Answering “how much renters insurance do I need?” requires focusing on three numbers: Personal Property, Liability, and Additional Living Expenses (ALE). A quick rule of thumb: Personal Property should equal the total replacement cost of everything you own (often $20,000-$50,000+). Liability should be at least $100,000, but $300,000 is safer. ALE should be 20-30% of your Personal Property limit. The only way to get an accurate figure is to conduct a home inventory. For a baseline understanding, start with our guide on what renters insurance is.

Quick Estimate Table:

– Studio / Minimalist: $20,000 Personal Property, $100,000 Liability

– 1-Bedroom / Average: $30,000 – $40,000 Personal Property, $300,000 Liability

– 2+ Bedrooms / Well-Furnished: $50,000+ Personal Property, $500,000 Liability (consider an Umbrella Policy)

Part 1: Calculating Personal Property Coverage (Your Stuff)

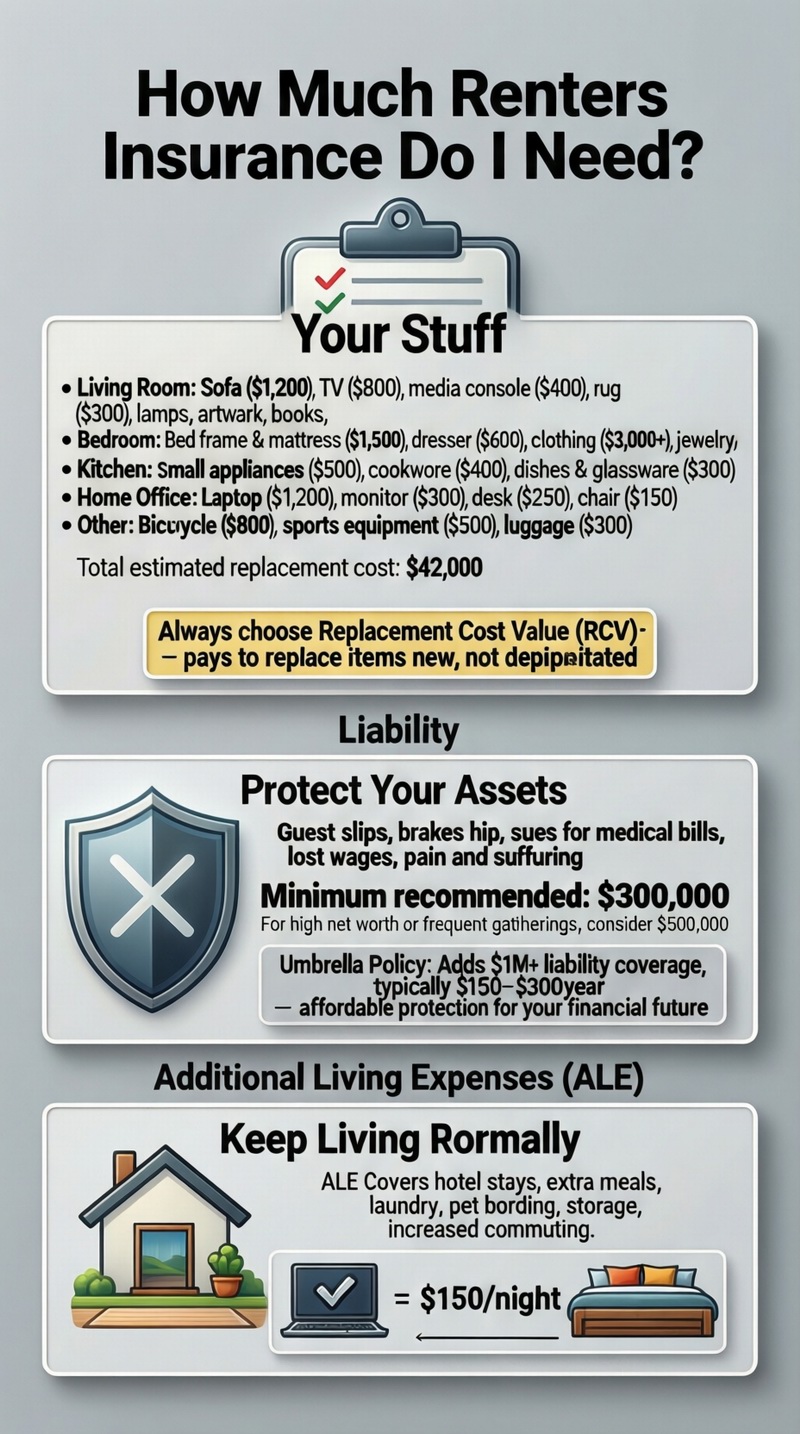

This is the most common question when determining how much renters insurance you need. Your personal property limit (Coverage C) is the maximum amount your insurer will pay to repair or replace your belongings after a covered loss like theft or fire. Underestimating this number is the #1 mistake renters make.

The Step-by-Step Home Inventory Method

There’s no substitute for a detailed home inventory. Go room-by-room and list every item, estimating its current replacement cost (what it would cost to buy new today).

Living Room: Sofa ($1,200), TV ($800), media console ($400), rug ($300), lamps, artwork, books, etc.

Bedroom: Bed frame & mattress ($1,500), dresser ($600), clothing ($3,000+), jewelry, etc.

Kitchen: Small appliances ($500), cookware ($400), dishes & glassware ($300).

Home Office: Laptop ($1,200), monitor ($300), desk ($250), chair ($150).

Other: Bicycle ($800), sports equipment ($500), luggage ($300).

Tip: Use a spreadsheet, app, or video walkthrough. Most people are shocked to find their total exceeds $25,000. For a deeper look at what this covers, see our renters insurance coverage breakdown.

Understanding “Actual Cash Value” vs. “Replacement Cost”

This choice drastically affects how much renters insurance you need financially after a claim.

Actual Cash Value (ACV): Pays the item’s value minus depreciation. A 5-year-old TV might only net you $150. This often leads to being underinsured even with “enough” coverage.

Replacement Cost Value (RCV): Pays the cost to buy a new, comparable item. That same TV gets replaced with a new $800 model. Always choose RCV coverage if available. It typically increases your premium by 10-20% but is worth it.

Special Limits for High-Value Items

Policies have “special limits” or sub-limits for certain categories. You may need additional coverage (scheduling) if you own items exceeding these typical limits:

| Item Category | Typical Sub-Limit | Action if You Exceed It |

|---|---|---|

| Jewelry, Watches, Furs | $1,000 – $2,500 (for theft) | “Schedule” individual high-value pieces. |

| Firearms | $2,000 – $3,000 (for theft) | Schedule the collection. |

| Silverware | $2,500 – $5,000 | Increase limit or schedule. |

| Business Property | $2,500 (on & off premises) | Consider a separate business policy. |

| Electronics (non-scheduled) | Part of general property | Ensure total limit is sufficient. |

Part 2: Determining Your Liability Coverage Limit

Liability coverage (Coverage E) protects your assets if you are found legally responsible for injuring someone or damaging their property. When considering how much renters insurance you need for liability, think about your net worth and future earnings.

Why $100,000 is Often Not Enough

A guest slips in your apartment, breaks a hip, and sues for medical bills, lost wages, and pain and suffering. Such a lawsuit can easily exceed $100,000. If a judgment is more than your limit, your personal savings, investments, and even future wages could be garnished. Recommended minimum: $300,000. If you have significant assets, a higher net worth, or host frequent gatherings, consider $500,000.

The Role of an Umbrella Policy

A personal umbrella policy provides an extra $1 million (or more) in liability coverage on top of your renters and auto insurance limits. It’s surprisingly affordable (often $150-$300 per year) and is the ultimate protection for your financial future. It’s a smart move once your assets or risk exposure grow.

Part 3: Additional Living Expenses (ALE) / Loss of Use

If a covered disaster (like a fire) makes your rental uninhabitable, ALE (Coverage D) pays for you to maintain your normal standard of living elsewhere. Underestimating this is a common error.

How to Calculate Your ALE Need

ALE covers:

– Temporary housing (hotel, short-term rental)

– Restaurant meals and food costs above your normal grocery spending

– Laundry, storage, pet boarding, and increased commuting costs

Policies typically set the ALE limit as a percentage of your personal property coverage (e.g., 20-30%). If you have $30,000 in property coverage, you might have $6,000-$9,000 for ALE. Is that enough? Consider:

– Local Hotel Costs: $150/night x 30 days = $4,500

– Extra Food: $40/day x 30 = $1,200

– Other Costs: Laundry, commuting = $500

Total Estimated: $6,200

In this case, a $6,000 limit might be tight. You can often increase your ALE limit for a small additional premium.

The Final Calculation: Bringing It All Together

Let’s walk through a real-world example for “Sarah,” a professional with a one-bedroom apartment.

Step 1: Personal Property Inventory Total: $42,000 (includes furniture, electronics, clothing, kitchenware).

Step 2: Chosen Coverage: $45,000 limit with Replacement Cost.

Step 3: Liability Limit: Chooses $300,000 (has a moderate savings account).

Step 4: ALE Limit: Policy automatically provides 30% of property limit = $13,500. Sarah confirms this is sufficient for her area.

Step 5: Deductible: Chooses a $500 deductible to balance premium savings and out-of-pocket cost.

Sarah’s Answer to “How much renters insurance do I need?”: A policy with $45,000 Personal Property (RCV), $300,000 Liability, and $13,500 ALE, with a $500 deductible.

How Your Choices Affect Your Premium

Understanding renters insurance cost drivers helps you make informed trade-offs:

– Increasing Personal Property Limit: Moderate increase. Going from $20k to $40k might add $30-$60/year.

– Switching from ACV to RCV: Adds 10-20% to the premium’s property portion.

– Increasing Liability from $100k to $300k: Very small increase, often $10-$20/year.

– Choosing a Higher Deductible: Lowers your premium. Going from $500 to $1,000 might save 10-15%.

Common Mistakes to Avoid When Choosing Limits

Mistake 1: Insuring for the value of your belongings, not the replacement cost. You must insure for the cost to buy everything new (RCV).

Mistake 2: Forgetting about off-premises coverage. Your stuff is covered anywhere in the world, usually at 10% of your total limit. Ensure that’s enough for items you travel with.

Mistake 3: Not updating your policy. When you buy a new laptop, TV, or jewelry, your total property value increases. Review your limits annually.

Mistake 4: Ignoring liability. It’s the most important coverage for protecting your wealth. Don’t skimp.

To avoid these, explore and compare all renters insurance options with the right limits in mind.

Conclusion: It’s Better to Be Over-Insured Than Under-Insured

Determining how much renters insurance you need is not about finding the cheapest policy; it’s about finding adequate protection. The few extra dollars per month for higher limits and Replacement Cost coverage are insignificant compared to the financial catastrophe of being underinsured after a fire or lawsuit. Take an afternoon to conduct a home inventory, assess your liability risk, and choose limits that let you sleep soundly, knowing you’re fully protected. Don’t guess—calculate, then contact insurers for quotes based on your informed numbers.

Frequently Asked Questions (FAQ)

Can my landlord tell me how much renters insurance to get?

Yes, for liability. Landlords can (and often do) specify a minimum liability limit in the lease, commonly $100,000. They cannot dictate your personal property limit, as that’s based on your own belongings. You must provide proof of insurance meeting their liability requirement.

What if I have roommates? How does that affect coverage needs?

Each roommate should have their own separate policy. Your policy covers your belongings and your liability only. If you share expensive items (like a living room TV), decide who insures it or each insure a portion. Never assume one policy covers all unrelated roommates—it leads to coverage gaps and claims disputes.

Is there a maximum limit for renters insurance?

Yes, insurers have maximum limits they will offer, often around $100,000 for personal property and $500,000 for liability on a standard policy. If you need more (e.g., for an extremely high-value art collection), you’ll need to schedule items or purchase a specialized valuable articles policy (a “floater”) and a personal umbrella policy for excess liability.

How often should I review my coverage limits?

At least once a year, or whenever you have a significant life change: moving, getting married, making a major purchase (like expensive electronics or jewelry), or starting a home-based business. An annual check-up ensures your coverage keeps pace with your life.

Does renters insurance cover my home business equipment?

Only up to a very low limit (typically $2,500). If you run a business from home, your computer, printer, and inventory may be inadequately covered. You likely need a separate business insurance policy (In-home business endorsement or a BOP) to properly cover business property and liability.

What is “replacement cost” for a discontinued item?

If an item is no longer made, the insurer will pay the cost to purchase the most similar, comparable item currently available on the market. For unique antiques or collectibles, this is why scheduling with an agreed value (based on an appraisal) is essential.

Where can I find a reliable home inventory tool or guide?

Many insurers offer apps. For a trusted, independent resource, the Insurance Information Institute offers a comprehensive home inventory guide and downloadable sheets. They provide a step-by-step approach to documenting your possessions, which is the cornerstone of answering “how much renters insurance do I need?” accurately.