In this QBE renters insurance review, we find that QBE is a massive, A-rated global insurance group, but its renters insurance products are typically not sold directly to individual consumers. Instead, QBE renters insurance is most often accessed through specialty programs, affinity groups, or as part of a corporate or institutional housing partnership. For the average renter shopping online, QBE will likely not appear as a direct option. However, if you are offered a QBE policy through your employer, university, or a membership organization, it can represent a convenient and potentially competitive group-rated option. The coverage is robust and backed by a financially strong carrier, but customization and direct customer service may be limited compared to going through a traditional agent or digital insurer. For the basics, see our guide on what renters insurance is.

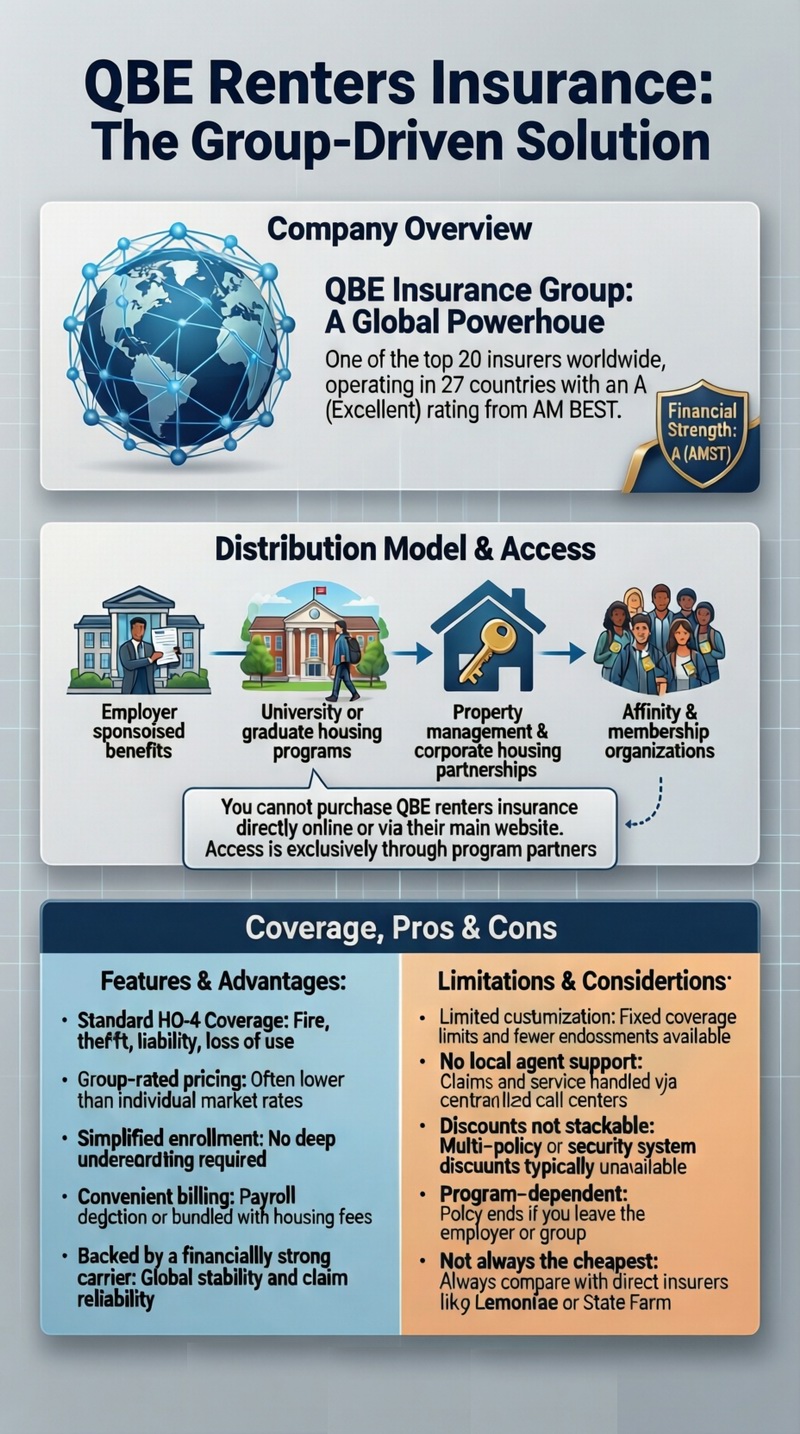

QBE Insurance Group: A Global Powerhouse

Understanding QBE renters insurance requires context about the company. QBE Insurance Group is an Australian multinational, one of the top 20 global insurers and reinsurers. It operates in over 27 countries and holds strong financial strength ratings (e.g., A from AM Best). In the U.S., QBE provides a wide range of commercial, specialty, and personal insurance products. Their foray into renters insurance is often through their “North America” segment, targeting specific market niches rather than the broad consumer market. This means you’re dealing with an extremely stable and experienced insurer, but one with a different distribution model than State Farm or Allstate.

The Distribution Model: How You Get a QBE Policy

You won’t call QBE directly or get a quote on their main website for a standard renters policy. Instead, QBE partners with:

– Employers: As a voluntary benefit offered to employees.

– Universities & Educational Institutions: For student housing or as a recommended provider for graduate students/faculty.

– Property Management Companies & Corporate Housing Providers: As a bundled or recommended option for their tenants.

– Affinity & Membership Groups: Offered to members of large organizations.

These programs often feature simplified enrollment, group discounts, and payroll deduction for payment.

Coverage, Features, and Policy Details

When offered through a program, QBE renters insurance provides the standard coverages you’d expect: personal property, personal liability, medical payments, and loss of use. The specifics (limits, deductibles, optional endorsements) will be determined by the design of the group program. However, based on QBE’s general approach, we can outline typical features and considerations.

| Coverage Aspect | Typical QBE Offering (Program-Dependent) | Review Notes & Considerations |

|---|---|---|

| Financial Strength | A (Excellent) from AM Best | A major strength. Policyholders have security knowing claims will be paid by a global giant. |

| Policy Coverage | Standard HO-4 (Named Perils) | Includes fire, theft, liability, etc. Exact perils list should be verified in the program materials. |

| Customization & Endorsements | Limited within a group program | You may have set limit options and fewer add-ons (e.g., scheduled jewelry, earthquake) than buying individually. Convenience over choice. |

| Claims Process | Centralized through QBE claims department | You would file claims directly with QBE via phone/online. The experience is that of a large insurer; it can be efficient but less personal. |

| Customer Service | Program-specific support + QBE service lines | You may have a dedicated contact for the program. General service is via call centers, not local agents. |

| Discounts | Primarily group-based discount | The main discount is baked into the group rate. Other common discounts (multi-policy, security system) may not be available or stack. |

Potential Advantages of a QBE Group Policy

– Ease of Enrollment: Simplified application, often without a deep underwriting process.

– Competitive Group Rate: The premium may be lower than an individual market policy due to group purchasing power.

– Convenient Billing: Payment via payroll deduction or bundled with other services (like your housing fee) is common.

– Trusted Backer: The QBE name provides assurance of stability.

Potential Drawbacks and Limitations

– Lack of Customization: You may not be able to choose your exact liability limit or add specific endorsements you want.

– Might Not Be the Cheapest: Always compare the group rate with individual quotes from other companies. The group discount isn’t always the best deal.

– Less Personal Service: No local agent to advocate for you or explain complex coverage questions.

– Program-Specific: If you leave the employer or group, you may need to find new insurance, though you can often convert to an individual policy.

Who Should Consider QBE Renters Insurance?

QBE renters insurance is a GOOD FIT if:

– It is offered conveniently through your employer, school, or housing provider as a voluntary benefit.

– The group rate is demonstrably cheaper than quotes you’ve obtained independently.

– You prioritize simplicity and don’t need highly customized coverage.

– You value the financial strength of the insurer behind the policy.

You should SHOP AROUND INDEPENDENTLY if:

– You want to choose your own coverage limits, deductibles, and endorsements (like scheduled jewelry or water backup).

– You prefer working with a local independent agent who can compare multiple companies for you.

– You are eligible for significant bundling discounts (e.g., with your auto insurance) that aren’t available through the QBE program.

– The QBE group rate seems high compared to quotes from direct insurers like Lemonade or traditional carriers like State Farm.

Always compare. Explore all renters insurance options to ensure the best value.

The Claims Process with QBE

If you need to file a claim, you would contact the QBE claims department using the information provided in your policy documents. The process is typical of a large insurer:

1. Report the claim via phone or online portal.

2. Provide your policy number (linked to your group program) and details of the loss.

3. A claims adjuster will be assigned to investigate and assess the damage.

4. You’ll submit documentation (photos, police reports, inventories).

5. The adjuster will determine coverage based on your policy terms and issue payment if covered.

Because it’s a group policy, there may be a specific contact or process outlined by your program administrator.

Conclusion: A Niche but Solid Option

In summary, QBE renters insurance is a legitimate and financially robust product, but it exists in a specific channel. For the average renter, it’s not something you seek out; it’s something that may be offered to you. If you encounter it, treat it like any other option: get the quote, understand the coverage limits and exclusions, and then compare it to a few quotes from the open market. Its greatest strengths are the convenience of group enrollment and the backing of a global insurer. Its potential weakness is a lack of flexibility. By doing your homework, you can determine if the QBE group program is the right balance of cost and coverage for your needs. For more on evaluating renters insurance cost and value, see our guide.

Frequently Asked Questions (FAQ)

Can I buy QBE renters insurance directly as an individual?

Generally, no. QBE’s personal insurance lines in the U.S. are primarily distributed through partnerships, programs, and sometimes independent agents for specialty products. An individual consumer looking for a standard renters policy will not find a direct-to-consumer portal on QBE’s main website. Your access is almost exclusively through a sponsoring organization.

Is QBE renters insurance good for students?

It can be an excellent option if offered through the university. University-sponsored programs are often tailored for students, with appropriate limits and simple enrollment. The premium might be billed to the student account, and coverage is designed for dorm or off-campus housing risks. Always compare with a parent’s homeowners policy extension or a standalone student policy.

How does QBE handle claims for high-value items like electronics?

Like all insurers, QBE policies have sub-limits for categories like electronics, jewelry, and cash. If your group policy doesn’t allow you to schedule (separately insure) high-value items, you may be underinsured. It’s critical to review the policy’s “special limits of liability” section and ensure your expensive laptop or camera collection is adequately covered, possibly through a separate policy or endorsement if available.

What happens to my QBE renters insurance if I leave my job or graduate?

Your coverage is typically tied to your membership in the group. When you leave, the policy may be canceled or you may be offered the option to convert it to an individual policy directly with QBE (often at a different rate). You will need to secure new renters insurance for your next home if you do not convert.

Does QBE offer bundling discounts with auto insurance?

Typically, no, because the renters policy is offered through a specific program, not as part of a package you build yourself. If you have auto insurance elsewhere, you likely cannot bundle to get a discount. However, QBE does offer auto insurance in some channels, so it’s worth asking your program administrator if a bundle is possible.

How do I contact QBE for customer service?

Contact information will be provided in your policy documents and likely by the program sponsor (your HR department, university housing, etc.). There will be a dedicated phone number and possibly an online portal for the specific program you are enrolled in.

Where can I find independent financial ratings for QBE?

You can view the financial strength ratings from major agencies like AM Best, Standard & Poor’s, and Moody’s directly on the QBE Group’s financial ratings page. This is an authoritative source for verifying the insurer’s stability.