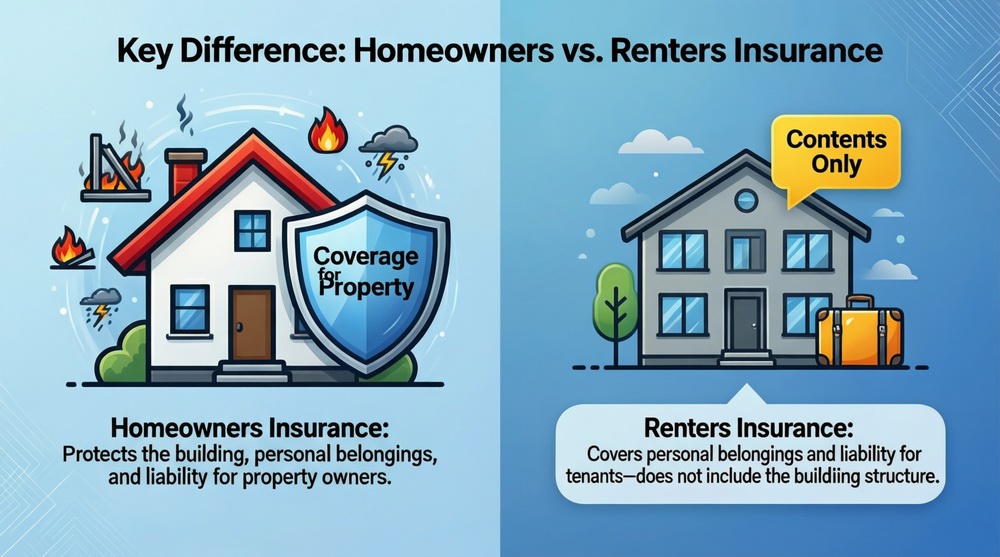

If you’re asking, “what is the primary difference between homeowners insurance and renters insurance?”, the core answer is this: Homeowners insurance covers the physical structure of the home and the owner’s personal belongings inside it, while renters insurance covers only the tenant’s personal belongings and liability—not the building itself. A homeowner is financially responsible for rebuilding their house after a fire; a renter is not. This fundamental distinction of structure vs. contents drives all other variations in coverage, cost, and requirement. This guide will explore this critical difference in depth, along with coverage details, costs, and scenarios to help you fully understand what renters insurance is and how it compares to protecting a home you own.

The Core Distinction: Structure vs. Contents

The single most important factor in answering “what is the primary difference between homeowners insurance and renters insurance?” is the point of financial responsibility. When you own a home, you own the dwelling—the walls, roof, foundation, and built-in fixtures. You are on the hook for hundreds of thousands of dollars in reconstruction costs if it’s damaged. Therefore, homeowners insurance must include Dwelling Coverage (Coverage A) as its cornerstone. When you rent, your landlord owns the structure. Your financial stake is in your personal property within the walls—your furniture, electronics, clothing, and other belongings—which is what renters insurance is designed to protect. This is not just a coverage detail; it’s the entire philosophical and financial basis for each policy type.

Understanding “Dwelling Coverage” in Homeowners Insurance

Dwelling coverage is the part of a homeowners policy that pays to repair or rebuild the physical structure of your home (including attached structures like a garage) if it’s damaged by a covered peril, such as fire, windstorm, or hail. The coverage limit should equal your home’s estimated replacement cost, not its market value. This is the most substantial and expensive component of a homeowners policy, as it protects the owner’s largest asset. Without it, a homeowner could face financial ruin from a single major incident.

Understanding “Personal Property Coverage” in Both Policies

Both homeowners and renters insurance include personal property coverage (Coverage C in a standard HO-3 policy). However, its role and proportion are vastly different. For a homeowner, it’s a secondary component, often set at 50-70% of the dwelling coverage limit. For a renter, it’s the primary component. The renter selects a limit (e.g., $20,000) based on the total value of their possessions. Both policies cover belongings against named perils, but a key difference often lies in the valuation method: homeowners policies frequently include “replacement cost” for personal property, while basic renters policies may default to “actual cash value” (depreciated value), though this can often be upgraded.

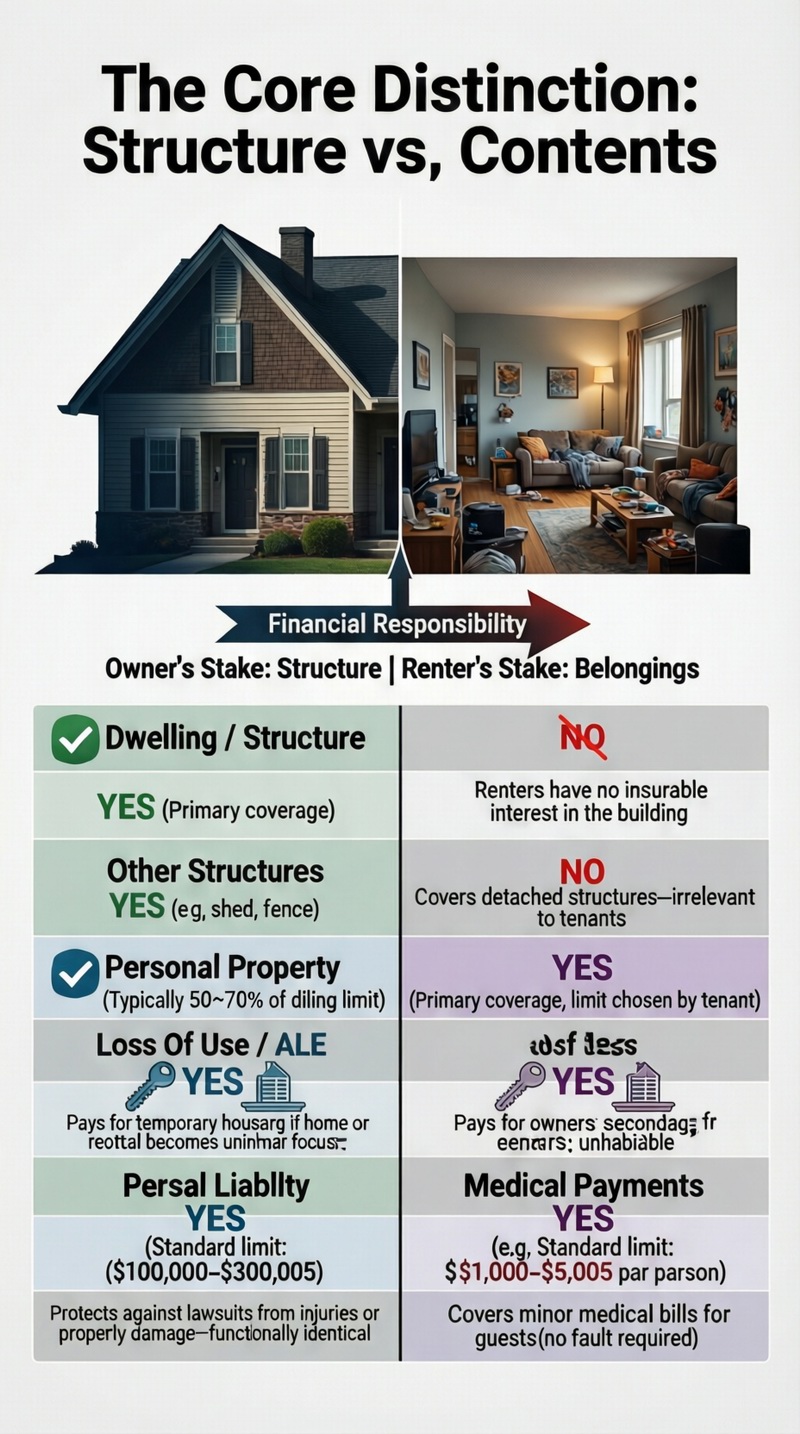

Coverage Breakdown: A Side-by-Side Comparison

Beyond the structure vs. contents divide, there are important similarities and differences in other standard coverages. Both policies provide personal liability protection and additional living expenses (ALE), but the context and typical limits vary. The following table provides a clear, visual comparison of the six standard coverage parts, highlighting the answer to “what is the primary difference between homeowners insurance and renters insurance?” across all facets of protection. For a deeper dive into the specifics of tenant protection, review our guide on renters insurance coverage details.

| Coverage Type | Homeowners Insurance (HO-3) | Renters Insurance (HO-4) | Key Difference Insight |

|---|---|---|---|

| Dwelling / Structure | YES (Primary coverage) | NO | The fundamental divide. The renter has no insurable interest in the building. |

| Other Structures | YES (e.g., shed, fence) | NO | Covers structures detached from the main home. Not applicable to tenants. |

| Personal Property | YES (Typically 50-70% of dwelling limit) | YES (Primary coverage, limit chosen by tenant) | A core coverage for both, but it’s secondary for owners and primary for renters. |

| Loss of Use / ALE | YES (Covers living expenses if home is uninhabitable) | YES (Covers living expenses if rental is uninhabitable) | Functionally identical. Pays for hotel, meals, etc., above your normal standard of living. |

| Personal Liability | YES (Standard limit often $100,000-$300,000) | YES (Standard limit often $100,000) | Nearly identical. Covers injuries or property damage you are legally responsible for. |

| Medical Payments | YES (e.g., $1,000-$5,000 per person) | YES (e.g., $1,000-$5,000 per person) | Identical. Pays for minor medical bills for guests injured on your property, regardless of fault. |

Similarities in Liability and Additional Living Expenses

It’s crucial to note that renters insurance is not “lesser” in all aspects. The liability and additional living expenses (ALE) coverages are functionally identical to those in a homeowners policy. If a guest slips and falls in your rented apartment, your renters liability coverage responds just as a homeowner’s would. If a fire makes your rental unit unlivable, your renters ALE coverage will pay for your temporary housing and related expenses. These coverages address risks that are entirely separate from property ownership, which is why they are essential for both homeowners and tenants.

Perils Covered: “Open Peril” vs. “Named Peril”

Another nuanced difference often lies in the form used. A standard homeowners policy (HO-3) typically covers the dwelling on an “open peril” basis, meaning it covers everything except specific exclusions (like flood or earthquake). The personal property coverage, however, is usually on a “named peril” basis, covering only the perils listed (e.g., fire, theft, vandalism). A standard renters policy (HO-4) usually covers personal property on the same “named peril” basis. This means the list of events that trigger coverage for your belongings is generally the same for both policies, even though the homeowner also has the broader structural protection.

Cost Implications: Why Renters Insurance Is So Much More Affordable

The dramatic difference in cost between the two policies is a direct result of the primary difference in what they cover. According to national averages, the annual premium for homeowners insurance is around $1,700, while renters insurance costs only about $180 per year—roughly one-tenth the price. This is because the insurance company’s potential financial loss (the “risk”) is massively different. A homeowners insurer may need to pay $300,000 to rebuild a house after a total loss. A renters insurer only needs to cover, say, $30,000 worth of a tenant’s contents and a liability claim. This lower risk translates into a much lower premium, making renters insurance one of the most cost-effective forms of financial protection available. Understanding renters insurance cost factors can help you find the best rate.

Factors That Influence Each Policy’s Price

While both policies consider factors like location, claims history, and credit-based insurance scores, the rating factors diverge due to the different risks:

Homeowners Insurance Cost Drivers: Home’s replacement cost, construction materials, age of roof and major systems, proximity to fire hydrants, local fire department rating, and swimming pools or other high-risk features.

Renters Insurance Cost Drivers: Chosen personal property limit, deductible amount, whether you want replacement cost or actual cash value, and the safety features of the rental unit (smoke alarms, security system). The building’s value is irrelevant.

The Affordability Misconception

Many renters mistakenly believe insurance is expensive because they mentally associate it with homeowners insurance costs. This misconception can lead to going uninsured. In reality, for less than the price of a few streaming services per month, a renter can secure robust liability and property protection. The affordability of renters insurance is a direct benefit of not being responsible for the multi-hundred-thousand-dollar structure.

Who Needs Which Policy? Scenarios and Requirements

Determining which policy you need is typically straightforward, but certain living situations can create confusion. If you hold a mortgage, your lender will require you to carry homeowners insurance to protect their financial interest in the property. If you rent, an increasing number of landlords and property management companies require renters insurance as a condition of the lease to limit their own liability and ensure tenants can recover from a loss without seeking recourse against the landlord. This requirement is becoming a standard best practice in the rental industry. Exploring all renters insurance options is wise when your lease mandates coverage.

Special Situations: Condo Owners and Life Estate Tenants

Two scenarios that blur the lines are condominium ownership and certain family living arrangements. Condo owners need a condo insurance policy (HO-6), which is a hybrid. It primarily covers the interior of the unit (like upgraded fixtures and personal property) and provides liability coverage, while the condo association’s master policy covers the building’s exterior and common areas. Someone with a “life estate” (the right to live in a home owned by someone else until they die) may have a unique insurable interest that requires a specialized policy, often discussed with the property owner and an agent.

The Critical Importance of Liability Coverage for Renters

A common renter’s mistake is thinking, “My stuff isn’t worth much, so I don’t need insurance.” This overlooks the liability component, which is arguably more important. If your dog bites a visitor, you accidentally start a kitchen fire that damages other units, or a guest has a serious fall in your apartment, you could be sued for medical bills, lost wages, and pain and suffering. Renters liability coverage provides a legal defense and pays for damages up to your policy limit, protecting your current assets and future income from garnishment. This protection is identical in function to a homeowner’s liability coverage.

Making the Right Choice and Avoiding Gaps

Understanding what is the primary difference between homeowners insurance and renters insurance is the first step in avoiding dangerous coverage gaps. The most common gap occurs when a renter assumes their landlord’s insurance covers them—it does not. The landlord’s policy covers only the building and the landlord’s liability. Your belongings and your personal liability are 100% your responsibility. Another gap can occur when a homeowner drastically underestimates their dwelling replacement cost or fails to update it with inflation and renovations, leaving them underinsured.

Actionable Steps for Renters and Homeowners

For Renters: 1) Take a home inventory to estimate the value of your belongings. 2) Get quotes for a renters policy, ensuring you understand the perils covered and choose between ACV and Replacement Cost. 3) Consider an umbrella policy if you need liability limits above the standard $100,000-300,000. 4) Provide your landlord with a certificate of insurance if required.

For Homeowners: 1) Regularly review your dwelling coverage limit with your agent to account for inflation and local construction costs. 2) Document your home’s features and upgrades. 3) Consider scheduled endorsements for high-value items like jewelry or art that exceed standard sub-limits. 4) Evaluate the need for separate flood or earthquake policies based on your location.

Consulting Authoritative Resources

For official definitions and detailed explanations of policy forms and standard coverages, one of the most reliable external resources is the Insurance Information Institute. Their comprehensive guides, such as their breakdown of a standard homeowners policy, provide authoritative, unbiased information that can help clarify complex insurance terms and concepts.

Conclusion

In conclusion, when asking “what is the primary difference between homeowners insurance and renters insurance?” remember it all stems from responsibility for the physical structure. Homeowners insurance is a comprehensive package protecting a massive asset (the home) and its contents. Renters insurance is a streamlined, affordable policy protecting your movable assets and your legal liability. One is not “better” than the other; each is precisely engineered for a specific form of occupancy. By understanding this core distinction—structure vs. contents—you can confidently secure the right policy, avoid costly assumptions, and ensure that your home, whether owned or rented, is a properly protected sanctuary.

Frequently Asked Questions (FAQ)

Does my landlord’s insurance cover my belongings?

No, absolutely not. This is the most dangerous misconception among renters. Your landlord’s insurance policy covers only the physical structure of the building and their own liability as the property owner. It does not extend to your personal property inside the unit, nor does it cover your personal liability for incidents that occur within your rented space. Protecting your belongings and your financial future is 100% your responsibility, which is why renters insurance is essential.

Can I get renters insurance if I live with roommates?

Yes, but coverage specifics are important. A standard renters policy typically covers only the named insured and their relatives. If you have unrelated roommates, they would not be covered under your policy unless they are specifically listed as a “named insured.” The better practice is for each roommate to purchase their own individual policy. Some insurers offer policies that can cover multiple unrelated individuals, but all parties must be named, and claims payments may be made jointly, which can complicate matters.

Is flood or earthquake damage covered under either policy?

No, not under standard forms. Both standard homeowners (HO-3) and renters (HO-4) policies explicitly exclude damage caused by floods and earthquakes/seismic activity. Flood insurance must be purchased separately through the National Flood Insurance Program (NFIP) or a private flood insurer. Earthquake coverage can sometimes be added as an endorsement (for an additional premium) to a homeowners policy or purchased as a separate policy. For renters, earthquake endorsements may be available to cover personal property, but the building itself remains the landlord’s concern.

How much personal property coverage do I need as a renter?

You need enough to cover the total replacement cost of all your belongings. The best way to determine this is to create a detailed home inventory, room by room. List items, their purchase price or estimated current value, and note serial numbers for electronics. Most renters find they need between $20,000 and $50,000 in coverage. Remember, it’s not just big-ticket items; clothing, kitchenware, books, and linens add up quickly. It’s better to slightly overestimate than to be underinsured after a loss.

If I work from home, are my business items covered?

Coverage for business property is very limited under both homeowners and renters policies. Typically, only a small amount (e.g., $2,500) is covered for business property in the home, and there is usually no coverage for business property away from the home (like a laptop you take to a coffee shop). Furthermore, liability related to a home business is generally excluded. If you run a business or have significant work-related equipment at home, you likely need a separate business insurance policy or a specific endorsement (like an “in-home business” rider) to your renters or homeowners policy.

Does renters insurance cover my car or things in my car?

No. Items stolen from your car are generally covered by your renters insurance policy (under the “theft” peril), as they are considered off-premises personal property. However, the car itself, its stereo system permanently installed in the dash, or any damage to the car from theft or vandalism is not covered by renters insurance. That is the function of your auto insurance policy, specifically the comprehensive coverage portion.

What happens if my rental becomes unlivable after a fire?

This is where your renters insurance proves invaluable. The “Loss of Use” or “Additional Living Expenses (ALE)” coverage will pay for the extra costs you incur while your primary residence is being repaired. This includes hotel bills, restaurant meals (above your normal food budget), laundry costs, pet boarding, and even storage fees for your salvaged belongings. It typically covers you for the reasonable time required to repair the unit or for you to find a new permanent residence, up to the policy limit (often a percentage of your personal property limit).