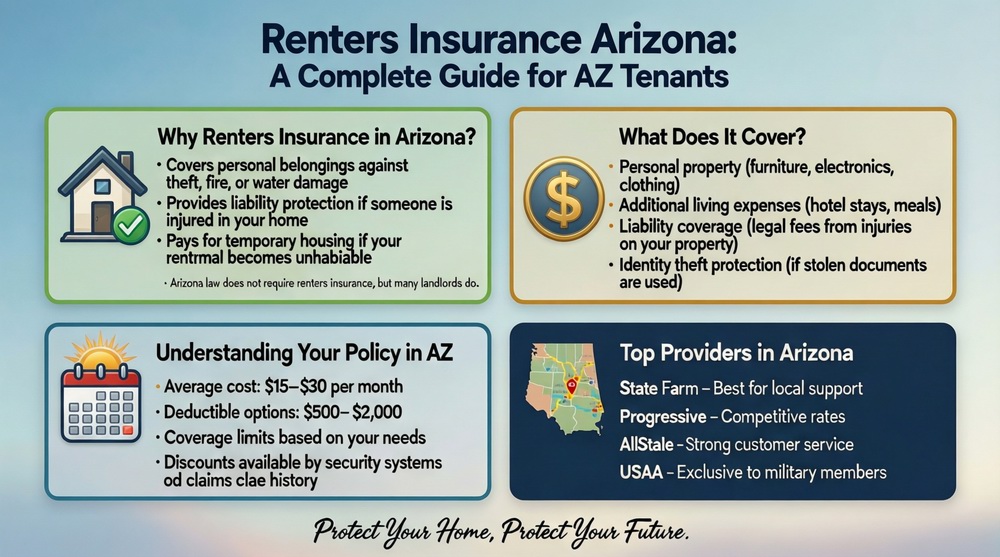

Securing renters insurance Arizona residents need is a smart and affordable step for any tenant. While Arizona law does not mandate renters to carry insurance, an increasing number of landlords and property management companies require it as a lease condition. The average cost in Arizona is slightly below the national average, around $165-$180 per year, but your premium will be influenced by your specific city, the value of your possessions, and Arizona’s unique risks like monsoons, extreme heat, and wildfire smoke. A standard policy protects your personal property from covered perils, provides liability coverage if someone is injured in your rental, and covers additional living expenses if you’re temporarily displaced. This guide will walk you through Arizona-specific considerations, how to get the best rate, and what to look for in a policy. Start by understanding what renters insurance is at its core.

Why Renters Insurance is Essential in Arizona

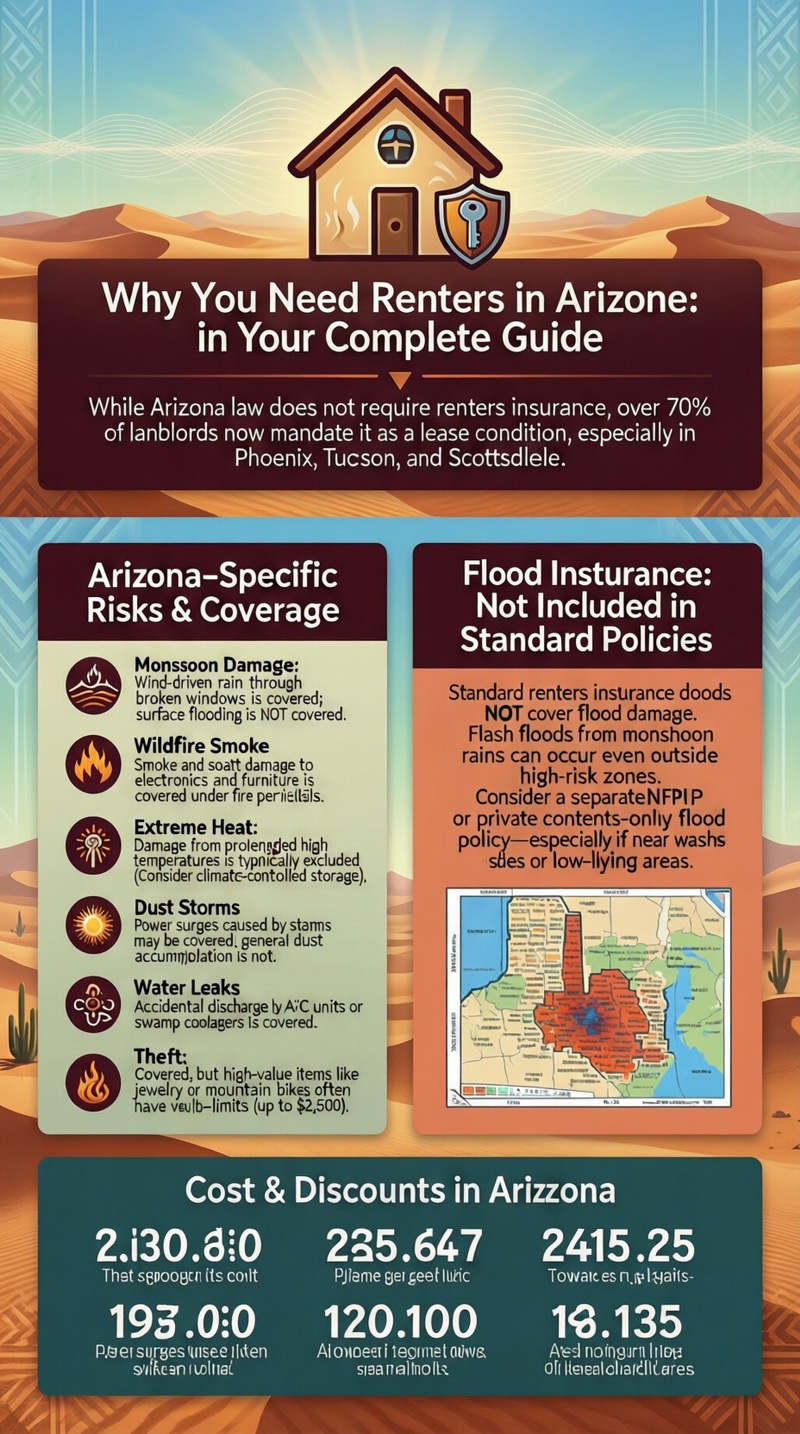

While the foundational reasons for renters insurance Arizona tenants need are universal, several state-specific factors make it particularly valuable. Arizona’s climate and geography present distinct risks. The intense summer monsoon season brings sudden, powerful storms capable of causing roof damage, flooding in low-areas, and wind-driven debris that can break windows. Extreme heat can strain and damage personal electronics and appliances. Furthermore, while your physical rental unit may not be in a direct wildfire path, smoke and soot from nearby wildfires can permeate homes, damaging furniture, clothing, and electronics. A robust renters insurance policy is your financial defense against these unpredictable events, covering the cost to repair or replace your belongings. It also provides crucial liability protection, which is vital in a state with a high rate of recreational activities and guests.

Landlord Requirements and Arizona Law

Arizona state law does not require tenants to carry renters insurance. However, landlords have the right to include a clause in the lease agreement mandating that you obtain and maintain a policy, typically with minimum liability limits (often $100,000). This has become a standard practice, especially in larger apartment complexes and managed properties in cities like Phoenix, Tucson, and Scottsdale. The lease may require you to provide a certificate of insurance naming the landlord as an “additional interest” party, which means they get notified if your policy lapses. Even if it’s not required, it’s a critical form of personal financial protection.

Addressing Common Arizona Misconceptions

Two major misconceptions persist among Arizona renters: “My landlord’s insurance covers me,” and “I don’t own enough to need it.” As elsewhere, your landlord’s policy only covers the building structure, not your personal property within it. Regarding value, most people underestimate the total cost of their clothing, electronics, furniture, kitchenware, and sports equipment—it adds up quickly. Additionally, the liability component is often more valuable than the property coverage, protecting you from devastating lawsuits if a guest is injured in your home.

Arizona-Specific Risks and Coverage Considerations

When shopping for renters insurance Arizona style, you must account for local perils. A standard policy (HO-4) covers named perils like theft, fire, vandalism, and certain water damage. However, you need to scrutinize the details and consider add-ons for comprehensive protection against Arizona’s unique challenges.

| Arizona Risk | Is it Covered by Standard Renters Insurance? | Action Steps & Endorsements |

|---|---|---|

| Monsoon Wind & Rain Damage | PARTIALLY | Wind-driven rain that breaks a window and damages belongings is typically covered. However, flooding from surface water is NOT covered. Ensure you have sufficient personal property limits. |

| Wildfire & Smoke Damage | YES | Fire and smoke are covered perils. If evacuated, your Additional Living Expenses (ALE) coverage pays for hotels/food. Check your ALE limit—it should be adequate for Arizona’s hotel costs. |

| Extreme Heat Damage | NO (usually) | Damage to electronics or other items from consistent high ambient heat is often considered “gradual deterioration” and excluded. Keep valuable items in climate-controlled areas. |

| Dust Storm / Haboob Damage | YES (for resulting perils) | If a dust storm causes a power surge that fries your electronics, that may be covered. If it simply coats everything in dust, cleaning is not a covered loss. |

| Water Damage from A/C or Swamp Cooler | YES | A leaking or overflowing air conditioning unit or evaporative cooler is considered accidental water discharge, a covered peril. |

| Theft / Break-Ins | YES | Covered. Be aware of sub-limits for high-value items like jewelry or mountain bikes. Consider scheduling expensive items. |

The Crucial Flood Insurance Discussion

Many Arizona renters are surprised to learn they might need flood insurance. Monsoon rains can cause rapid, devastating flash flooding in washes, low-lying areas, and even streets. Standard renters insurance Arizona policies do not cover flood damage. Flood insurance is a separate policy through the National Flood Insurance Program (NFIP) or private insurers. Check FEMA’s Flood Maps, but note: over 25% of flood claims occur outside high-risk zones. If your rental is near a wash or in a flat area with poor drainage, a contents-only flood policy is a wise, affordable addition.

Valuables and Recreational Equipment

Arizona’s lifestyle often includes expensive recreational gear: mountain bikes, hiking equipment, golf clubs, and off-road vehicles. Standard policies have sub-limits for sports equipment (often $1,500-$2,500). If you own a high-end mountain bike or a collection of gear, its value may exceed this limit. Discuss these items with your agent to ensure they are fully covered, either by increasing your overall limit or scheduling specific items. For detailed insights, review our page on renters insurance coverage specifics.

Cost of Renters Insurance in Arizona: Cities and Discounts

The average cost for renters insurance Arizona wide is competitive. According to industry data, the average annual premium ranges from $165 to $200, compared to a national average of around $180. However, your exact cost will vary based on location within the state. Urban areas with higher crime rates and property values typically see higher premiums. For example, renters in Scottsdale or central Phoenix may pay more than those in smaller towns like Flagstaff or Sierra Vista. The primary factors affecting your renters insurance cost in AZ are: the amount of personal property coverage, your chosen deductible, your claims history and credit-based insurance score (where permitted), and the safety/security features of your rental unit.

Maximizing Arizona-Specific Discounts

To get the best rate on your renters insurance Arizona policy, ask providers about these discounts:

Bundling Discount: Combine your renters policy with your auto insurance (the most significant savings).

Protective Devices Discount: For having smoke alarms, deadbolt locks, or a monitored security system.

Claims-Free / Loyalty Discount: For maintaining a policy with no claims over time.

Paperless/ Auto-Pay Discount: For enrolling in electronic documents and automatic payments.

Non-Smoker Discount: Many insurers offer a discount if no one in the household smokes.

Getting Quotes from Arizona Providers

It’s essential to compare quotes from multiple companies. Consider a mix of national carriers with a strong AZ presence (State Farm, Allstate, Farmers) and regional or digital insurers (Lemonade, Hippo). When comparing, ensure you’re looking at identical coverage limits, deductibles, and valuation methods (Actual Cash Value vs. Replacement Cost). Replacement Cost coverage, while slightly more expensive, is highly recommended as it pays to buy new items, not their depreciated value.

Top Renters Insurance Companies in Arizona

Many national and regional insurers offer renters insurance Arizona policies. The best company for you depends on your priorities: price, digital experience, local agent support, or bundling.

State Farm: A top market share leader in AZ with a vast network of local agents. Excellent for bundling and personalized service.

Allstate: Another major player with many local agents and strong bundling discounts. Offers good digital tools.

Farmers Insurance: Known for its customizable policies and local agents. A solid choice for those wanting face-to-face interaction.

Lemonade: A popular digital insurer offering instant quotes and claims via an app. Often very competitive on price for standalone policies, appealing to younger renters.

USAA: If you are a veteran, active military, or family member, USAA provides exceptional rates and service (but membership is required).

The key is to get at least three quotes. Don’t forget to explore all renters insurance options available in your specific zip code.

The Role of Local Independent Agents

In Arizona, working with an independent insurance agent can be advantageous. These agents are not tied to one company; they can shop your policy with multiple insurers to find the best combination of coverage and price for your specific needs and location. They can also be invaluable advocates during the claims process.

How to File a Claim in Arizona: Steps and Tips

If you experience a loss, follow these steps to ensure a smooth claims process for your renters insurance Arizona policy:

1. Mitigate Immediate Damage: Take reasonable steps to prevent further loss (e.g., put a tarp over a broken window, move belongings away from water).

2. Document Everything: Take photos and videos of the damage before cleaning up. Create a detailed list of damaged/missing items.

3. File a Police Report: For theft or vandalism, this is mandatory. For other incidents, it can provide official documentation.

4. Notify Your Landlord: Inform them of the damage to the rental property itself.

5. Contact Your Insurance Company: File the claim via phone, website, or app. Provide all documentation and your policy number.

6. Cooperate with the Adjuster: They may call, email, or visit to assess the damage. Provide any additional information they request.

7. Keep Receipts: If you have ALE coverage and need to stay in a hotel, keep all receipts for reimbursement.

For complex perils like water or fire damage, the Arizona Department of Insurance and Financial Institutions provides resources and can assist with disputes, similar to information found on the Insurance Information Institute’s claims guide.

Conclusion: Securing Your Arizona Rental

Obtaining renters insurance Arizona tenants can rely on is one of the most responsible and cost-effective decisions you can make as a renter. For about the price of a few cups of coffee per month, you gain peace of mind knowing your personal possessions are protected from Arizona’s unique mix of perils—from monsoon winds to theft. More importantly, you shield your personal finances from liability lawsuits and gain a safety net if you’re ever temporarily displaced from your home. By understanding the local risks, shopping for quotes with an eye toward proper coverage (not just the lowest price), and maintaining a home inventory, you transform your rental into a truly secure home. Take the time today to get quotes and secure the protection that fits your life in the Grand Canyon State.

Frequently Asked Questions (FAQ)

Is renters insurance required by law in Arizona?

No, Arizona state law does not require tenants to have renters insurance. However, it is extremely common for landlords and property management companies to require it as a condition in the lease agreement. They can mandate minimum liability coverage (e.g., $100,000) and require you to provide proof of insurance before move-in and upon renewal.

Does renters insurance in Arizona cover scorpion or pest infestations?

No. Standard renters insurance does not cover damage or the cost of removal for insect, rodent, or pest infestations, including scorpions. This is considered a maintenance issue. Any damage to your belongings from pests (e.g., rodents chewing wires) is also generally excluded. Pest control is the responsibility of the tenant or landlord, depending on the lease terms.

Will my policy cover me if I’m temporarily relocated due to a wildfire?

Yes, this is a key coverage. If a civil authority mandates an evacuation or your rental is uninhabitable due to a covered peril like wildfire, the Additional Living Expenses (ALE) portion of your policy will pay for reasonable extra costs. This includes hotel stays, restaurant meals (above your normal food budget), laundry, and pet boarding. Be sure to keep all receipts.

Are roommates covered under one renters insurance policy in Arizona?

Typically, only the named insured and their relatives are covered. If you have unrelated roommates, they are not automatically covered under your policy. They would need to be added as “named insureds,” which can complicate matters if you have a claim. The safest and most common approach is for each roommate to purchase their own individual renters insurance policy to cover their own belongings and liability.

How does Arizona’s extreme heat affect my electronics coverage?

Standard renters insurance covers electronics for named perils like theft, fire, or power surges from lightning. However, damage caused solely by prolonged exposure to high ambient heat (e.g., a laptop left in a hot car that warps) is typically excluded, as it’s considered gradual deterioration or neglect. It’s best to store and use electronics in climate-controlled environments.

What is the most important coverage to have in Arizona?

While all parts are important, two stand out: 1) Liability Coverage protects your assets if you’re found responsible for injuring someone or damaging their property—this can shield you from financial ruin. 2) Replacement Cost Value for your personal property. Arizona’s sun and heat can depreciate items quickly; ACV would give you very little for a 3-year-old couch, while RCV allows you to buy a new one.

Can my Arizona renters insurance be canceled for filing a claim?

Insurers cannot cancel a mid-term policy in retaliation for filing a claim. However, after the policy period ends (at renewal), the company may choose not to renew your policy based on your claims history or other risk factors. For small claims close to your deductible amount, it’s often worth considering whether filing is financially prudent in the long run, as it could affect your renewal premium or eligibility.