When asking “what is the average cost of renters insurance?”, the answer isn’t one-size-fits-all. Your premium depends on your location, belongings, and chosen coverage. However, understanding national averages and key pricing factors empowers you to budget effectively and shop smartly. This guide provides clear 2024 cost data, breaks down what influences your rate, and answers crucial questions like monthly expenses and how to find affordable coverage. Let’s explore the real numbers behind renters insurance cost and how you can secure the best value for your protection.

What Is the Average Cost of Renters Insurance Nationally?

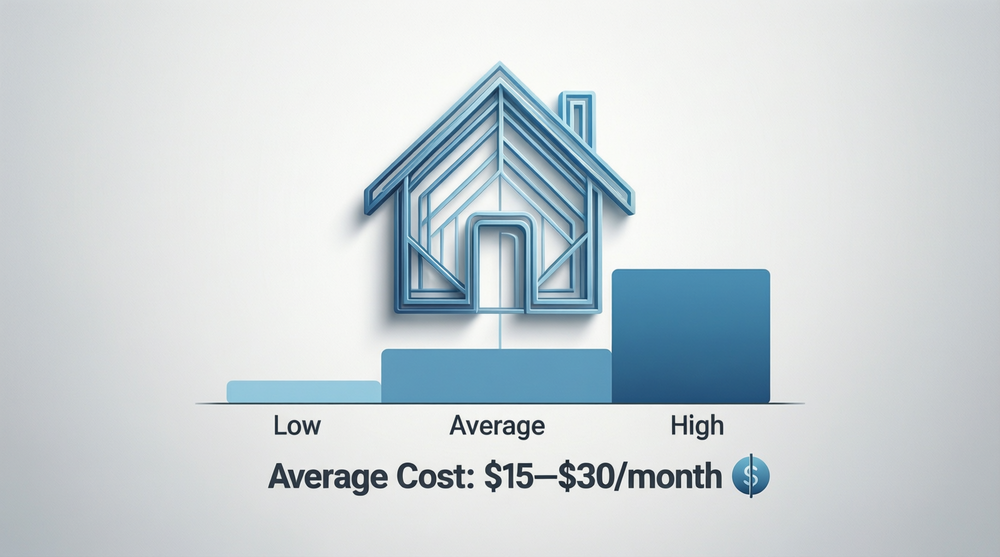

According to 2024 data from industry analysts like the Insurance Information Institute and Quadrant Information Services, the national average cost for a standard renters insurance policy is approximately $15 to $30 per month, or $180 to $360 per year. This average is for a policy with $30,000 in personal property coverage, $100,000 in liability coverage, and a $500 deductible.

What Is the Most Common Amount for Renters Insurance?

The most common policy amount, which forms the basis of the average cost, typically includes:

- $30,000 in personal property coverage.

- $100,000</strong in personal liability coverage.

- A $500 deductible.

This level of coverage is a standard starting point for a single adult or couple in a one-to-two-bedroom apartment with a moderate amount of belongings. It answers the core question of what is the average cost of renters insurance for a baseline policy.

Breaking Down the Monthly Cost: How Expensive Is Renters Insurance Monthly?

For most renters, insurance is a very manageable monthly expense. To put it in perspective:

- The average monthly cost of **renters insurance** is often less than a single streaming service subscription or a few cups of coffee.

- It frequently costs one-tenth the price of the average auto insurance premium.

You can expect to pay $12 to $25 per month in low-risk areas, while renters in major metropolitan cities or regions prone to natural disasters might see monthly premiums of $30 to $50+. The best way to know your exact monthly cost is to get personalized quotes based on your address and needs.

Key Factors That Determine Your Personal Premium

Your answer to “what is the average cost of renters insurance for ME?” depends on several variables. Insurers assess these to calculate your specific risk level.

1. Your Location (ZIP Code)

This is the biggest factor outside your control. Your premium is heavily influenced by:

- Local Crime Rates: Higher theft and vandalism rates mean higher premiums.

- Proximity to a Fire Station: Closer proximity can lower your rate.

- Regional Weather Risks: Living in an area prone to tornadoes, hurricanes, or wildfires increases cost.

2. Coverage Limits and Deductible Choice

You directly control these costs. Higher coverage limits and lower deductibles increase your premium, and vice versa.

| Coverage Choice | Lower-Cost Option | Higher-Cost Option | Impact on Premium |

|---|---|---|---|

| Personal Property Limit | $20,000 | $50,000 | Higher limit = Higher premium |

| Liability Limit | $100,000 | $500,000 | Higher limit = Slightly higher premium |

| Deductible | $1,000 | $500 | Lower deductible = Higher premium |

| Replacement Cost vs. Actual Cash Value | Actual Cash Value | Replacement Cost | Replacement Cost = Higher premium |

3. Your Personal Profile

Insurers also consider:

- Credit-Based Insurance Score: In most states, a higher score can lead to lower rates.

- Claims History: A history of filing frequent insurance claims may increase your cost.

- Certain Dog Breeds: Owning a breed insurers deem high-risk can increase premiums or lead to exclusions. Learn more in our guide on renters insurance with restricted breeds.

Cost Scenarios: How Much Does $500,000 Renters Insurance Cost?

Policies with high liability limits like $500,000 are recommended for those with more assets or higher risk. The cost increase is often less than you might think.

While a standard $100,000 liability policy might average $180/year, upgrading to $500,000 in liability coverage may only cost an additional $20 to $50 per year. This small investment provides crucial extra protection against lawsuits. For a detailed look at what this coverage includes, see our page on renters insurance coverage.

Finding the Best Deal: Who Has the Cheapest Rental Insurance?

There is no single “cheapest” company for everyone. The most affordable insurer for you depends on your unique profile. However, some companies are consistently competitive:

- Lemonade: Often offers low starting rates through its digital-first model and gives back unused premiums.

- State Farm: A major provider with extensive discount options (bundling, security devices) that can lead to very low final premiums.

- Travellers: Frequently ranks well for value in customer satisfaction surveys.

The real answer: The cheapest rental insurance for you will come from comparing personalized quotes from at least 3-4 companies. Use online comparison tools or an independent agent. Don’t forget to apply all eligible discounts, which is one of the most effective ways to lower renters insurance cost.

How to Get an Accurate Quote for Your Situation

To move beyond averages and find your true cost, follow these steps:

- Take a Home Inventory: Know the approximate value of your belongings to choose the right personal property limit.

- Decide on Liability & Deductible: Choose liability limits ($300K+ is wise) and a deductible you can afford.

- Gather Your Info: Have your driver’s license, Social Security number, and basic info about your rental unit ready.

- Shop Around: Get quotes from different types of insurers (major, digital, regional).

Conclusion: Affordable Protection Is Within Reach

So, what is the average cost of renters insurance? Nationally, it’s a very affordable $15-$30 per month for solid baseline coverage. Your personal cost depends on location, coverage choices, and discounts. Remember, the goal isn’t just the cheapest policy, but the best value—adequate protection at a fair price. By understanding the factors at play, raising your deductible wisely, and shopping competitively, you can secure essential financial protection without straining your budget. Start your search today to lock in your rate and gain peace of mind. For a foundational understanding, begin with what renters insurance is.

Frequently Asked Questions (FAQ)

Q1: Is renters insurance really worth the monthly cost?

A: Absolutely. For less than a dollar a day on average, you get liability protection that can save you from financial ruin in a lawsuit, and coverage to replace your belongings after theft or disaster. The potential benefit far outweighs the minimal cost.

Q2: Why does my friend in another state pay half what I do?

A: Location is a primary cost driver. Differences in state regulations, local crime rates, and natural disaster risks create significant price variations. Your friend likely lives in a lower-risk area.

Q3: Can my landlord require me to have renters insurance and dictate the cost?

A: Yes, landlords can and often do require tenants to carry renters insurance. However, they cannot dictate which company you use or the exact cost you pay. They can only specify minimum coverage amounts (e.g., $100,000 liability).

Q4: Will my premium go up if I file a claim?

A: Often, yes. Filing a claim, especially for a preventable incident, can lead to a premium increase at renewal. For very small losses, it may be more cost-effective to pay out-of-pocket to avoid a rate hike.

Q5: How can I get the most accurate online quote?

A: Be as precise as possible. Use your exact ZIP+4 code, provide accurate information about security features (deadbolts, alarms), and give a realistic estimate of your belongings’ value. Inaccurate info can lead to price changes later. For reliable data on insurance trends, you can also review reports from the Insurance Information Institute.

Q6: Are there any hidden fees with renters insurance?

A: Most companies charge a small monthly installment fee if you don’t pay your premium annually. Always ask if there are “policy fees” or “service fees.” Reading the quote breakdown carefully will show all charges.

Q7: Does the age or type of my apartment building affect cost?

A: Yes. Newer buildings with updated electrical, plumbing, and fire suppression systems (like sprinklers) may qualify for lower rates. Older buildings without updates may be seen as higher risk for fire or water damage.