement ring would not be fully covered. Solution: “Schedule” high-value items with an appraisal. |

| Firearms | $2,000 – $3,000 (total) | Similar to jewelry, this is an aggregate limit for all guns stolen in a single loss. |

| Silverware, Goldware | $2,500 – $5,000 (total) | Covers precious metalware sets. Individual pieces may fall under general property. |

| Business Property | $2,500 (on & off premises) | Includes laptops, cameras, or tools used for work. Limit applies separately from personal electronics. |

| Money, Bank Notes, Bullion | $200 – $500 (total) | Very low limit for cash, coins, and precious metals in bar form. |

| Watercraft & Trailers | $1,000 – $1,500 | For smaller boats, canoes, and their trailers. Larger vessels need a separate policy. |

Common Exclusions to Theft Coverage

Beyond sub-limits, certain situations may be excluded. Most policies will not cover theft if it’s committed by someone who lives in your household or is a named insured on your policy. If your roommate steals from you, your insurance won’t cover it (this is a civil matter). Furthermore, if your property is stolen from a residence you’ve voluntarily left vacant for an extended period (often 30+ consecutive days), coverage may be suspended. Always check your policy’s “vacancy clause.”

Actual Cash Value vs. Replacement Cost: A Major Payout Difference

When your claim is paid, the valuation method makes a huge difference. A basic policy with Actual Cash Value (ACV) will pay you the item’s depreciated value. A 5-year-old stolen laptop might only net you $150. A policy with Replacement Cost Value (RCV) coverage will pay you the cost to buy a new, comparable laptop today, which could be $800. RCV coverage is usually worth the slight premium increase and is a critical factor in how fully you recover from a theft.

The Step-by-Step Claims Process for Stolen Items

Knowing the procedure is essential when you need to turn the answer to “will renters insurance cover stolen items?” into actual reimbursement. Acting quickly and methodically protects your rights and streamlines the process.

Step 1: Ensure Safety & Contact Police. If you discover a burglary, do not touch anything. Leave the premises and call the police from a safe location. File an official police report and obtain the report number.

Step 2: Notify Your Landlord. Inform your property manager or landlord of the break-in, as they may need to secure the property (fix a broken door lock).

Step 3: Contact Your Insurance Company. Call your insurer’s claims department or start a claim online. Provide your policy number, the police report number, and a brief description of the loss.

Step 4: Document Everything. Take photos of any signs of forced entry and the areas where items are missing. Create a detailed list of all stolen items. This is where a pre-existing home inventory is invaluable.

Step 5: Work with the Adjuster. A claims adjuster will be assigned. They may ask for your inventory list, receipts, photos, manuals, or credit card statements to establish ownership and value.

Step 6: Receive Payment. After verification, you will receive a payment for the covered amount, minus your deductible. For RCV policies, you may get an initial ACV payment, then a second payment after you provide a receipt for the replacement item.

The Importance of a Home Inventory

The single best thing you can do to prepare for a theft claim is to maintain a current home inventory. This is a detailed list, with photos or videos, serial numbers, and receipts (or estimated values/purchase dates) for your belongings. Store this digitally (e.g., in the cloud). After a theft, when you’re stressed, this document makes compiling your claim list fast and accurate, and it provides strong evidence for the insurer, leading to a smoother and potentially larger settlement. Without it, you’re likely to forget items and struggle to prove you owned them.

How Your Deductible Affects Your Claim

Your deductible is the amount you pay out of pocket before insurance kicks in. If you have a $500 deductible and $2,000 worth of stolen goods, the insurer will pay $1,500. For small thefts where the total loss is close to or below your deductible, it may not make financial sense to file a claim, as it could lead to a future premium increase. Consider the cost of renters insurance and your chosen deductible when evaluating your risk.

Preventing Theft and Maximizing Your Coverage

While knowing will renters insurance cover stolen items is crucial, prevention is better. Many policies offer discounts for having security devices like monitored alarm systems, deadbolt locks, or smoke detectors. Proactively securing your apartment not only reduces risk but can also lower your premium. Furthermore, to maximize your coverage, review your policy’s sub-limits annually. If you acquire expensive jewelry, electronics, or art, contact your insurer to “schedule” these items. This involves getting a professional appraisal and adding a rider to your policy for a specific premium, which provides full, stated-value coverage for that item without a deductible in many cases.

What About Theft from Vehicles?

This is a common point of confusion. Yes, renters insurance typically covers items stolen from your car. Your laptop bag stolen from your back seat is covered under your renters policy’s off-premises theft coverage. However, the car stereo, built-in navigation system, or any damage to the vehicle itself (broken window, slashed seats) is covered by your auto insurance comprehensive coverage, not your renters policy. It’s important to file claims with the correct insurer.

Consulting Authoritative Resources

For official information on property insurance and theft, the Insurance Information Institute is an invaluable non-profit resource. Their article on homeowners and renters insurance provides authoritative context on how these policies function, including the principles behind theft coverage.

Conclusion

So, will renters insurance cover stolen items? Emphatically, yes—it is a fundamental protection. However, a successful claim hinges on understanding the rules: filing a police report, being aware of sub-limits for valuables, knowing the difference between ACV and RCV, and maintaining a home inventory. Renters insurance provides powerful financial recovery after the violation of a theft, but it works best for policyholders who are informed and prepared. By taking the steps outlined here, you can ensure that if the unfortunate happens, you’ll be able to replace your stolen belongings and move forward with minimal financial strain. Explore all renters insurance options to find a policy with the right theft protections for your lifestyle.

Frequently Asked Questions (FAQ)

Does renters insurance cover a stolen bicycle?

Yes, typically. A stolen bicycle is covered under the personal property theft coverage of your renters insurance, whether it was taken from a locked garage, a bike rack, or even a public rack. However, if you own a very high-end bicycle (e.g., worth over $3,000), its value might exceed the general personal property limits for sports equipment. In that case, you may need to schedule it separately to ensure full coverage. Always note the serial number and take a photo of your bike for claim purposes.

What if my stolen phone was not locked with a password?

Your phone’s security settings generally do not affect your insurance coverage. As long as the incident qualifies as a legitimate theft (you didn’t just lose it), and you file a police report, your renters insurance should cover it, subject to your deductible and any sub-limits for electronics. The insurer is concerned with the unlawful taking of property, not the security features on the device itself.

Will filing a theft claim raise my renters insurance premium?

It might. Like most insurance, filing a claim can lead to a premium increase at renewal because you are now statistically a higher risk. The impact depends on your insurer’s policies, your claims history, and the claim amount. For a small claim barely above your deductible, the potential premium increase over several years might outweigh the payout. It’s often advisable to file claims only for significant losses and use insurance for its intended purpose: protecting you from major financial hardship.

Are stolen packages from my doorstep covered?

Yes, this is a growing area of coverage. “Porch piracy” is generally considered theft and is covered under your renters insurance, as the packages are considered your personal property once delivered. You will need to provide evidence, such a delivery confirmation from the retailer and possibly security camera footage. However, for frequent low-value package thefts, it may not be worth filing a claim due to your deductible and potential rate increases.

How long do I have to file a theft claim?

You should file a claim as soon as possible after discovering the theft and filing a police report. While policies have a “suitability clause” that gives you typically one to two years from the date of loss to formally sue the insurer, delaying your claim is strongly discouraged. A long delay can raise questions about the validity of the claim and make it harder to gather evidence (like security footage) and remember all stolen items. Notify your insurer within 24-48 hours if possible.

Does renters insurance cover identity theft if my wallet is stolen?

Standard renters insurance does not cover the financial losses or legal fees associated with identity theft. However, many insurers offer an optional identity theft endorsement or “fraud expense coverage” for an additional small premium. This add-on can cover costs like notarization fees, lost wages for time spent resolving the issue, and sometimes reimbursement for stolen funds. If your wallet with IDs and cards is stolen, you should primarily focus on canceling cards and placing fraud alerts.

What proof do I need for stolen items without receipts?

You can still successfully claim items without receipts. Proof can include: clear photographs or videos of the items in your home (from your home inventory), credit card or bank statements showing the purchase, owner’s manuals or warranty cards with serial numbers, model numbers from old product boxes, or even photos from social media that show you with the item. The more corroborating evidence you have, the smoother the process will be.