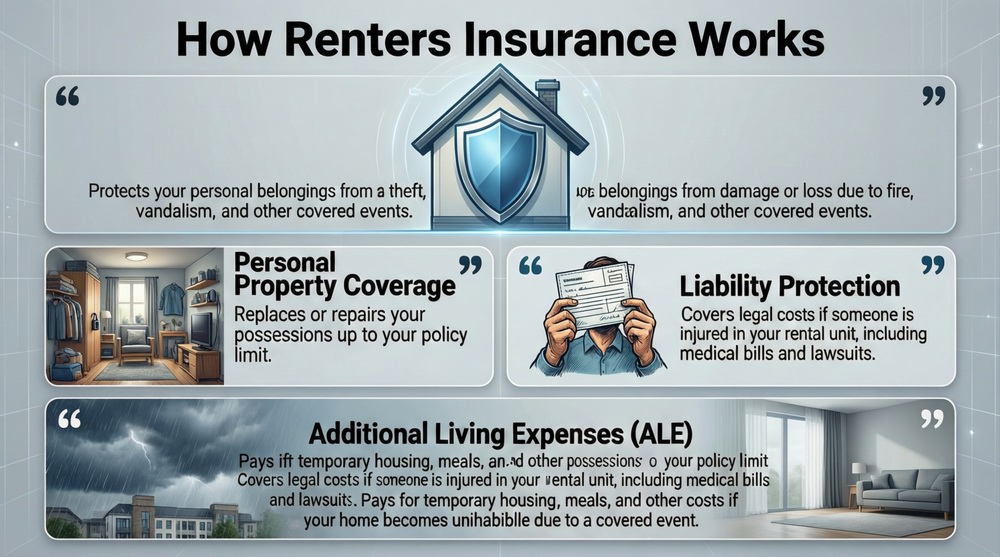

How does renters insurance work? In essence, it’s a contract where you pay a small, regular premium to an insurance company. In exchange, they agree to cover specific financial losses related to your rented home. It works by protecting you in three key areas: 1) Your Stuff: It pays to repair or replace your personal belongings if they’re stolen or damaged by events like fire, theft, or vandalism. 2) Your Liability: It covers legal and medical costs if you’re found responsible for injuring someone or damaging their property. 3) Your Living Expenses: It pays for temporary housing (like a hotel) if your rental becomes uninhabitable due to a covered event. For a monthly fee often less than your streaming subscriptions, you transfer massive financial risk to the insurer. Start with the basics in our article on what renters insurance is.

The Core Mechanics: The Policy as a Legal Contract

Understanding how does renters insurance work begins with recognizing it as a binding legal agreement (policy). You (the policyholder) agree to pay a premium, usually monthly or annually. The insurance company agrees to provide financial compensation for covered losses, as defined in the policy document, up to specified dollar limits. The policy outlines exactly what is covered (named perils), what is excluded, how much you’ll receive for a loss (based on valuation method), and how much you pay out-of-pocket first (your deductible). This contract is governed by state insurance regulations, ensuring standard practices and consumer protections.

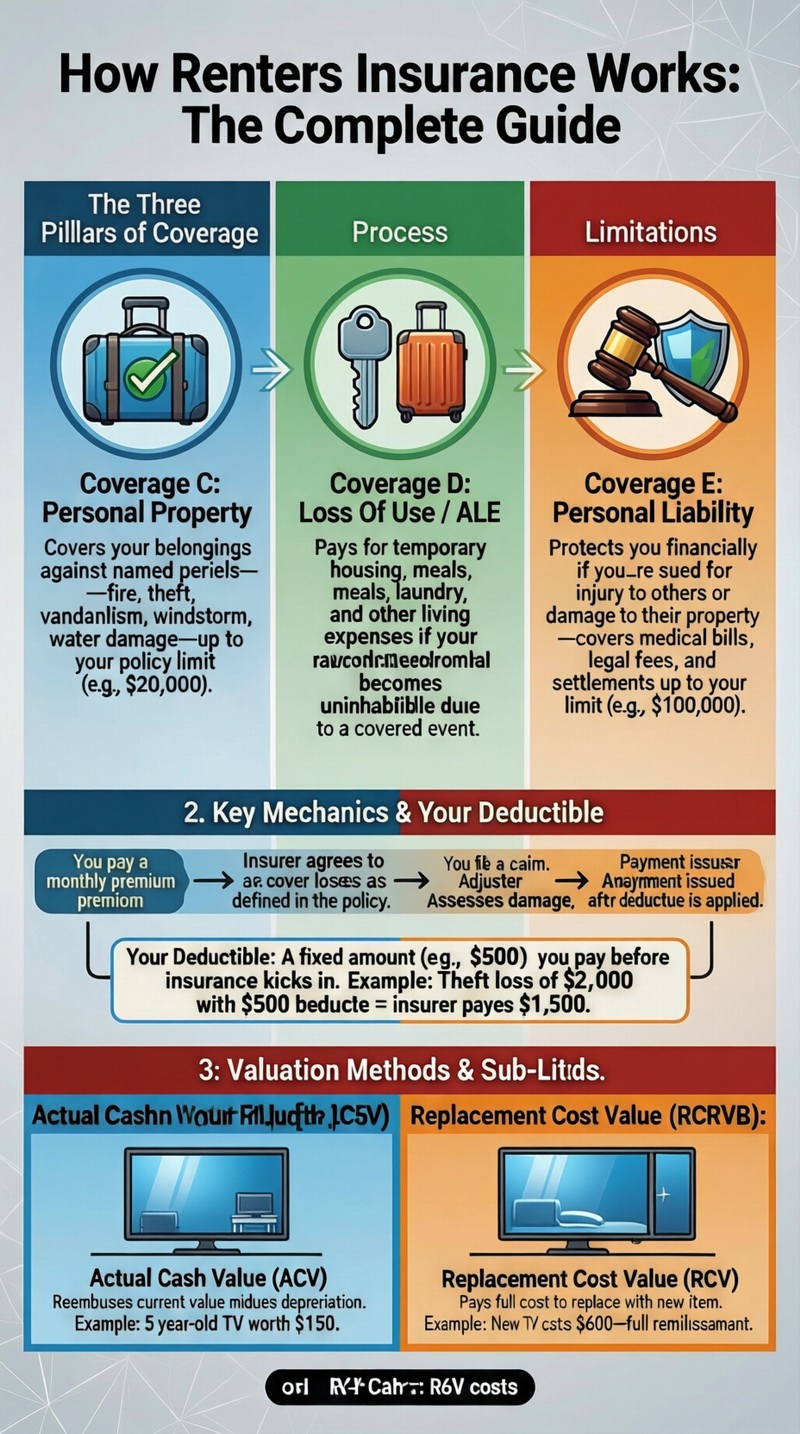

The Three Pillars of Coverage: C, D, and E

Renters insurance policies are standardized into sections. Knowing these helps decode how renters insurance works:

Coverage C – Personal Property: This is coverage for your belongings. You choose a total limit (e.g., $20,000). It covers items against “named perils” like fire, theft, vandalism, windstorm, and more.

Coverage D – Loss of Use / Additional Living Expenses (ALE): If a covered event makes your home unlivable, this pays for extra costs like hotel bills, restaurant meals, and laundry.

Coverage E – Personal Liability: This protects your finances if you are legally liable for bodily injury or property damage to others. It pays for their medical bills, repairs, and your legal defense, up to your policy limit (e.g., $100,000).

The Role of Your Deductible

Your deductible is your share of the financial responsibility in a claim. It’s a fixed dollar amount you must pay before the insurance company pays anything. For example, if you have a $500 deductible and a $2,000 theft loss, you pay $500, and the insurer pays $1,500. Choosing a higher deductible lowers your premium but increases your out-of-pocket cost when you file a claim.

A Detailed Breakdown: What’s Covered and How Payments Work

Let’s get practical. How does renters insurance work when something actually happens? The following table illustrates common scenarios, showing which part of your policy responds and how the financial settlement is calculated. This is the operational heart of the coverage. For a deeper dive into protection details, see our guide on renters insurance coverage.

| What Happens (The Loss) | Which Coverage Applies | How It Works / Payment Example |

|---|---|---|

| Your laptop is stolen from your apartment. | Coverage C – Personal Property | You file a police report and a claim. Insurer determines value. If laptop’s Replacement Cost is $1,200 and your deductible is $500, you receive a check for $700. |

| A kitchen fire makes your apartment unsafe for 2 weeks. | Coverage D – Loss of Use (ALE) & Coverage C | ALE: You stay in a hotel ($100/night x 14 days = $1,400). You submit receipts and are reimbursed. Property: Your damaged belongings are separately paid for under Coverage C. |

| A guest slips on your rug, breaks an arm, and sues you. | Coverage E – Personal Liability | Your insurer provides a lawyer. If found liable, they pay the guest’s medical bills and settlement up to your limit (e.g., $50,000). You pay nothing beyond your deductible (which often doesn’t apply to liability claims). |

| A pipe bursts, ruining your furniture and books. | Coverage C – Personal Property | Water damage from plumbing is a covered peril. The insurer assesses the damage, applies depreciation if ACV, subtracts your deductible, and issues payment. |

| Your bike is stolen from a public bike rack. | Coverage C – Personal Property (Off-Premises) | Renters insurance covers belongings anywhere in the world, typically at 10% of your total limit. So if you have $20k coverage, you have $2k for off-premises theft. |

Actual Cash Value vs. Replacement Cost: The Critical Choice

When your insurer pays for a lost item, the valuation method drastically changes the amount. Actual Cash Value (ACV) reimburses you for the item’s current worth, minus depreciation. A 5-year-old TV might be worth $150. Replacement Cost Value (RCV) pays you the amount needed to buy a brand-new, comparable TV at today’s prices, which could be $600. RCV coverage costs about 10-25% more but is almost always worth it. It fundamentally changes how renters insurance works for you financially after a loss.

Understanding Sub-Limits and Scheduled Items

Your policy has overall limits, but also “sub-limits” for specific categories. For example, you might have $20,000 total coverage but only $1,500 for jewelry theft. If you own a $5,000 engagement ring, it would not be fully covered. To insure high-value items fully, you “schedule” them. This involves getting an appraisal and adding a rider to your policy for an extra premium, which provides stated-value coverage for that specific item, often with no deductible.

Cost, Factors, and How to Get a Policy

How does renters insurance work in terms of cost? It’s famously affordable. The national average is about $15-$20 per month ($180-$240 annually). Your exact renters insurance cost depends on:

– Location: Crime rates and local disaster risk in your city/zip code.

– Coverage Amounts: Higher personal property and liability limits mean a higher premium.

– Deductible: A higher deductible (e.g., $1,000) lowers your premium; a lower one ($250) raises it.

– Valuation: RCV costs more than ACV.

– Discounts: Bundling with auto insurance, having security systems, being claim-free, and paperless billing can save you 5-20%.

The Step-by-Step Process to Get Covered

1. Inventory Your Belongings: Roughly estimate the total value of your stuff to determine how much Coverage C you need.

2. Get Quotes: Contact 3-4 different insurers (national, local, digital) for quotes. Provide the same coverage details to each for an apples-to-apples comparison.

3. Choose Your Policy: Select the policy that offers the best value (coverage + price + company reputation), not just the cheapest.

4. Apply and Pay: Complete the application, choose your payment plan, and make your first payment. Your coverage starts on the effective date.

5. Provide Proof to Landlord (if required): If your lease mandates it, send your landlord a certificate of insurance.

How to File a Claim: The Process in Action

When loss strikes, here’s how renters insurance works in practice:

1. Report to Authorities: For theft or vandalism, file a police report. For fire or major damage, call the fire department.

2. Mitigate Further Damage: Take reasonable steps to prevent more loss (e.g., stop a leak, board up a broken window).

3. Notify Your Insurer: Contact your insurance company ASAP via phone, app, or website to start the claim.

4. Document Everything: Take photos/videos of the damage. Make a list of damaged/missing items.

5. Cooperate with the Adjuster: An insurance adjuster will contact you to investigate the loss. Provide all documentation.

6. Receive Settlement: Once approved, you’ll receive a payment, minus your deductible. For RCV, you may get a second payment after you replace items and submit receipts.

Common Misconceptions and What Renters Insurance Does NOT Do

To fully grasp how does renters insurance work, you must also know what it doesn’t do. It is NOT your landlord’s insurance, which only covers the building. It typically does NOT cover damage from floods or earthquakes (these require separate policies). It does NOT cover your roommate’s belongings unless they are named on the policy. It does NOT cover business inventory or commercial liability if you run a business from home. It does NOT cover your car (that’s auto insurance) or your health (that’s health insurance). For a broad view of your options, explore all renters insurance options.

The Importance of a Home Inventory

Your claim’s success hinges on proof. A home inventory is a list, with photos/videos and receipts, of your major belongings. Stored digitally (in the cloud), it proves ownership and value after a loss, making the claims process faster and ensuring you don’t forget items. It’s the single best thing you can do to make your policy work effectively for you.

Conclusion: An Essential, Affordable Safety Net

So, how does renters insurance work? It works as a simple, powerful, and remarkably affordable financial safety net designed specifically for tenants. For a minimal monthly cost, it protects the value of your possessions, shields you from catastrophic liability lawsuits, and ensures you have a place to stay if disaster strikes. It works by spreading risk across millions of policyholders, allowing the insurer to pay for the few who experience major losses. By understanding the three pillars of coverage, choosing the right limits and RCV, and maintaining a home inventory, you ensure this system works perfectly for you when you need it. Don’t wait for a disaster to learn its value—secure your policy today.

Frequently Asked Questions (FAQ)

Is renters insurance mandatory?

While not state-mandated, it is increasingly required by landlords and property management companies as a condition in the lease. They want to ensure you can cover liability claims and replace your belongings without seeking recourse against them. Even if not required, it’s a wise financial decision for virtually every renter.

How much renters insurance do I really need?

For Personal Property, enough to replace everything you own. Conduct a home inventory. For Liability, at least $100,000, but consider $300,000+ if you have assets to protect or higher risk. For ALE, ensure the limit (often 20-30% of your property limit) is enough to cover local hotel costs for several months.

Can my landlord require me to have renters insurance?

Yes. Landlords have the legal right to include a clause in the lease requiring you to carry renters insurance with specific minimum coverages (e.g., $100,000 liability). They can also require you to provide proof (a certificate of insurance) and name them as an “additional interest.”

Does renters insurance cover my roommate?

Generally, no. A standard policy covers the “named insured” and their relatives. An unrelated roommate is not automatically covered. They need their own separate policy. Some insurers offer policies that cover multiple unrelated tenants, but all must be named on the policy, and payouts for shared property can be complicated.

What’s the difference between “peril” and “hazard”?

A peril is the actual cause of a loss (fire, theft, windstorm). Your policy lists covered perils. A hazard is a condition that increases the likelihood or severity of a loss (e.g., faulty wiring, a slippery floor). Insurers assess hazards when setting your premium and may deny a claim if you knowingly concealed a hazard.

How quickly does renters insurance take effect?

Typically, coverage begins as soon as you pay your first premium and the policy is issued, which can often be the same day if you apply online. There is usually no waiting period for standard perils like theft or fire. However, for certain add-ons like flood insurance or earthquake coverage, there may be a mandatory waiting period (e.g., 30 days).

What should I do if my claim is denied?

First, ask for a written explanation citing the specific policy language that justifies the denial. Review your policy. If you believe the denial is incorrect, you can appeal the decision with the insurer, providing additional documentation. If unresolved, you can file a complaint with your state’s Department of Insurance, an authoritative body that regulates insurers. For general dispute guidance, resources like the Insurance Information Institute’s complaint guide can be helpful.